April 5, 2017

“If your business is not a brand, it is a commodity.”

-Donald Trump

Dear Fellow Shareholders,

You know that a brand has achieved success when it becomes the default word for the product or service to which it’s attached. We Google to search the Internet, ride a Jet Ski, need a Band-Aid, throw a Frisbee, drink from a Thermos, and relax in a Jacuzzi. Thirteen years ago, a Saturday Night Live skit spawned a neologism for a perennially pessimistic person: Debbie Downer.

Jingle:

“You’re enjoying your day, everything’s going your way

Then, along comes Debbie Downer!

Always there to tell you about a new disease

A car accident or killer bees.

You’ll beg her to spare you, “Debbie, please.”

But you can’t stop Debbie Downer!”

During the past few years, we have received friendly advice that our unenthusiastic view of small cap valuations could cause us to be seen as “perma-bears”…and nobody wants to hang out with a Debbie Downer. The path of least resistance in the investment business is to put on a happy face. We readily admit that we are wired to be more skeptical than your average Joe, but we hope the brand we are building will eventually be regarded as less Chicken Little and more Jiminy Cricket, the level-headed conscience of Pinocchio. We try to tell it like it is, ugly or not.

While small cap stock prices should seem quite beautiful to a seller today, for a buyer eager to deploy capital, they’re downright hideous. The P/E ratio of the Russell 2000 is in the triple digits (113x), and the index’s constituents haven’t collectively grown GAAP earnings over the past 20 years. U.S. economic growth has been declining and leverage in the system has been rising, yet the EV/EBITDA of the benchmark is nearly 50% above the peak multiple reached before the credit crisis.

While I was writing this letter, a colleague forwarded to me just-released market commentary from a prominent small cap mutual fund company. That manager believes the small cap cycle has more room to run. They base this on the market’s resilience over the past year, in light of developments such as Brexit and the U.S. election. They support their argument by saying that this cycle is young, identifying the February 2016 pullback as the trough. They also noted that since the inception of the Russell 2000 in 1979, the index has declined by 15% or more 12 times. According to their analysis, the median return during the subsequent rebound was 99%. Since the Russell 2000 is only up 48% from their February 11, 2016 trough, they think we are less than halfway through a recovery. While we don’t know whether the market will continue to grind higher in the short-term, we couldn’t disagree more with their logic.

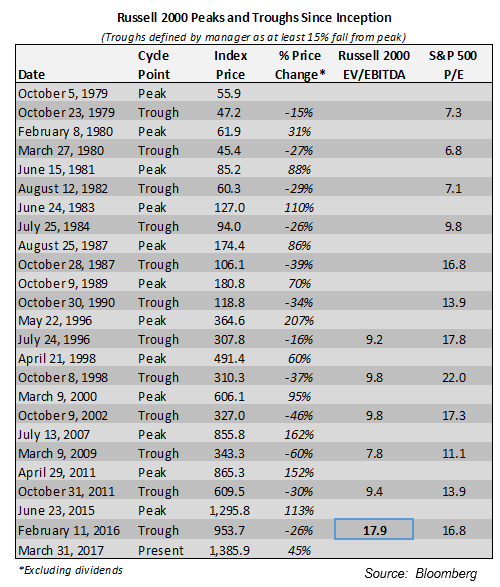

We believe it is highly misleading to claim that this cycle is “young.” We’re currently in the second longest bull market in history, as this one began in March 2009. While the Russell 2000 did experience a 26% peak-to-trough pullback from June 2015 to February 2016, in our opinion, this hardly qualifies as a bear market given its brevity and the extremes of the peak. The aforementioned small cap fund company thinks we’re halfway through the rebound based on a mechanical calculation of the median return from previous corrections exceeding 15%. The problem with this argument is that the small cap market was far cheaper at historical troughs than it was in February 2016.

