October 3, 2017

“We are what we repeatedly do. Excellence, then, is not an act, but a habit.”

– Aristotle

Dear Friends and Clients,

I recently picked up a copy of Joel Tillinghast’s “Big Money Thinks Small.” Joel is a longtime portfolio manager with Fidelity. I couldn’t help but chuckle when in Chapter 1, “It’s a Mad, Mad World,” Joel outlines what he regards as the crucial steps to successful investing:

- Make decisions rationally

- Invest in what we know

- Work with honest and trustworthy managers

- Avoid businesses prone to obsolescence and financial ruin

- Value stocks properly

The reason for my chuckle is that Mr. Tillinghast, in his five bullet points, outlines almost exactly what we attempt to do at Intrepid Capital, and more specifically for the purposes of this letter, in the Intrepid Capital Fund (the “Fund”). These principles might seem like a no-brainer, but you’d be surprised how many professional investors fail to consistently follow them, in my opinion. As I once heard it said of commodity trading, “The rules are very simple. Following the rules, however, is very difficult.”

One reason it’s so difficult is that the market doesn’t consistently recognize or reward investors who try to adhere to such a philosophy. I would love to add “earn consistently high returns” as a sixth bullet inherent to our investment process, but there are periods when behavior that goes directly against the five rules seems like the profitable path – irrational decision making is rewarded, buyers of arcane and complex strategies seem to reap all the profits, honest and dishonest managers are treated alike by the market, unsustainable businesses are propped up by cheap debt, and valuing stocks seems to be a fruitless exercise.

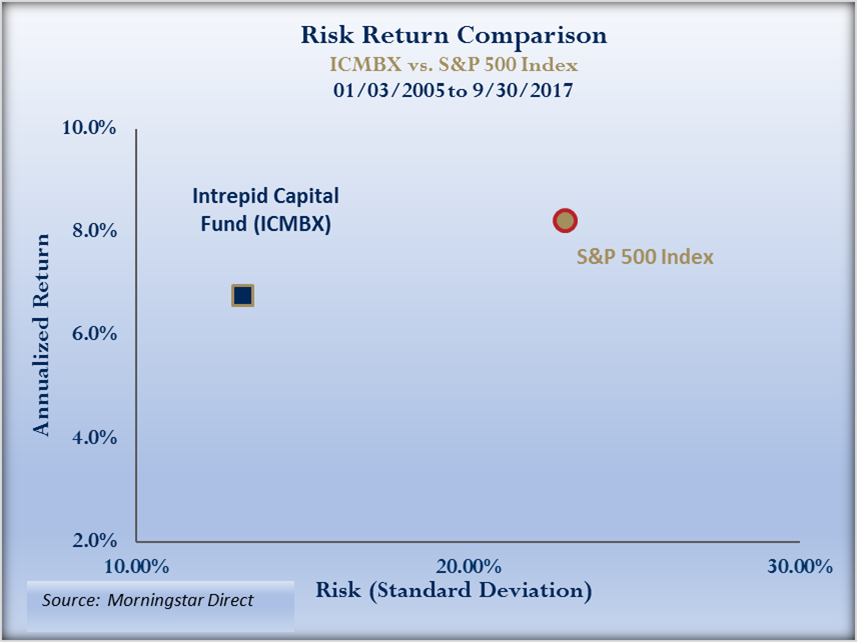

These are the times when following the rules can be very difficult indeed. As the portfolio manager of the Fund, I am attempting to deliver equity-like returns with substantially less risk than an equity index. Since inception on 1/3/2005, we have been able to deliver on that value proposition as shown in the chart below.

