January 2, 2018

Dear Fellow Shareholders,

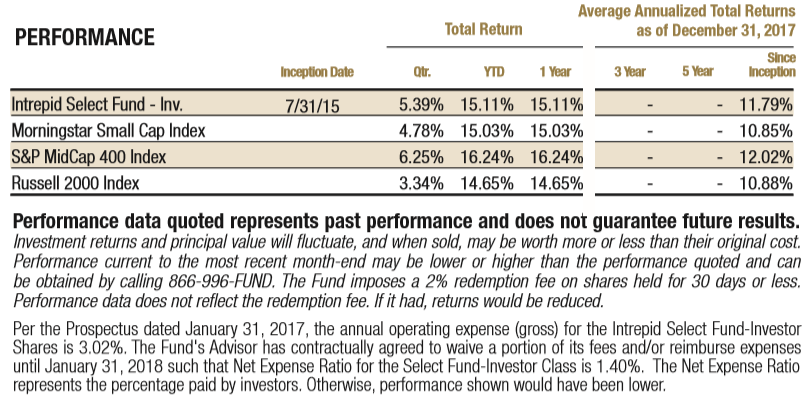

The Intrepid Select Fund (the “Fund”) appreciated 5.39% in the fourth quarter and 15.11% for 2017. The Russell 2000, Morningstar Small Cap Total Return, and S&P MidCap 400 indexes returned 3.34%, 4.78%, and 6.25%, respectively, for the fourth quarter. For the full calendar year, the Russell 2000, Morningstar Small Cap, and S&P MidCap 400 were up 14.65%, 15.03%, and 16.24%, respectively. The Fund’s performance was similar to benchmarks despite holding an average of around 12.5% of Fund assets in cash over the course of the year. Our holdings increased in price more than benchmarks. At the end of the year, 11.3% of the Fund was held in cash equivalents. The Select Fund experienced inflows near the end of December, which raised the level of cash.

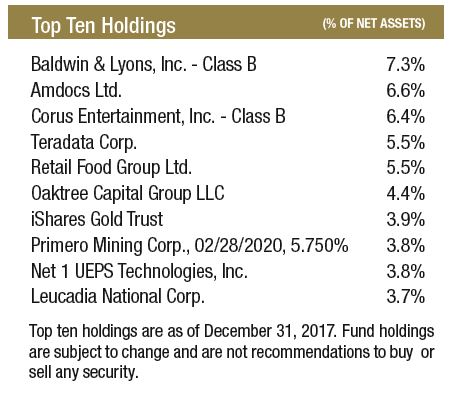

The Fund purchased three new securities in the fourth quarter: Discovery Communications (ticker: DISCK), Net 1 UEPS Technologies (ticker: UEPS), and Retail Food Group (ticker: RFG AU). Discovery Communications is one of the world’s largest providers of television programming. The TV industry is facing considerable pressure in the U.S. as viewers shift to over-the-top (OTT) options. Traditional cable networks are experiencing decreases in subscribers due to cord-cutting and cord-shaving, which has been offset to date by increases in pricing. This can’t continue indefinitely. Television advertising could soon be under siege as marketers direct more funds to digital platforms supplied by Google and Facebook.

Discovery’s management is not complacent about the threats to their business. The company is in the process of acquiring Scripps Networks Interactive, the owner of HGTV and Food Network. The union with Scripps will give the combined firm a 20% share of U.S. cable TV viewership and should make Discovery’s networks more likely to be included in new OTT skinny bundles, which would help mitigate the impact of cord-shaving. Discovery and Scripps own nearly all their own content, in contrast to many other major media companies. This better positions Discovery to go direct to the consumer if legacy cable bundles fracture beyond repair. Discovery has already made inroads into developing more direct “digital” relationships with viewers. The company’s TV Everywhere apps are helping mitigate advertising pressures, Discovery and Scripps own popular online content targeting millennials, and the company currently offers multiple streaming services in Europe, including what they believe is a nascent “Sports Netflix.” Additionally, networks like Discovery Channel and HGTV mainly feature unscripted programming, which competes for eyeballs less directly with services like Netflix that specialize in big-budget scripted fare. Discovery is present in over 220 countries and derives 47% of revenue from international regions. The company’s content travels well and the exposure to less mature overseas markets helps hedge the business model against the rapidly changing U.S. Pay TV landscape.

Discovery’s stock dropped 40% after announcing the Scripps acquisition in July and disclosing greater-than-expected declines in U.S. subscribers. The Select Fund owned Scripps when the takeover announcement was made. The Scripps purchase will stretch Discovery’s balance sheet to Net Debt/EBITDA of 4.6x, but management intends to quickly deleverage. Insiders such as billionaire John Malone have been loading up on shares for the first time in Discovery’s history as a public company. Discovery was trading for less than 7x expected free cash flow when we purchased the name in November, and the stock rebounded as the year closed out.

