April 4, 2017

“Better to remain silent and be thought a fool than to speak out and remove all doubt.”

-Abraham Lincoln

Dear Friends and Clients,

No, I am not referring to Donald Trump or his incessant tweets. As an aside, I am not certain “tweeting” is appropriate for the President of the United States, especially since they seem to go out unfiltered to the public, which could be a positive or negative depending on your point of view. I was thinking how it would be much more comfortable for those of us at Intrepid Capital to “remain silent” than offer our opinions on the state of the capital markets. I am also reminded of the peril in what I would call “The Boy Who Cried Wolf” syndrome. We have consistently expressed the view that stock prices in relation to the underlying business values are high and likely distorted by the interest rate suppression activity of central banks across the globe. Frankly, I am sure you are tired of hearing this refrain, but it is true, using almost any valuation method one chooses. Always remember the quote from the godfather of value investing, Warren Buffett: “Price is what you pay. Value is what you get.”

My concern for our shareholders, after a long period of both low volatility and higher than normal annualized returns in the U.S. equity markets, is that it becomes expected that one will earn 15% with little risk. If only it were so! Since January 3, 2005, the inception date of the Intrepid Capital Fund (“the Fund”), the annualized rate of return of the S&P 500 is slightly higher than 7%, not twice that rate. The past twelve years encompass two bullish phases of upward equity prices and only one bearish phase, 2007-2009 – posthumously referred to as the Financial Crisis. This bullish phase commenced around this time eight years ago, interrupted only briefly by some volatility in the summer of 2011 around the U.S. debt downgrade. This business of money management is a strange one in that investors, contrary to consumers in virtually any other industry, generally want to buy more stocks, bonds, and commodities after – and only after – prices have risen considerably. Conversely, when stocks are on sale at deeply discounted prices, the majority of investors won’t touch them with a 10-foot pole. This is what I refer to regularly, and sarcastically, as “buying high and selling low!”

Intuitively, in order to create the mispriced opportunities we seek, there must be either a micro event (e.g. company specific – missed earnings, debt downgrade) or macro event (e.g. unexpected change in interest, outbreak of war). Unfortunately, with cheap credit available to all and no obvious global seismic shifts such as sudden currency devaluations, we are left with mostly odds and ends to add to the portfolio. So, we sit here like firemen, waiting to slide down the pole when the bell rings to ferret out investments that meet the stringent qualifications of what we consider absolute value. In the interim, we wait, wait, and wait some more. What will be the catalyst that changes this placid sea into a stormy hurricane? I wish I knew! Believe me, if I did, I would rush to position the portfolio to take advantage of it.

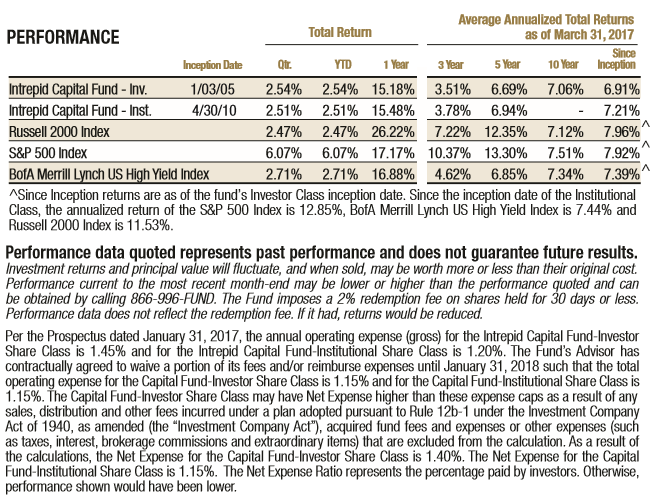

With all of that said, we are pleased with some recently received validation of our investment process. During the quarter, two of our portfolio holdings, Dominion Diamond (ticker: DDC) and Spotless Group (ticker: SPO AU), received buyout offers which helped the stocks reach our internal valuations for each company and led to positive performance for the Fund. For the quarter ending March 31, 2017, the Fund increased 2.54%. For the same period, the S&P 500 Index returned 6.07% and the Bank of America Merrill Lynch US High Yield Index returned 2.71%. Considering the minimal risk incurred due to a healthy 12.1% cash position at the end of the quarter, along with 32.1% in bonds, both investment grade and short duration high yield, and 55.8% in equities, both domestic and international, we are pleased with the performance of the Fund for the period.

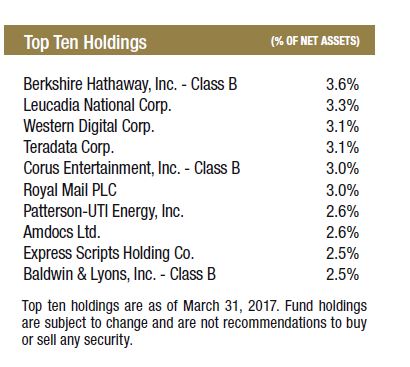

The Fund’s five largest contributors during the quarter were Western Digital (ticker: WDC), Dominion Diamond (ticker: DDC), Oaktree Capital (ticker: OAK), Teradata (ticker: TDC), and Leucadia National (ticker: LUK). The Fund’s five largest detractors for the quarter were Syntel (ticker: SYNT), Dundee Corp. (ticker: DC/A CN), Patterson-UTI Energy (ticker: PTEN), Royal Mail PLC (ticker: RMG), and Verizon (ticker: VZ).

For the first six months of the fiscal year, which began September 30, 2016, the Fund increased 4.94% compared to the returns of the S&P 500 Index and Bank of America Merrill Lynch US High Yield Index of 10.12% and 4.64%, respectively. Contributors to the Fund for the six-month period were Western Digital, Leucadia National, Dominion Diamond, Fenner (ticker: FENR), and Tetra Tech (ticker: TTEK). Detractors to the Fund for the same period were Syntel, Royal Mail, Dundee (ticker: DC.A), Express Scripts (ticker: ESRX), and Primero Mining’s 5.75% convertible bonds due 2/28/2020.

We will be attending the upcoming Morningstar Conference in Chicago on April 26-28. Let us know if you plan to attend. We look forward to seeing you there.

Thank you for your continued support and entrusting us with your hard-earned capital.

Best regards,

Mark F. Travis President

Intrepid Capital Fund Portfolio Manager