January 4, 2026

Dear Fellow Shareholders,

The fourth quarter of 2025 proved to be a fitting conclusion to what was a strong year for credit markets. Despite intermittent bouts of volatility, risk assets finished the year on solid footing. Major equity indices continued to grind higher and closed the year near all-time highs. Credit markets also fared well. Rates ended the year relatively flat, leading to modest positive returns for investment grade bonds in the fourth quarter. High yield credit performed slightly better, with the broadly followed indices delivering returns of approximately 130-140 basis points.

High yield credit spreads saw some moderate widening at various points in the quarter, as investors reacted to risks of further trade flare ups and a less dovish Fed. High yield spreads ended the quarter about 20 basis points wide of the multi-year lows from earlier in the year, but remain tight by historical standards at around 300 basis points at year-end.

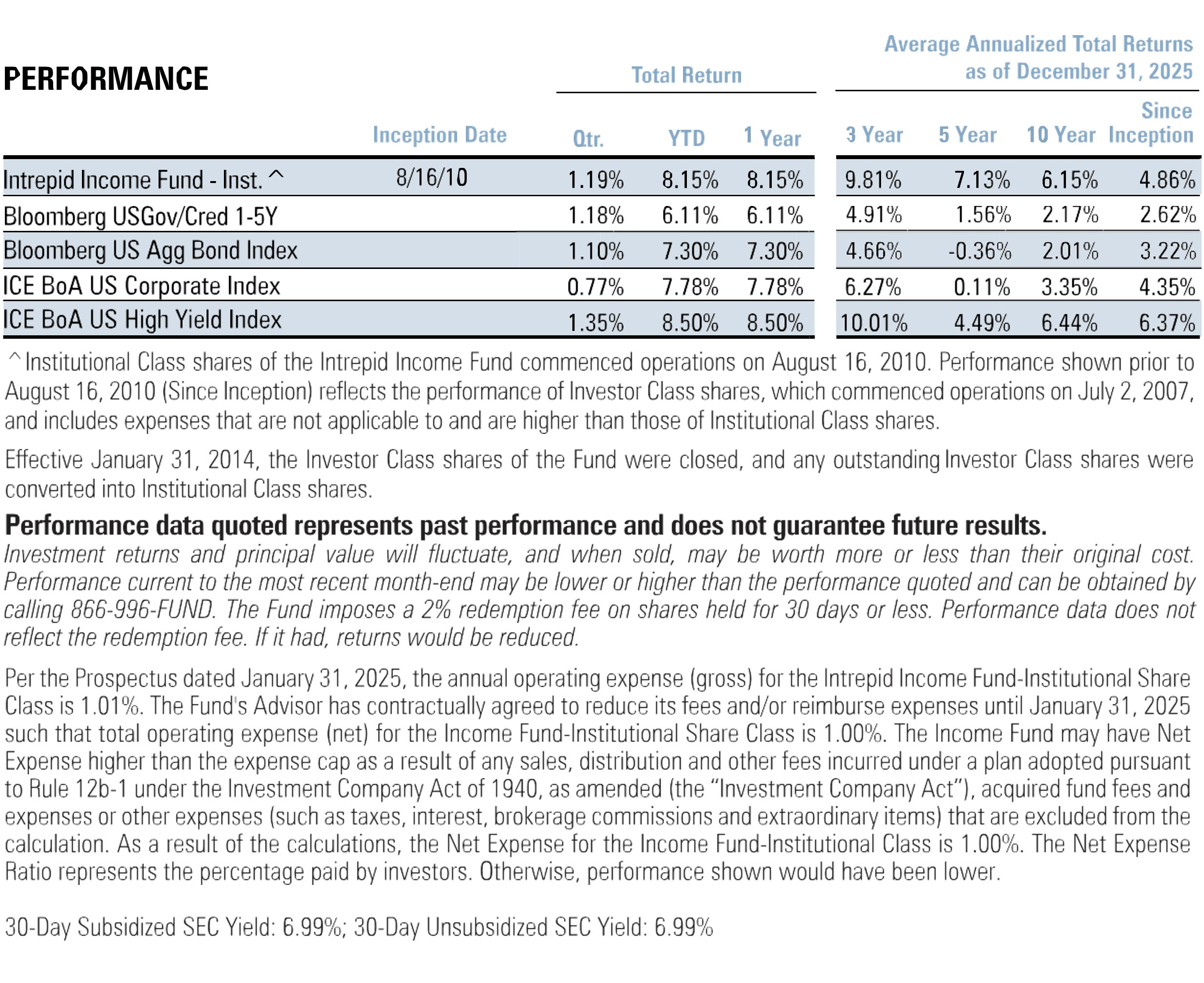

The Intrepid Income Fund (the “Fund”) delivered a return of 1.19% for the quarter ended December 31, 2025, compared to a return of 1.18% for its benchmark Bloomberg US Gov/Credit 1-5 Year Index. For the full year, the Fund returned 8.15% compared to 6.11% for its benchmark. We are particularly pleased with the Fund’s recent performance relative to high yield indices. For the three years ended December 31, 2025, the Fund’s 9.8% annualized return was just a notch below the 10.0% of the widely followed ICE BofA High Yield Index. While downside protection is our goal, participating in bull markets is another important feature. Our recent upside capture has exceeded our expectations, which we attribute mainly to good idiosyncratic performance in certain credits rather than a more risk-on tactical positioning. We continue to fund value in smaller issue, off-the-run credits that we believe offer comparable return to High Yield indices, but with less risk.

