July 5, 2017

Dear Fellow Shareholders,

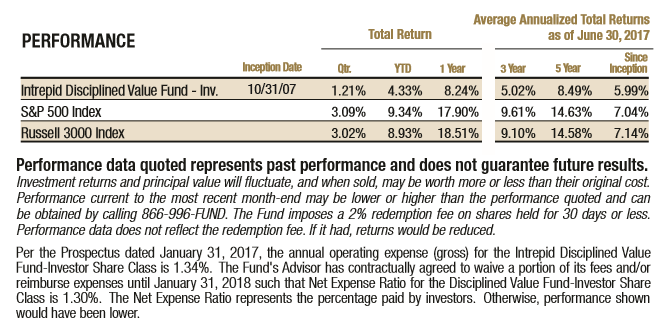

I am pleased to report the performance of the Intrepid Disciplined Value Fund (the “Fund”) for the quarter, year-to-date and trailing one-year periods ended June 30, 2017. For the quarter, the Fund increased 1.21%, which brings the year-to-date return to 4.33% and the trailing one-year return to 8.24%. The Fund’s annualized return for the trailing five-year period is remarkably similar at 8.49%. For comparison, the returns of the S&P 500 Index and the Russell 3000 Index for quarter ended June 30, 2017 were almost identical at 3.09% and 3.02%, respectively. For the year-to-date period, the S&P 500 Index and the Russell 3000 Index returned 9.34% and 8.93%, respectively. For the trailing one-year period, the S&P Index and the Russell 3000 Index increased 17.90% and 18.51%, respectively.

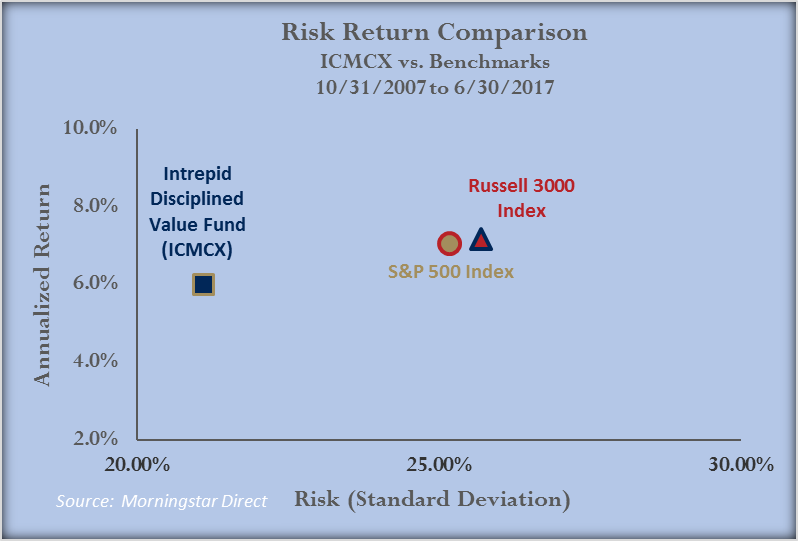

In our attempt to deliver a consistent process and exceptional risk-adjusted returns over a full market cycle, we are challenged in the current environment as we continue to confront high equity prices. As shareholders invested alongside our clients, our goal is to preserve your capital as well as our own. As shown in the chart above, the risk metrics of this Fund indicate we have taken materially less risk compared to the indices. We do this by focusing on our bottom-up valuation process and searching for high-quality businesses that we believe are mispriced using conservative valuation techniques. At this stage in the economic cycle, with a headwind of high equity prices – trailing price-to-earnings (P/E) ratio of 21 for the S&P 500 Index as of June 30, 2017 – cash in the Fund of 44.4% is reflective of the difficulty we are having in finding qualifying investments.

