July 5, 2017

“The inherent irony of the efficient market theory is that the more people believe in it and correspondingly shun active management, the more inefficient the market is likely to become.”

– Seth Karman – The Baupost Group

Dear Friends and Clients,

About once every decade I lament the day in college when I finished reading “The Intelligent Investor” by Benjamin Graham, and it clicked as I became an investor devoted to seeking “value.” Well, here I am again, feeling like momentum investors are having all the fun as my patience wears thin waiting for securities that we believe are both safe and cheap. Currently, most of the equity markets appear neither cheap nor safe to us. The momentum investors who are the current subject of my envy seem to only care that prices are going up, downside be damned, and pithy market aphorisms like “Don’t fight the Fed” and “BTFD” (buy the – uh, friendly dip) have worked out swimmingly for the last several years. To me, much of what I am observing in the equity markets is indicative of this momentum mindset, and frankly, why trend-following can work so well, at times.

I accuse most investors of “buying high and selling low” or, in the immortal words of the humorist Will Rogers, “Don’t gamble; take all your savings and buy some good stock and hold it till it goes up, then sell it. If it don’t go up, don’t buy it.” As a student of financial history, it interests me to look back over my lifetime and think about what preceded difficult equity conditions where prices were down 50% or more. In the early 1970s, we had the “Nifty 50” must-own growth stocks. This worked great until the oil embargo of 1973-1974. In the mid-1980s, as I was beginning my career at E.F. Hutton, the hot sale was “portfolio insurance,” which allowed investors to stay completely invested without fear of loss. This “magic” was to happen by selling index futures into a falling market – a nice theory until “Black Monday” in October of 1987 when prices declined 22% in one day.

A decade later, after co-founding Intrepid Capital with my father Forrest in 1995, I watched clients leave to seek their “internet fortune.” Three years after starting the firm, the Munder Net Net Fund and the Van Waggoner Emerging Growth Fund were the investors’ favorites…R.I.P! The Nasdaq Index and the QQQ ETF were the only things to own in 1997, 1998, and 1999, until they weren’t. Lest you have forgotten, the S&P 500 Index actually lost money in 2000, 2001, and 2002. Well, hardly a half decade later, the momentum trade was housing and particularly mortgage-related equities. Very few investors stopped to ask, “Are these mortgages being carelessly underwritten?” If they had, maybe the S&P 500 would not have suffered a 57% decline from October 2007 to March 2009 as the housing bubble burst.

So, where are we today? Anecdotally, I see excess everywhere I look. When I ride my bicycle around my neighborhood in Ponte Vedra Beach, Florida, I pass a different home being demolished every few days, with a new, bigger home being built in its place. When I have the radio on while working in my garage, I hear frequent ads to “come to our real estate seminar to learn how to flip properties.” Snap, Inc. (ticker: SNAP) recently went public with egregious terms (no voting rights) for minority shareholders and no prospect of company profits, at least not any time soon. Last but not least, most money entering the stock market is going into some sort of indexed product, a trend accelerated in small part by government edict via the Department of Labor (DOL) ruling. I suspect that like much of government regulation, we will see once again “the law of unintended consequences,” particularly if we see a sharp contraction in equity prices similar to the ones I described earlier.

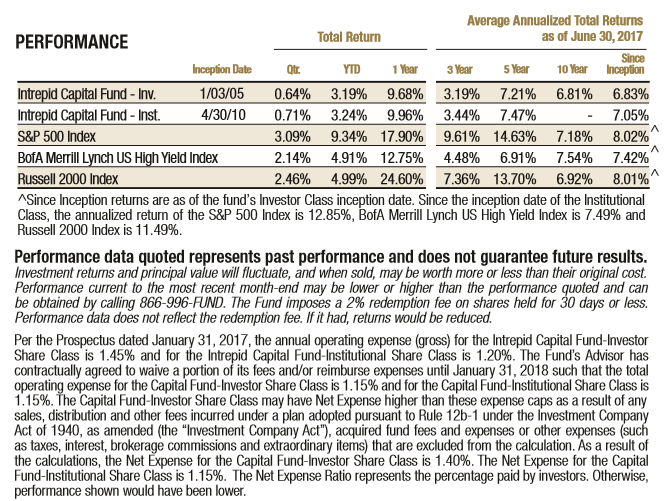

The Intrepid Capital Fund (the “Fund”) increased 0.64% for the second quarter ended June 30, 2017 compared to the BofA Merrill Lynch US High Yield Index and the S&P 500 Index, which returned 2.14% and 3.09%, respectively. Year-to-date through June 30, 2017, the Fund increased 3.19% compared with returns of 4.91% and 9.34% for the BofA Merrill Lynch US High Yield Index and the S&P 500 Index, respectively.

The Fund’s five largest contributors during the quarter were Corus Entertainment (ticker: CJR/B CN), Western Digital (ticker: WDC), Hornbach Baumarkt AG (ticker: HBM GR), Stallergenes Greer (ticker: STAGR FP), and Metka Industrial (ticker: METTK GA). The Fund’s five largest detractors for the quarter were Patterson UTI (ticker: PTEN), Express Scripts (ticker: ESRX), Dundee Corp. (ticker: DC/A CN), Verizon Communications (ticker: VZ), and Teradata (ticker: TDC). Cash in the Fund at the end of the quarter was 18.5%.

In this industry, there is career risk for managers who are “under-invested” in a rising market like the one we find ourselves in today. Not to worry – at this point, I am unemployable elsewhere! Please rest assured that I, along with the employees of Intrepid Capital, are invested alongside you. As you have heard from us many times, we are content to hold cash when we believe compelling opportunities are not present. We continue to seek businesses that can be valued with a high degree of confidence and those we believe to be selling at a discount to our fair value estimate. Our goal is to provide attractive absolute, risk-adjusted returns. We believe the cash present in various amounts in each of our funds to be a sea anchor in a rising market, and a life boat when many investors become fearful and decide to sell. Stay tuned, this could get interesting.

Thank you for entrusting us with your hard-earned capital. It is not a position we take lightly. If there is anything we can do to serve you better, please don’t hesitate to call.

Best regards,

Mark F. Travis President

Intrepid Capital Fund Portfolio Manager