Our firm only has access to Russell 2000 earnings data going back to 1995. Per share earnings for the small cap index are extremely volatile and sometimes negative, so we examined the historical EV/EBITDA multiple of the Russell at the last five troughs prior to 2016. The average multiple was 9.2x. The multiple in February 2016 was 17.9x. For the periods prior to 1995 where we don’t have Russell data, we do have access to S&P 500 earnings. The P/E of the S&P 500 in these earlier years was much lower, on average, than it was in the late 90’s and 2000’s. While large and small caps don’t always behave similarly (e.g. during the tech bubble), we are confident that the 17.9x EV/EBITDA seen in February 2016 was above any previous trough valuation for the Russell index. Therefore, we think it’s extremely imprudent to project past returns from Russell 2000 troughs onto today’s market without acknowledging the materially different starting point for valuations. Simply put, small caps have never been this expensive.

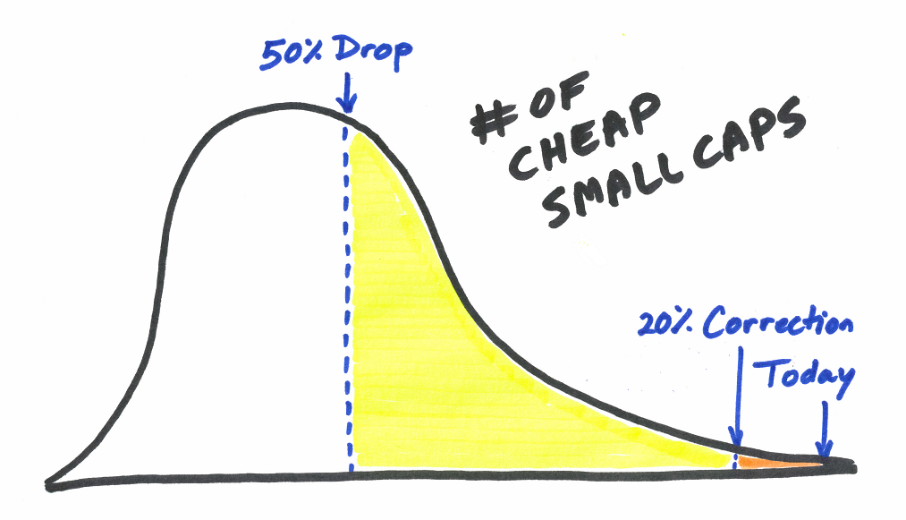

We are often asked what it will take for us to put more money to work. One good new idea would get us excited. We found two of them in Q4 but none this quarter. We would probably need more than a dozen opportunities for the Intrepid Endurance Fund (the “Fund”) to reach a more fully invested status. While that could happen even amid the broadest small cap bubble of all time, our gut tells us the market will need to fall significantly before the Endurance Fund is fully invested again. To help visualize how we judge today’s opportunity set, for illustrative purposes only, consider a positively skewed distribution.[2] We are currently on the far end of the right tail. With a correction of 10% or 20% to small cap prices, we would still remain close to valuation extremes. A 50% plummet would just take us back to levels reached in 2011. While we expect that we would be aggressively deploying capital under that scenario, the market would not be reflecting the fire sale valuations we saw in 2009.

Source: Intrepid Capital

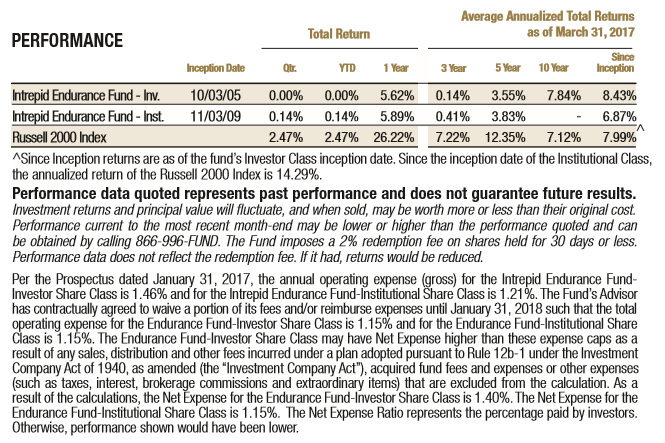

The Endurance Fund was exactly flat for the calendar first quarter ending March 31, 2017, while the Russell 2000 increased 2.47%. The median stock in the Russell 2000 was up 0.12% in the quarter, so almost all of the index’s performance was derived from larger capitalization constituents. For most of the quarter, the Fund’s return was in negative territory, as a few of our top holdings experienced large markdowns. However, performance improved near the end of the quarter due to a proposed takeover for one of the Fund’s main positions and increases in the value of other holdings.