We’ve gandered at Net 1 UEPS once or twice before, since it has historically traded at a low EBIT multiple. However, our looks were always superficial, and we were scared off by the firm’s outsized exposure to the South African government. Like Transformers, with UEPS there’s more than meets the eye. While UEPS derives significant cash flow from distributing welfare payments in South Africa and has been informed it is losing this contract, management is adamant that the company’s payment technology and infrastructure will have enduring value for other applications in the country and elsewhere. More importantly, UEPS has an interesting portfolio of other assets, including KSNET, one of the largest card payment processors in South Korea. The value of KSNET and UEPS’s investment portfolio could exceed the company’s market capitalization, even assuming the firm’s South African assets are worthless.

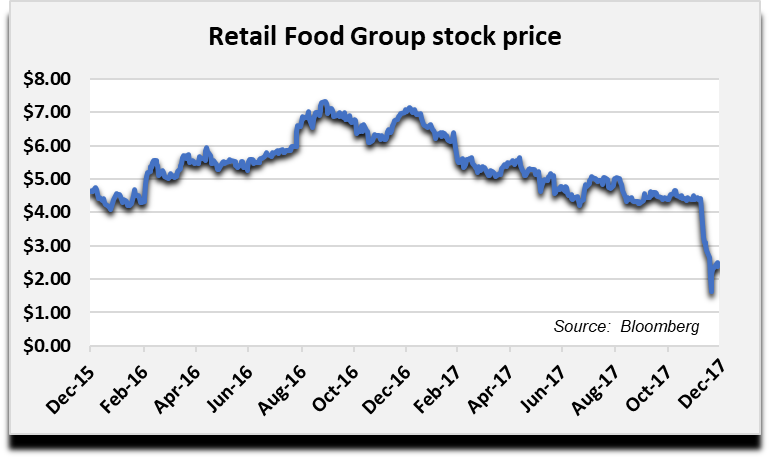

Retail Food Group (RFG) is an Australian franchisor of quick service restaurants. The heavily-shorted shares plunged 63% from December 8th to December 20th after a series of newspaper articles trashed the company and its treatment of franchisees. Three different members of Intrepid’s investment team have previously independently researched RFG, but the price never met our margin of safety.

Franchise businesses are usually good businesses. They often generate copious free cash flow and are frequently awarded high multiples by investors for the stability inherent in the franchise model. In the U.S., Dunkin’ Brands trades for 18x EBIT. RFG was selling below 6x estimated forward EBIT when we bought it. RFG’s franchises sell donuts, other baked goods, coffee, and pizza. The firm also owns wholesale operations for coffee, cheese, and bakery products. Some of the franchise concepts are struggling, and the hostile press coverage claimed that a disproportionate number of RFG franchisees are trying to sell their stores compared to other franchise concepts. Our analysis indicates that the reporters exaggerated their claims. RFG may need to take steps to improve its relationship with franchisees, but we don’t see this business disintegrating at the rate implied by the stock action. Donut King and Gloria Jeans are strong brands in Australia, and a meaningful proportion of the company’s value is tied to these franchises and RFG’s wholesale operations. We entered our position near the lows, and the stock has recovered some lost ground already.

The Fund exited its position in Dominion Diamond (ticker: DDC) during Q4 after the completion of Dominion’s takeover by The Washington Companies. We did not completely sell out of any other holdings. Nevertheless, the Fund owns several names that are fully valued and are candidates for disposal when we find a better opportunity. Unlike other products managed by Intrepid Capital, the Fund aims to be 90% invested. It hasn’t been easy. We must weigh the tradeoffs between holding fully valued names we know well, increasing weightings in stocks we think are undervalued, or purchasing new securities for which we haven’t finished our research. Despite our self-imposed cash constraint, our goal is to deliver to you, our shareholders, a differentiated investment product.

The Select Fund’s main contributors in the fourth quarter were Syntel (ticker: SYNT), Teradata (ticker: TDC), and Retail Food Group. Syntel’s shares rallied after the company reported third quarter earnings. Revenue increased sequentially even with an ongoing drag from American Express, and margins were better than expected. Excluding American Express, Syntel’s sales increased 3.1% year-over-year and 3.7% on a sequential basis. Revenue defined as “digital” was up 18% from Q316. While the third quarter report was a positive surprise and management revised guidance higher, the forecast still suggests a weak Q4. We don’t know whether management is sandbagging or if fourth quarter performance will deteriorate. We reduced our holding since the shares no longer offer an attractive discount, in our view.

