October 3, 2017

Dear Fellow Shareholders,

Global financial markets continued to appreciate nearly unabated in the third quarter ended September 30, 2017. Nearly every major asset class posted gains in the period. The most followed U.S. stock indexes garnered mid-single-digit returns. Major fixed income indexes posted more modest gains in the low-single-digits. The markets have experienced historically low volatility as stocks notch record after record. By the end of September, the S&P 500 reached 41 straight weeks without moving up or down by more than 2%. There are only two periods with longer streaks; the mid-1960s and the mid-1990s.[1]

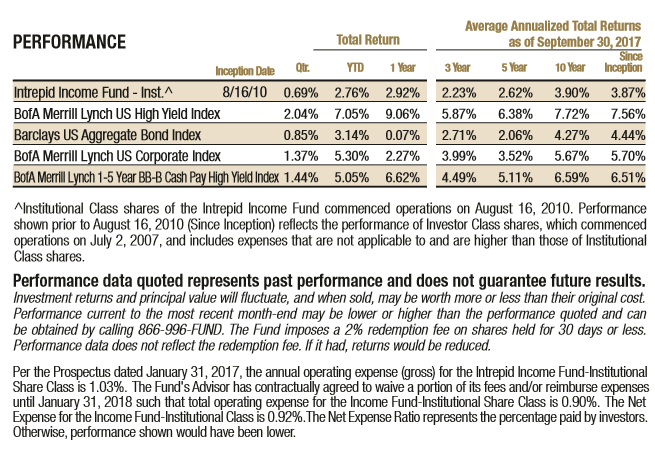

The yield curve shifted slightly higher across most tenors, but the move was more pronounced at the front end of the curve as the probability of a December 2017 rate hike increased. Treasuries provided positive returns despite higher interest rates. The Bloomberg Barclays US Aggregate Bond Index, which represents the broader U.S. investment grade bond market with roughly 9,500 bond issues, returned 0.85%. Exposure to credit risk was rewarded in the quarter. Corporate bond spreads across all ratings tightened in the quarter, and lower-rated bonds generally outperformed. The BAML U.S. Corporate Index, which comprises investment grade corporate bonds, returned 1.37% in the quarter. The BAML High Yield Index rose 2.04%, and the BAML 1-5 year BB-B Index, which we believe is most representative of the Intrepid Income Fund’s (the “Fund”) investment style, increased 1.44%.

In contrast, the Fund returned 0.69%. The Fund’s cash and Treasury bills allocation, which averaged about 15% of assets in the quarter, was partially responsible for the performance drag. Additionally, approximately 38% of assets were held in short-term investment grade corporates, which underperformed longer-duration issues. Our strategy has always been to focus on making calculated credit bets while minimizing interest rate risk, hence our short-duration posturing. High-yield rated corporates accounted for roughly 30% of the portfolio, most of which were BB-rated issues. Our high-yield positioning has been very defensive as yields have been near all-time lows, which also contributed to the underperformance. It’s also important to note that a large number of the Fund’s holdings are not included in our primary benchmarks. In the third calendar quarter, the Fund’s largest contributors were Regis’s 5.5% notes due 12/02/2019 (ticker: RGS) and Consolidated-Tomoka Land’s 4.5% convertible notes (ticker: CTO), both of which are discussed below. There were no material detractors in the quarter.

Several of our short-duration investment grade holdings matured in the quarter ended September 30, 2017. Only one core high-yield position was called; Sally Beauty’s 5.75% notes. We sold the remainder of our Dominion Diamond stock after the previously announced buyout offer from The Washington Companies was increased. Our purchase activity was mostly limited to new short-term investment grade holdings and additions to existing positions. We purchased two new high-yield issues that are likely to be called in the near-term, and therefore aren’t worth detailing here, but we expect our initial work on these two companies to pay dividends as both are likely to be high-yield issuers for the foreseeable future.

The Fund’s fiscal year ended on September 30, 2017. In the twelve-month period, the Income Fund returned 2.92%. The Barclays US Aggregate and the BAML US Corporate Index returned 0.07% and 2.27%, respectively. The BAML High Yield Index increased 9.06%, and the BAML 1-5 year BB-B Index rose 6.62%. The largest contributors to the Fund’s performance in the fiscal year were the lawsuit settlement payment from Cash America received in January, Corus Entertainment’s common stock (ticker: CJR/B CN), Consolidated-Tomoka’s convertible notes, and Dominion Diamond’s common stock (ticker: DDC). The most significant detractors in the fiscal year were Primero Mining 5.75% due 2/28/2020 (ticker: PPPMF) and our positions in two Rent-A-Center bond issues (ticker: RCII). There were no other material detractors.