This begs the question: how can we have so much cash and still have been losing money until the very end of Q1? It’s not easy! We often invest in complicated situations and unloved businesses, but usually not in unloved business models. Currently, we own very few securities that belong to the Russell 2000 benchmark, and that’s not a coincidence. Russell stocks are expensive, no doubt pumped up by indiscriminate ETF buying. The Fund’s holdings are as uncorrelated to the market as they have ever been, which has been achieved by owning foreign securities, convertible bonds, precious metals, and other investments that fall outside of the U.S. small cap benchmark.

While the Fund’s performance over the past two quarters has not been impressive, we believe there are two points worth considering. First, price does not equal value. In general, we think that some our key holdings became even better bargains in recent months. Many of our top losers from 2015, a difficult year, were top gainers for us in 2016. Second, it’s not unusual for the Fund’s performance to deviate significantly from the small cap index. Last year, all of the Fund’s return came in the first 8 months of the year, and we didn’t rally at all post-election. The small cap market exhibited the opposite behavior.

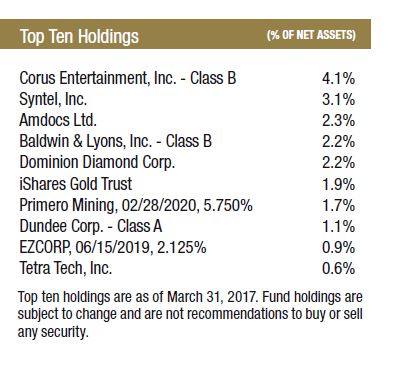

The largest contributors to the Fund in the first quarter were Dominion Diamond (ticker: DDC), Corus Entertainment (ticker: CJR/B CN), and the iShares Gold Trust (ticker: IAU). On March 16th, Dominion announced strong guidance for its 2018 fiscal year, which ends on January 31, 2018. This led to a 12% spike in the stock, which had been selling off over concerns that India’s demonetization could have longer-lasting impacts on rough diamond prices than previously thought. That weekend, The Washington Companies disclosed that it made a U.S. $13.50 per share takeover offer to Dominion’s board in February, which was a 54% premium to where the stock traded before the company issued guidance. We were not completely surprised by the offer, since Dominion’s balance sheet has a large amount of cash and because the stock had been trading near multiyear lows. Washington consists of a group of privately held businesses in the U.S. and Canada, including one of the largest copper and molybdenum mines in North America. Billionaire Dennis Washington owns the firm, and the bid for Dominion was rumored to be pushed by David Batchelder, the activist who co-founded Relational Investors and who sits on Washington’s board. Dominion and Washington have not been able to agree on terms that would allow Washington to complete its due diligence. Both parties have publicized their dispute.

On March 27th, Dominion said it would explore strategic alternatives that could include a sale of the company. The firm engaged in a similar process beginning in 2015, but the effort seemed to fizzle after Dominion entered into a settlement with an activist group. We believe the odds are higher of a deal being completed this time due to Washington’s expressed interest and because the composition of the board has changed. The rough diamond market is also in better shape today. Dominion’s shares are now fully valued using our base case assumptions, so we partially reduced the position. However, the stock continues to trade below Washington’s conditional offer. We think Dominion could be more valuable in the arms of a strategic suitor, so we have maintained exposure to the name.