Teradata’s better-than-expected third quarter earnings helped push the shares higher. The company’s recent performance broke from a multiyear trend of disappointment. Recurring revenue increased 8% in the quarter and now comprises over half of total revenue. Nevertheless, total revenue was still down 5% year-over-year, and Teradata’s reported profitability leaves much to be desired. We believe management will need to show continued progress toward their long-term free cash flow targets in order for the stock to continue performing.

The main detractors from Q4 performance were Corus Entertainment (ticker: CJR/B CN), Oaktree Capital (ticker: OAK), and Dundee Corp. (ticker: DC/A CN). Canadian equities were less ebullient than their U.S. counterparts in 2017, but Corus and Dundee’s share prices underperformed local benchmarks. Corus delivered improved results in fiscal 2017 compared to the prior two fiscal years, as the firm succeeded in stabilizing advertising revenue. Nevertheless, the company’s ad results were slightly below expectations, and management has cautioned that the outlook for television advertising in Canada remains soft. Corus is holding its own in a tough environment and trades at a 10% dividend yield, but even this low valuation cannot withstand a resumption of top line declines. Corus and other TV network owners must work quickly to implement technology to deliver targeted advertising and more flexible viewing options to defend against the onslaught from over-the-top services. We’re watching closely.

January 10, 2018 update: Corus just reported a 4% decline in television advertising revenues for its fiscal first quarter despite easy comparisons from the prior year. These results were significantly worse than management telegraphed shortly before the fiscal quarter ended, which further reduces their credibility. While the shares trade for a low multiple of cash flow, we have lost confidence in the revenue stabilization story. We believe management and the board overemphasize dividends at the expense of debt reduction. We sold our position at a loss.

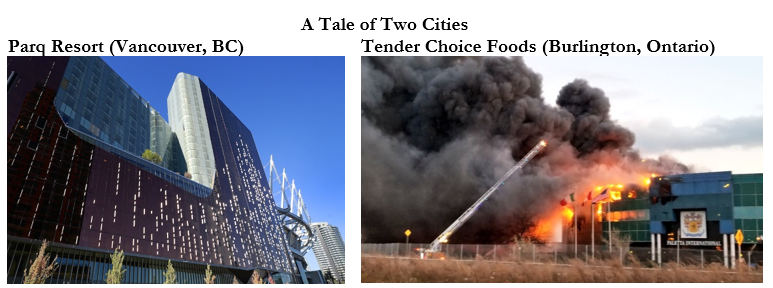

Dundee achieved two important milestones in the third quarter, including closing the sale of United Hydrocarbon (UHIC) to Delonex Energy and opening the Parq Vancouver casino and resort. The UHIC deal eliminates a $12 million annual cash drag to Dundee and offers the potential for a future royalty tied to Delonex’s Chadian oil production several years from now. Parq Vancouver is Dundee’s main opportunity for near-term cash flows, although this is dependent on refinancing the project’s prohibitively expensive construction debt. We believe Dundee should capitalize on the strong market for Vancouver hotel transactions and sell the two hotels attached to Parq Vancouver, with proceeds applied to reducing borrowings.

Just when Dundee’s situation seemed to be incrementally brightening, the company reported in November that it suspended activities at Blue Goose’s Tender Choice chicken processing facility to address repairs required by the Canadian Food Inspection Agency. Weeks later, the facility burned down. While destructive fires are unpredictable (usually, and hopefully in this case), Dundee’s original rationale for purchasing Tender Choice wasn’t strong. Management claimed Tender Choice would help Blue Goose expand its organic brand into conventional chicken and they also suggested vertical integration synergies, but the main purpose was to acquire EBITDA to dilute losses at the Blue Goose subsidiary. This is another disappointing example of capital allocation by Dundee’s leadership. With that said, Dundee’s stock already reflects nothing favorable, as it’s trading at less than 25% of tangible book value. If management can begin extracting cash flow from Parq Vancouver in 2018, Dundee could partially stem its ongoing bleed in book value. Dundee is one of the Fund’s smallest positions.

Oaktree Capital’s shares fell during Q4. Core operating results were reasonably stable when the company reported in November. Incentive income was below last year’s level, although this category is lumpy. Oaktree has a significant amount of undeployed capital as it awaits better opportunities for distressed debt. High yield spreads remain tight and yields on C-rated debt are roughly half the level from their early 2016 peak. We like Oaktree’s countercyclical features and expect them to remain intelligent allocators of investor capital.

Thank you for your investment.

Sincerely,

Jayme Wiggins, CFA

Chief Investment Officer

Intrepid Select Fund Portfolio Manager