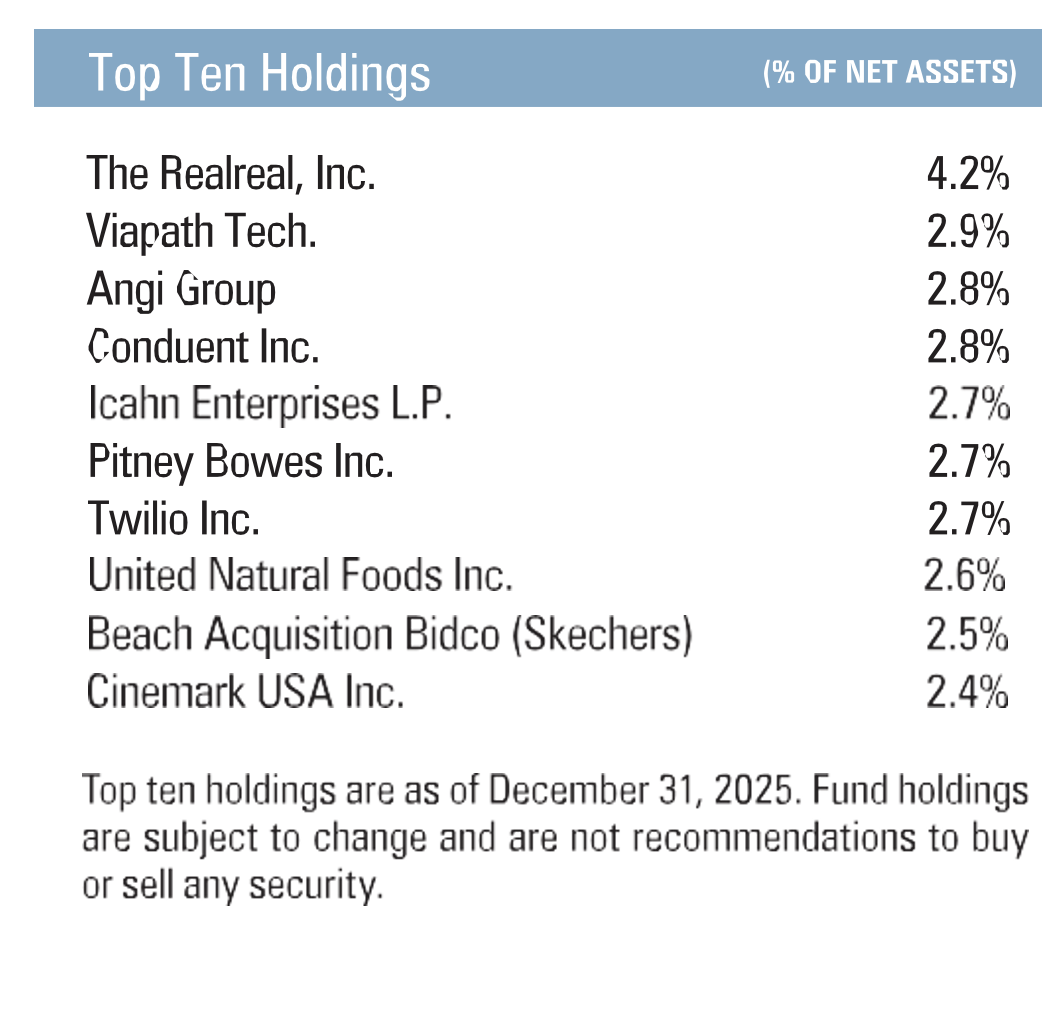

The portfolio continues to be anchored by credits with strong balance sheets, identifiable asset coverage, and durable free cash flow. Among the more notable contributors to performance during the quarter were a handful of positions in the consumer and communications sectors that benefited from strong operating results and spread compression specific to those issuers. The top contributors meaningfully outpaced the drag from our top detractors.

We ended the quarter with a yield-to-worst of approximately 8.0%, which is relatively consistent with prior quarters and reflects a similar spread with some movement in rates. The Fund’s effective duration was 1.8 years atquarter-end, which is about 0.3 years below prior quarter and the first quarter below 2 years since 2023. This shortening was mainly due to a larger number of credits trading at levels that would imply being called early, thus reducing their effective duration. Other duration metrics, such as average maturity, remain relatively unchanged from the prior quarter. We continue to hold a mix of core positions with maturities ranging from 2-5 years as well as positions with an imminent maturity or call date.

Entering 2026, we find ourselves in a familiar position: cautiously optimistic about the opportunity set, but mindful that valuations in credit are not cheap by historical standards. As we have noted in prior commentaries, we believe the credit quality of the high yield index is healthier than in prior cycles. Ratings mix skews higher, the portion of secured debt is higher, and many companies have exploited the favorable credit environment of the last several years to extend maturities. Furthermore, we think the rapid growth in private credit picked off a number of would-be public credits at the riskier end of the spectrum.

On the other hand, spreads remain tight relative to long-run averages, and a number of macroeconomic crosscurrents — including residual tariff impacts, a gradually softening labor market, and an uncertain path for monetary policy — warrant continued vigilance. We recognize that the credit conditions of the last three years have been mostly benign by historical standards and are prepared for more volatility in 2026.

For now, we remain focused on what we can control: identifying creditworthy issuers in our core niche of small issue, less-followed fixed income securities, and maintaining the shorter duration profile that has served the Fund well across a variety of environments. We believe the portfolio is well-positioned to deliver attractive absolute returns withless rate sensitivity, while providing meaningful downside protection should credit conditions deteriorate.

As always, we welcome outreach and would welcome the opportunity to discuss the portfolio with you in more detail. Thank you for your trust and investment.

Sincerely,

Hunter Hayes, CFA, Chief Investment Officer

Intrepid Income Fund Co-Portfolio Manager

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Matt Parker, CFA, CPA

Intrepid Endurance Fund Co-Portfolio Manager

Joe Van Cavage, CFA

Intrepid Endurance Fund Co-Portfolio Manager