Corus Entertainment’s stock appreciated modestly in the first quarter. We believe the company’s television advertising revenue is only one quarter away from showing year-over-year growth, which would end a painful chapter in Corus’s history. If Corus’s earnings start to improve, we think investors should be willing to assign a higher multiple to the company’s free cash flow stream. Corus’s shares currently offer a dividend yield of 8.7%. We expect management to apply cash flow to debt reduction.

iShares Gold Trust benefited from the 8.9% increase in the price of gold over the first three months of the calendar year. We don’t envision this as a permanent holding for the Fund and would rather own actual businesses, like precious metal streamers. Nevertheless, if streaming companies or miners trade at higher valuations than can be justified by current metals prices, we will sell them, just like any other stock.

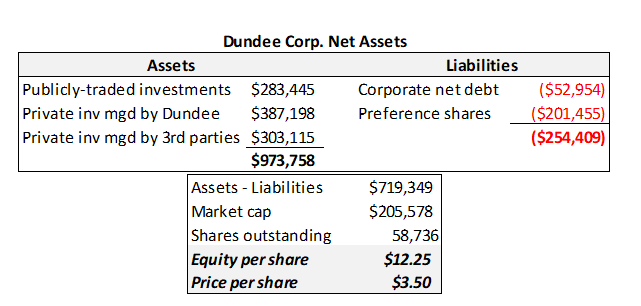

The top detractors from Q1 performance were Dundee Corp. (ticker: DC/A CN), Syntel (ticker: SYNT), and Primero Mining’s 5.75% Convertible Notes (CUSIP: 74164WAB2). Dundee’s performance has been abysmal, and that comment doesn’t just apply to the stock. The company is involved in many different ventures, but almost nothing has worked out. We attribute at least half of the unfavorable outcomes to poor decisions by management and the rest to bad luck. Hindsight is 20/20, and our involvement in Dundee came from trying too hard to find value in an over-picked market. Our fair value for the stock is based on asset value, in contrast to our typical discounted free cash flow valuation. We felt comfortable with this approach because the assets were originally anchored by publicly-traded equities that seemed reasonably valued to us on inspection. Dundee’s cash flow has been negative as the team attempted to nurture a basket of various nascent businesses into self-sustaining enterprises. It hasn’t worked. We had chances to revisit the investment as the situation changed and decent investments were exchanged for speculative ones. The mistake is on me, your Portfolio Manager. We have not added to the holding in over a year and reduced our position last summer at better prices—a small victory in an otherwise dreadful investment.

So where do we go from here? Dundee is a $3.50 stock with $12.25 of book value. That book value continues to decline as the company’s portfolio is not generating cash flow but Dundee is incurring corporate overhead and financing costs. Right now the market is implying that every single private company Dundee manages is worth nothing, plus that the business burns cash at the current rate for another three years. We have urged management to sell Dundee’s public investments to pay off bank debt and preferred stock, which would reduce cash burn by half. If the company then catches a break on one of its major private investments, it could mark a turning point for the company’s fortunes. We’re not holding our breath but aren’t yet inclined to sell Dundee at today’s prices. The Fund’s weight in Dundee is approximately 1%, so its impact on performance going forward should be more limited.

Our investment in Syntel started off well, increasing over 15% in just a few months…then the company announced guidance in February. The stock gave it all back and then some, so now we’re about 15% in the red. While fourth quarter results were in line with projections, the company’s outlook for 2017 was well below consensus estimates. Management painted a subdued spending picture for the industries Syntel serves. The stock’s underperformance is primarily tied to Syntel’s revenue declines versus growth for the rest of the IT services industry. The company coasted for years on sales growth from its largest customers—American Express, State Street, and FedEx. Those customers are now reducing spending, and Syntel’s smaller clients are not picking up the slack. This has prompted management to increase the heretofore lean marketing budget.