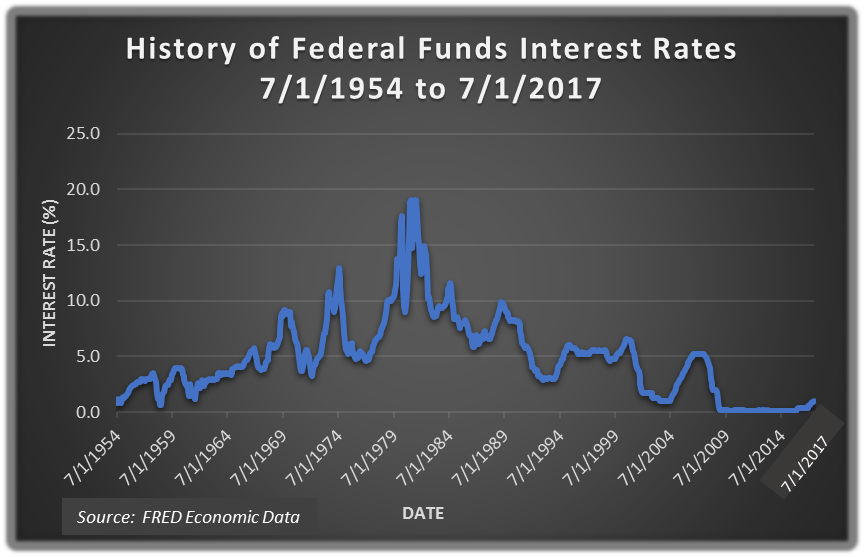

Prior to the financial crisis and the Fed’s long-term suppression of interest rates (see chart below), we were in some instances able to deploy cash reserves and earn ~3-5% nominal returns on the balances. It has only been since December of 2016, with central bank rate suppression activity maybe, ever so slowly, coming to an end, that we believe investing these balances in Treasury bills has become a worthwhile endeavor again.

From our perspective, interest rates are a price, and frankly, one the marketplace could easily set without the machinations of the Federal Reserve, European Central Bank, or the Bank of Japan. To use an analogy, just think of trying to diet by stepping on a scale every morning to help guide your dietary intake as well as your caloric output through exercise. Except every time you step on the scale, someone sneaks up behind you and presses their toe on the scale! I believe the distortions in the financial markets are much more widespread and consequential than a dieter becoming discouraged from a misreading of the bathroom scale. When the “Fed” and other central bankers take their “toe off the scale” and equity prices adjust to a more normalized interest rate environment, we anticipate utilizing the cash in the Fund to take advantage of buying opportunities.

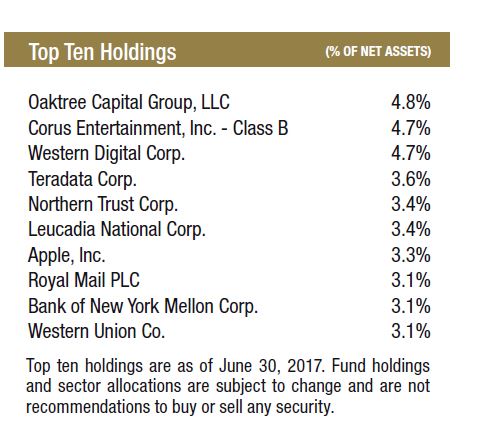

The Fund’s five largest contributors during the quarter were Western Digital (ticker: WDC), Corus Entertainment (ticker: CJR/B CN), Northern Trust (ticker: NTRS), Coach (ticker: COH), and Bank of New York Mellon (ticker: BK). The Fund’s five largest detractors for the quarter were Dundee Corp. (ticker: DC/A CN), Verizon (ticker: VZ), Teradata (ticker: TDC), Alamos Gold (ticker: AGI), and Patterson UTI (ticker: PTEN).

Thank you for your continued support and investment in the Fund. If there is anything we can do to serve you better, please don’t hesitate to contact us.

Best regards,

Mark Travis

President

Intrepid Disciplined Value Fund Portfolio Manager