July 5, 2017

Dear Fellow Shareholders,

Global markets continue to be influenced by many of the same themes we have discussed in these letters in recent periods. Namely, the incessant search for yield, persistently low energy prices, and the impact of e-commerce on a variety of industries – in particular, brick and mortar retailers. The culmination of yield-seeking behavior might have occurred in June, when Argentina was able to sell $2.75 billion of 100-year bonds. The country has defaulted on its debt five times in the last 100 years, most recently in 2014! Nevertheless, the issuer received orders totaling $9.75 billion. The search for yield was not restricted to just the western hemisphere. Across the Pacific, Australian bank Macquarie offered a $750 million bond that was oversubscribed by 16 times, meaning $12 billion in total capital was chasing after the deal.

Energy and traditional retailing are two of the very few areas of broad concern to investors. The fears appear to be justified, so far. In our last letter, we highlighted several well-known retailers that were forced to declare bankruptcy, and we noted that more pain was on the horizon. The second quarter claimed more casualties, including Sears Canada, Payless Shoesource, rue21, and Gymboree. These operators plan to close stores and shed debt, but will attempt to continue operating after emerging from bankruptcy. Other management teams have concluded that liquidation is the only option. Gordman’s and bebe are closing all of their stores, joining hhgregg, The Limited, and Wet Seal.

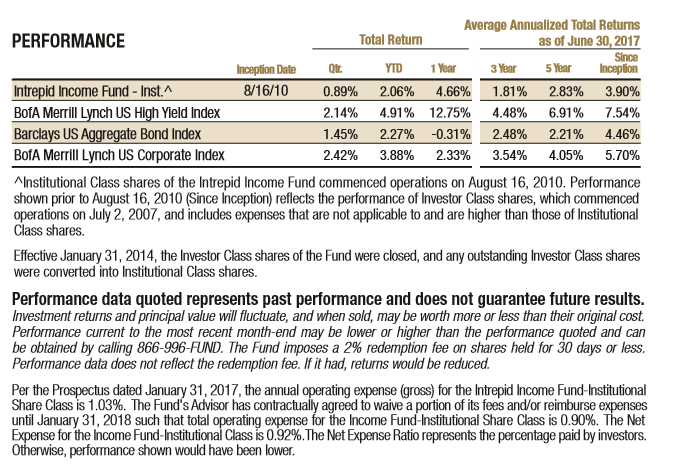

Markets mostly performed well outside of energy and retail. Fixed income securities generally provided positive returns in the second quarter despite the Federal Reserve’s second rate hike this year. Longer maturity Treasury bond yields actually declined, which produced a tailwind to fixed income securities. The yield on the ten-year U.S. Treasury note declined slightly from 2.39% to 2.31%. The 2.25% Treasury note maturing on 2/15/2027 gained 0.74%. Investment-grade bonds, as measured by the Bloomberg Barclays Aggregate Bond Index, gained 1.45% in the quarter. Credit put in a very strong performance, with the BofA/ML US High Yield Index gaining 2.14% in the quarter ended June 30, 2017. High yield returns were bested by investment-grade credit. The BofA/ML US Corporate Index returned 2.42% in the second quarter.

The Intrepid Income Fund (the “Fund”) rose 0.89%. The Fund focuses on taking calculated credit risks while attempting to minimize credit risk, so our holdings did not benefit from lower rates in longer duration securities to the same extent as the indexes quoted above. Additionally, our holdings have typically been higher-quality, and therefore do not usually rise as much in a strong “risk-on” period. In the second quarter, short-term investment grade bonds averaged roughly 37% of the Fund’s assets, and Treasury bills averaged another 13%. Less than half of the Fund is invested in high-yield or unrated securities.

The top contributors to the Fund’s performance in the second calendar quarter were Corus Entertainment common stock (ticker: CJR/B CN), Consolidated-Tomoka Land Company convertible notes due in 2020 (ticker: CTO), and EZCORP convertible notes due in 2019 (ticker: EZPW). There were no material detractors in the quarter.

Corus’s share price rose after the company reported earnings in June. The company’s advertising revenues were flat compared to the prior year, which was a marked improvement over recent quarters. We believe the shares are still undervalued. Corus also pays an 8% dividend.

Consolidated-Tomoka is a Daytona Beach, Florida-based owner of office and retail income producing properties located across the United States. It also owns 8,200 acres of undeveloped land near I-95 in Daytona Beach. The company has been slowly monetizing its raw land and redeploying the proceeds into income-producing properties. The firm issued $75 million in convertible bonds in early 2015 that was partially used to fund purchases of income-producing properties. The notes pay a 4.5% coupon and mature in March 2020. We purchased the bonds late last year. While the equity does not appear significantly undervalued, we believe the yield on the bonds is relatively attractive.