Some investors are also concerned about Syntel’s chops in the digital arena, but the company’s well-regarded SyntBots automation platform demonstrates that Syntel can develop cutting edge IP. Lastly, legal immigration policy remains an overhang, as there are several bills in Congress that seek to change the H-1B visa program, and the Trump administration has already made a couple of marginal changes that could negatively impact outsourcers. We take some comfort that both Chuck Schumer (D-NY) and Paul Ryan (R-WI) have previously expressed support for the H-1B program, suggesting that it may be difficult to push a bill through Congress that severely curtails visa issuances. Even if we are wrong, Syntel has several ways to deal with fewer visas, including sending more work offshore, increasing local hiring of Americans, expanding automation to reduce labor, and also passing along cost increases to customers. Syntel trades for about 9x expected free cash flow. It is now the second largest position in the Fund and one of the biggest discounts to our estimated fair value.

Primero Mining experienced an eventful quarter, which included a mine strike, reserve reduction, CEO resignation, and going concern language. Did we mention we like this security? The bonds certainly carry risk, but they yield 25%. We believe the strike at the San Dimas Mine in Mexico will end shortly, since the miners have few other options for employment. Additionally, Silver Wheaton has indicated that it is willing to modify its silver stream with Primero if it is fairly compensated. Silver Wheaton also recently guaranteed Primero’s credit facility, enabling a six month extension that gives Primero time to explore strategic alternatives. In other words, Silver Wheaton is as attached as ever to Primero. We view this relationship as the main lever to improve the company’s health.

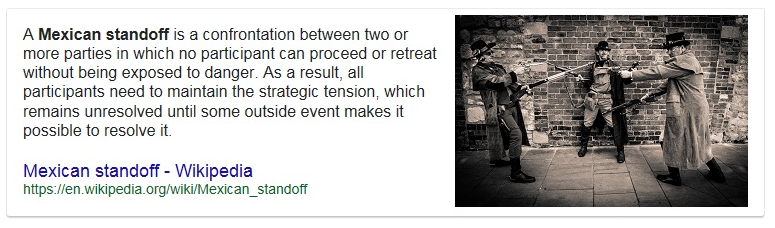

With that said, Primero, Silver Wheaton, and the Tax Administration Service (SAT) are embroiled in a Mexican standoff at the moment (pun intended). Primero can survive if either the SAT relinquishes its pursuit of Primero for higher taxes on its silver production or if Silver Wheaton reduces the burden of its silver stream on San Dimas. However, if either the SAT or Silver Wheaton acts, the other party may not have to yield anything. We think Silver Wheaton will cave first, since its Herculean efforts to avoid paying taxes in Mexico and almost everywhere else make it unlikely that it would want to see this situation through a restructuring. Silver Wheaton as a mine owner in Mexico would be a much juicier target than Primero.

Our promise to you is straightforward: we have a process and we’re sticking to it, come hell or high water. The linchpin of our process is to not own stocks that we think are overvalued, which covers just about everything today. If we cannot find an undervalued security, we hold cash or equivalents. As a result, cash and Treasury bills account for 79.4% of the Endurance Fund—an all-time high. Some shareholders have departed because they don’t want to pay us a fee on cash, even though they respect our stock selection. We understand. In spite of the temporary consequences to fund flows for holding “too much cash,” we wouldn’t feel comfortable justifying our management fee by intentionally owning overvalued stocks.

Investing is a tough, competitive business. The hardest aspect is managing your emotions. When do you get into the market? When do you get out? Most investors struggle with these questions. This Fund is designed to take that burden from you. If the stock market is bubbly, our positioning is sober. If it’s a bloodbath, we’re Bram Stoker. We’re not any smarter than the next guy and we make plenty of mistakes, but our process is our guidepost. The one thing that we’re certain we do well is follow our investment process. As shareholders in the Fund, that helps us sleep well at night. Thank you for your investment.

Sincerely,

Jayme Wiggins, CFA

Chief Investment Officer

Intrepid Endurance Fund Portfolio Manager

[1] http://www.nbc.com/saturday-night-live/video/debbie-downer/n11825?snl=1

[2] We chose a positively skewed distribution because we believe periods of overvaluation are more extreme and frequent than the periods of undervaluation.