I am always amazed at the short-term mindset of the average mutual fund investor. There is a great mismatch in this industry between the underlying term of different asset classes and the time horizon of investors in those asset classes. For instance, many yield seekers today are content to treat a high yield bond index, such as the well-known BofA Merrill Lynch US High Yield Index (the “Index”), as a nearly risk-free money market substitute in which they can put cash to work for a few months (or less). This may seem like a low-risk strategy to earn a little extra yield, but the securities that make up the Index are markedly riskier and longer-term in nature. The average bond in the Index is 6.3 years away from maturity, and the average issuer has a single B credit rating, according to Merrill Lynch, which is how Standard & Poors classifies a company that currently has the ability to meet its financial obligations but is vulnerable to defaulting if business or economic conditions worsen.[1] That combination of both interest rate risk and credit risk doesn’t strike me as the characteristics of a short-term, cash equivalent investment.

Even more egregious than that, I’ve recently heard other investment managers[2] tell stories of clients asking if they should “park some money” in the S&P 500 for a few months. For most of the last 100 years, such a blasé mindset toward stock market risk would have been unheard of. But when the S&P has averaged a 14.2% return over the last five years and has gone almost a full year without a 3% drawdown (as of this writing, only 7 days shy of the longest such run in history), and when investors’ expectations of the future are naively based on the last few years, it’s natural for such myopic behavior to become popular again.

While we are of course mindful of short-term performance, we are much more interested in how we look over the trailing 10 years. I can hear many of you now: “That’s a nice thought Mark, but we will give you three years!” Yes, that is unfortunately the time horizon over which most performance is evaluated and money is allocated in this business. I like 10 years because it is more likely to encompass a full market cycle of both a bullish phase and a bearish phase. Full market cycles are the time horizon we focus on at Intrepid and the time frame over which we think all investment managers’ performance should ideally be measured. Truthfully, it doesn’t take excessive skill to passively ride a bull market; a skillful manager should be able to participate in an up market while also protecting and preserving capital in a down market.

In contrasting our Tillinghast-esque philosophy to current market thinking, I have marveled for quite some time at the cult-like status of both Elon Musk and his electric car company Tesla. Wall Street analysts expect Tesla to sell 121,000 cars this year (they sold 76,000 last year). This level of production will generate an expected 2017 pre-tax loss of $1.4 billion (with a “B”), and next year’s loss is forecasted at a mere $550 million. The company will likely have to continue tapping the capital markets for funding until they reach a break-even level of production, which Wall Street believes will happen in 2019.

To clarify, I’m not disparaging Mr. Musk or the company itself, but rather the market’s collective decision to value such a cash-burning enterprise at almost $66 billion and to price its recent oversubscribed debt issue ($1.8 billion of 8-year senior notes) at a 5.25% yield, which is an all-time record low for a B- rated issuer. To me this seems to violate, at a minimum, rule #1 above. Personally, if I were a creditor of a small, unprofitable electric car manufacturer with large, entrenched, deep-pocketed competitors and an uncertain growth runway, I would demand a much higher return than 5.25% to compensate for the chance that I might not be paid back..

On the flip side, going back to Mr. Tillinghast’s Rule #2 (invest in what you know), I present the Regis Corporation 5.5% notes due 12/2/2019. Regis is a company we know well, as we at times have owned both their equity and their debt. Regis is in the business of giving haircuts, and I frequent my local Supercuts, one of Regis’ brands.

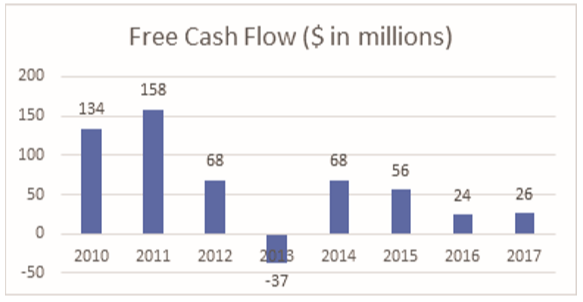

These bonds also satisfy Rule #4 (avoid businesses prone to obsolescence and financial ruin), as obsolescence is highly unlikely to occur for Regis between now and when this bond matures in December 2019. The company’s operations are generating positive free cash flow (see below), and the most recent filings disclose $172 million in cash available to cover its $121 million in debt. Despite these favorable credit conditions, the bonds offer a yield of 5.5% to maturity – an attractive premium to that offered by Treasuries considering the risk assumed. Based on my past attempts to shear my own hair and the unlikely event that this business is “Amazoned,” I feel more comfortable about the return of my principal in Regis than I would in Tesla.