Last year we owned the bonds of three different publicly-traded pawn shop operators – EZCORP (ticker: EZPW), Cash America (ticker: CSH), and First Cash Financial (ticker: FCFS). First Cash acquired Cash America in September 2016 and retired the Cash America bonds at a significant premium as required by the make-whole covenant. At the time, Cash America and a bond investor were engaged in a long-running lawsuit related to the retirement of $103.5 million of the notes after Cash America spun off an online lending business in 2014. Despite the notes being non-callable at the time, CSH did not pay a make-whole premium on this partial retirement. Summary judgement was completed on September 19, 2016, and the judge ruled in favor of the bondholders. The only disagreement was the amount of compensation that would be awarded to bondholders. After several short delays, the parties came to an agreement. On January 13, 2017, the Fund received payment of the settlement proceeds.

Consolidated-Tomoka is a Florida-based owner of office and retail income producing properties located across the United States. It also owns several thousand acres of undeveloped land near I-95 in Daytona Beach, which it has been monetizing over the past few years. The notes pay a reasonable 4.5% coupon to the March 2020 maturity and are also convertible into common stock. We believed the yield offered by the bonds was attractive before considering the value of the convertible option. Nevertheless, the option contributed to the Fund’s performance in the fiscal year as CTO’s shares have appreciated materially since our purchase of the bonds.

The Fund’s largest position is Regis Corp.’s 5.5% notes. We have been a lender or equity owner of the company on several occasions in the last ten years. Regis is the country’s largest owner and franchisor of hair salons. The most recognizable banners are Supercuts, MasterCuts, and SmartStyle/Cost Cutters locations in Wal-Mart stores. Regis has struggled over the last several years, and management turnover has been high as the company continues to search for skilled turnaround executives. Nevertheless, we continue to believe the notes offer an attractive risk-adjusted yield with a very short duration. While the company has performed poorly operationally for some time, the balance sheet remains very clean.

Dominion Diamond (ticker: DDC) is the world’s third largest diamond producer. The company owns interests in two mines located in Canada, which is one of the most stable political jurisdictions in the world. While the diamond industry is not recession-resistant, the long-term supply and demand fundamentals appear to be supportive of prices. Diamond mines can take over a decade to construct from start to finish, which tends to stabilize the supply side of the equation. Furthermore, because just four producers account for roughly 75% of global production value, the industry has historically been quite rational in pulling back supply in the face of weak end-market demand. The firm has a very strong balance sheet that includes a large cash balance and sizeable inventory of diamonds. Shortly after we purchased the shares, Dominion received an unsolicited buyout offer at a 36% premium to the prior closing price.

Our investments in two bonds issued by rent-to-own operator Rent-A-Center (ticker: RCII) detracted from the Fund’s performance in the fiscal year. We trimmed the positions late in calendar 2016 and exited completely in early 2017 when the business started to deteriorate significantly. Rent-A-Center’s issues at first appeared to be transitory, but subsequently the business did not improve as we expected. Readers can find more commentary on our view in the Fund’s Q117 commentary. Primero Mining’s 5.75% convertible notes were the largest detractor in the twelve months ended September 30, 2017. We invite readers to review the Intrepid Endurance Fund’s quarterly commentaries for more detail on Primero. Portfolio manager Jayme Wiggins distills the situation with much more clarity than I can hope to provide.

Over the past few quarters we have reported on a number of specific events or securities that appeared to indicate excessive risk-taking behaviors. We wish we could report to you that some level of normalcy has returned to the financial markets, but unfortunately that isn’t the case. Consider the following recent bond issuances:

- Austria issued 100-year bonds that pay 2.1% annually.

- Tesla secured a 5.3% coupon on its $1.8 billion B- rated bond issue due in 2025. This is the lowest coupon ever for its maturity and rating. The company is expected to burn $3.3 billion in cash in 2017.

- HD Supply Waterworks, a distributor of water, sewer, and fire protection products, was able to issue bonds at a coupon lower than the firm’s leverage ratio. The bond received orders that totaled ten times the size of the offering.

These are just a few of many instances where downside risks appear to be completely ignored. Most fixed income subsectors are offering the lowest spreads since 2007. Absolute yields are at or near record lows. Nevertheless, there is evidence that credit qualities are deteriorating. Covenant quality, as measured by Moody’s, is near the weakest on record. Corporate leverage ratios are extended beyond levels experienced before the credit crisis. In fact, a recent study concluded that 80% of large corporations have debt-to-EBITDA ratios above 4x, and half have debt-to-EBITDA ratios greater than 5x. In addition, recent recoveries on defaulted bonds have been lower than historical levels, a condition we believe could continue and lead to larger capital impairments than in past cycles.

It should not come as a surprise when we say we are having difficulty discovering securities that offer adequate risk-adjusted yields. We will not deploy your capital into high-risk securities promising just a few percentage points in annual returns. In the absence of attractive opportunities, the Fund will continue to hold Treasury bills and short-term investment grade bonds. We are diligently searching for pockets of value in what may be under-explored corners of the market, including bonds with small issue sizes, convertible bonds and preferred stock. Thank you for your investment.

Sincerely,

Jason Lazarus, CFA

Intrepid Income Fund Portfolio Manager

[1] “Could this be the Least Volatile September Ever?” LPL Financial Research. 27 September 2017. Web.