January 9, 2020

Dear Friends and Clients,

This letter always causes me to stop (however briefly!) and reflect on the past, whether it is the most recent quarter, the past year, 5 years, 10 years, etc. In today’s case, it is a much deeper reflection looking back on 25 years since cofounding Intrepid Capital with my father, Forrest. We celebrate our firm’s 25th birthday this month.

I sit here today as a 58-year-old, having spent my entire working career in the investment management business; it will be 36 years this summer. At the time I started the firm, I fled a high paying job, up the freight elevator in the now Bank of America tower in downtown Jacksonville, despite a wife at home with our first of two children (who was just 1 year old). I left with the simple idea of creating something better for our clients; a place where my team and I would coinvest with clients, on identical terms as fiduciaries.

Despite an environment that has been challenging for asset management companies, in my opinion, this firm has survived and thrived for the last 25 years for two reasons: 1) a philosophy of balancing both risk AND reward to obtain optimal results for our clients, and 2) staying steadfast to that philosophy despite short-term market conditions.

I named the firm Intrepid Capital after Ted Turner’s America’s Cup sailboat. The name implies it is not for the faint of heart. This is not to say that I was going to openly embrace risk; I wasn’t then and I’m not now. The name to me was more centered around the necessity to look different than our peers, sometimes for the better and sometimes for the worse. While I can proudly show a long-term track record, the last five years have been humbling.

Said another way, Intrepid has been successful for clients long-term because it has been willing to look different than the typical money manager – often in a way that meant managing risk more closely when conditions warranted, but at times increasing risk when we saw it as favorable for long-term client outcomes. As a result, I have oftentimes thought of myself as a “Risk Manager” just as much as a “Portfolio Manager.”

Unfortunately, over the last five years, our philosophy of managing risk while seeking reward has not kept up with strategies that can be characterized as “highly risk-seeking.” We are not proud of our underperformance over this period and are taking aggressive steps to address it. But we also want to emphasize that – over our 25 year history – we have been through periods like this before, and have come through them with our clients in a stronger place each time by remaining focused on risk. Our 25 years of experience covering several market cycles suggests that portfolio managers are like pilots in that “There are old pilots, there are bold pilots, but there are no old bold pilots.”

This does not mean we are standing by and simply waiting for market trends to turn in our direction. We remain hard at work finding attractive opportunities – based on a balance of risk AND reward – for the capital you entrusted to us. This past year has been especially fruitful in that sense, as we purchased more new ideas in 2019 than we have in many years. We attribute this increased activity to the same spirit of continuous process improvement we have employed over the past 25 years and are particularly excited about our most recent process tweaks based on early results.

We look forward to Intrepid’s next 25 years of navigating through the constant change in the markets. We are thankful for our clients’ trust as we continue to employ our “risk manager”-focused strategy, which we think is especially important today in a world where investment portfolios look more and more similar due to the increasing prevalence of indexing. While recent market returns have been dominated by stocks with large weights in the common indexes as investors aggressively seek higher risk profiles, you can entrust Intrepid to stay differentiated from its peers and continue to manage risk prudently.

As a real-life example, the Intrepid Capital Fund (“ICMBX” or the “Fund”) has the unusual distinction of making “The New York Times” Mutual Fund List twice: as a 5-year performance leader in 2011 (when managing risk was rewarded well) and a 5-year performance laggard in 2019 (when managing risk was not rewarded). Same guy, same place, doing the same thing: employing an investment strategy that has done well for clients for over 25 years.

This is the hallmark of the Intrepid name and the driver of our past success. With this philosophy in place, we believe the next twenty-five years should be even more rewarding for our clients.

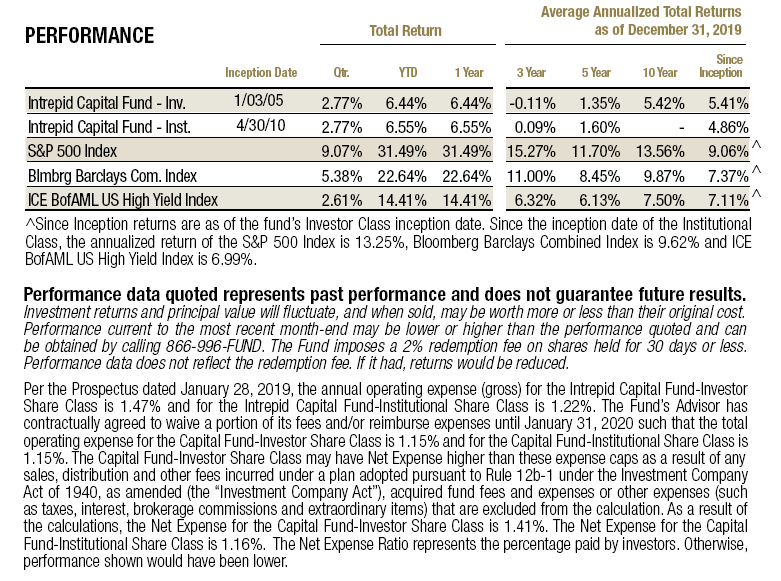

As for the short-term, for the three months ended December 31, 2019, the Intrepid Capital Fund increased 2.77% compared to 5.38% for the benchmark consisting of 60% S&P 500 Index/40% Bloomberg Barclays US Gov/Credit Index. The largest contributors during the period were Jefferies Financial Group (ticker: JEF), Sykes Enterprises (ticker: SYKE), and Skechers USA (ticker: SKX). The three largest detractors were Vistra Energy (ticker: VST), Select Interior Concepts (ticker: SIC), and Dollar Tree (ticker: DLTR).

Happy 25th Birthday, Intrepid Capital! And thank you to our clients and shareholders for their trust in us. If there is anything we can do to serve you better, please don’t hesitate to call.

Best Regards,

Mark F. Travis, President

Intrepid Capital Fund Portfolio Manager