We have been involved with several different pawn shop operators over the last few years. We recently added to our oldest pawn position, EZCORP’s convertible notes due in 2019. Regular readers will recall that we substantially trimmed the position last year after the notes rallied from the low-60s to near par. The bonds performed very well after it became clear to the market that the value destruction occurring in a Mexican payday loan subsidiary could be isolated. Since then, the company was able to divest this subsidiary on favorable terms. Although much of the purchase price will be collected in future years (and will therefore be subject to the credit risk of the acquirer), the deal appears favorable. The notes declined in price recently as the stock sold off, and we were able to repurchase the notes at what we believe to be an attractive price. Last week, the company issued new convertible notes due in 2024 that pay a 2.875% coupon. EZCORP plans to use the proceeds to redeem a very high interest secured loan, and the remainder may be allocated to repurchase a portion of our convertible notes. While the stock fell substantially on the news of the equity dilution, the retiring of the secured loan is a positive event for creditors.

Three of the Fund’s larger positions were called in the second quarter, including the bonds of Alamos Gold and FirstCash Inc.

The bonds of FirstCash (ticker: FCFS) were one of the fund’s largest positions for close to two years. We have discussed the company on several occasions, but to quickly recap, FirstCash is the product of the merger of two large pawn shop operators, First Cash and Cash America. We owned the bonds of both companies before the merger was completed. Our Cash America bonds were repurchased by the company last year. We maintained a large position in the FirstCash notes. We expected the notes to be called earlier this year so the issuer could eliminate some restrictive covenants, which occurred in the last quarter. The company issued new bonds that pay 5.375% and mature in 2024. We participated in new issue, but on a limited basis due to the longer duration.

Alamos Gold (ticker: AGI) unexpectedly issued equity and used the cash to retire our bonds. While we are disappointed that we are no longer a lender after being involved with the company for several years, we believe management made a good decision to issue stock, particularly with respect to the spot price of gold.

We exited the remainder of our position in PHI Inc (ticker: PHII) in the second quarter after several months of slowly trimming the name. PHI owns and operates helicopters for use in the energy and medical industries. The company transports workers to and from offshore oil and gas platforms and also performs medevac flights. The business’s fundamentals have deteriorated significantly over the past six quarters and are likely to get worse. While we believed the company would be able to survive a period of low oil prices, the critical part of the thesis we got wrong is that we did not expect oil prices to remain so low for so long. This has resulted in customers negotiating hard to slash their operating costs, including helicopter transportation. In addition, we underestimated the profitability of a key contract that recently ended, which has further weighed on profitability. While we made money on the investment, we were partially bailed out by yield-hungry investors.

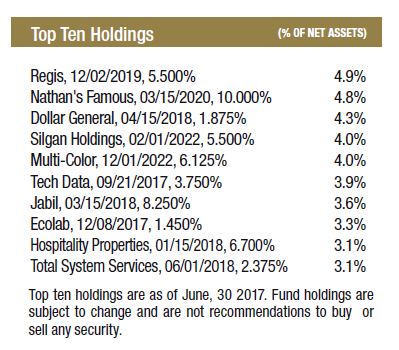

As we have complained for as long as we can remember, it has been very difficult to find suitable income-generating securities to replace our called bonds. We identified only one new core position in the quarter; Silgan Holdings’ 5.5% notes due 2/01/2022. Silgan is a leading manufacturer of metal cans, plastic containers, and closure systems (tops for food and beverage containers). The company was founded in 1987 to acquire the packaging plants of the large U.S. food manufacturers like Nestle, Campbell, and Del Monte. The company has durable competitive advantages in metal cans and closures. In the US, Silgan commands a 60% share of the metal can industry. This share has little risk of competition from current or new entrants, as it costs too much to transport empty cans more than 300 miles from the manufacturing location. Without the means to make the cans themselves, food manufacturers need certainty the containers will be available and correctly made, so 90% of Silgan’s metal can sales are contracted for multiple years with input cost pass-through clauses.

Silgan is a classic Intrepid business: it is a market leader, the business is predictable, and it generates substantial free cash flow. We owned the stock and bonds close to a decade ago. Our own Ben Franklin (now Portfolio Manager of the Intrepid International Fund) was a young analyst when the idea was initially sourced in 2008. This is a good example of how we leverage our body of knowledge across the credit and equity teams. While our opportunity set remains quite limited, we are confident that our diligent searching will continue to unearth attractive investments for our shareholders. Thank you for your investment.

Sincerely,

Jason Lazarus, CFA

Intrepid Income Fund Portfolio Manager