Regis Corp

Source: Company filings

In summary, be rational, invest in what you know, and be careful with speculative business investment. Our process is built around these principles. I believe that by following this process, we will deliver attractive risk-adjusted results over a full market cycle (>10 years).

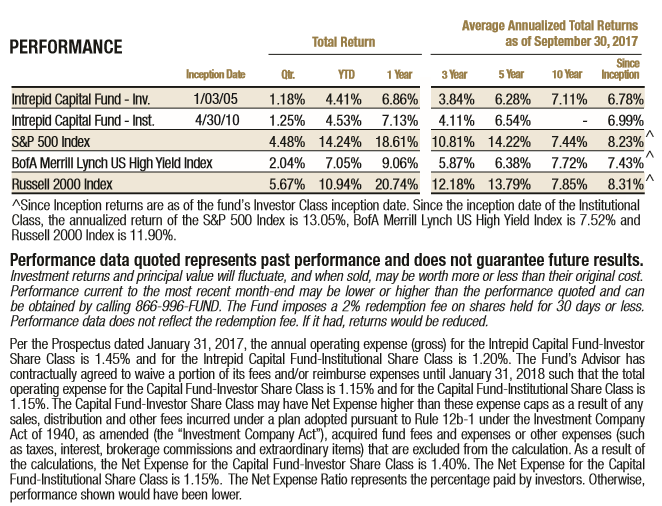

The Intrepid Capital Fund ended its most recent fiscal year on September 30, 2017 with a return of 6.86%, which is just a hair ahead of the since inception result of 6.78%. The Fund ended the fiscal year with a mix of 46% in equity, 33% in debt, and 22% in cash or T-bills. Coincidentally, the mix in the Fund was similar at the end of the prior fiscal year, with 49% equity, 29% bonds and 22% in cash. The Fund’s defensive cash holdings have muted its recent performance, but the securities we invest in have yielded very competitive results. For the fiscal year, the Fund’s equity holdings were up 12.14% and fixed income securities returned 4.39%. Since inception annualized returns of 11.59% for equities and 6.79% for fixed income bear similarly compelling testimony to the strength of our research and security selection.

This performance compares unfavorably to the rapidly rising S&P 500 and Russell 2000 equity indexes over the last three months. As they say of the weather in Florida, “Stick around, that will change.” The since inception performance is closer to the blended indexes consisting of stock and bonds. In almost every case, we are attempting to take less risk.

As for the quarter ended September 30, 2017, the Fund’s five largest contributors were Syntel (ticker: SYNT), Teradata (ticker: TDC), Verizon (ticker: VZ), Dominion Diamond (ticker: DDC), Berkshire Hathaway Class B (ticker: BRK/B). The Fund’s five largest detractors for the quarter were G.U.D. Holdings (ticker: GUD AU), Baldwin & Lyons (ticker: BWINB), Royal Mail (ticker: RMG LN), Patterson UTI Energy (ticker: PTEN), Leucadia National (ticker: LUK).

Thank you for entrusting us with your hard-earned capital, it is not a position we take lightly. If there is anything we can do to serve you better, please don’t hesitate to ask.

Best regards,

Mark F. Travis President

Intrepid Capital Fund Portfolio Manager

[1] “S&P Global Ratings: RatingsDirect.” Standard and Poors. August 18, 2016. Web. 12 October 2017.

[2] Bilello, Charlie. “Is the S&P the New Money Market?” Pension Partners. October 2, 2017. Web. 12 October 2017.