January 4, 2026

Dear Fellow Shareholders,

Our Fund’s positive performance was interrupted when bombs started dropping in Iran the last week of February, though we managed to hang on to positive results over the trailing six months. I am pleased to report a positive

+1.16% return over that period, but volatility certainly spiked in March as the market had to digest significantly higher oil prices, along with the guessing game of “would he, or won’t he.” The “he” in this case was Donald Trump and his demands of the theocratic regime in Tehran.

+1.16% return over that period, but volatility certainly spiked in March as the market had to digest significantly higher oil prices, along with the guessing game of “would he, or won’t he.” The “he” in this case was Donald Trump and his demands of the theocratic regime in Tehran.

A relentless air war that began with the death of the Supreme Leader and much of his cabinet ended in March with Iranblocking the Strait of Hormuz and choking off 20% of the world’s oil supply, sending the price of oil skyward

and stocks falling. In addition, the “risk free” 10-year US Treasury rate repriced higher roughly 30 basis points to ~4.30%. Gold, often a refuge in falling stock and bond markets, also moved lower in response to all of the above.

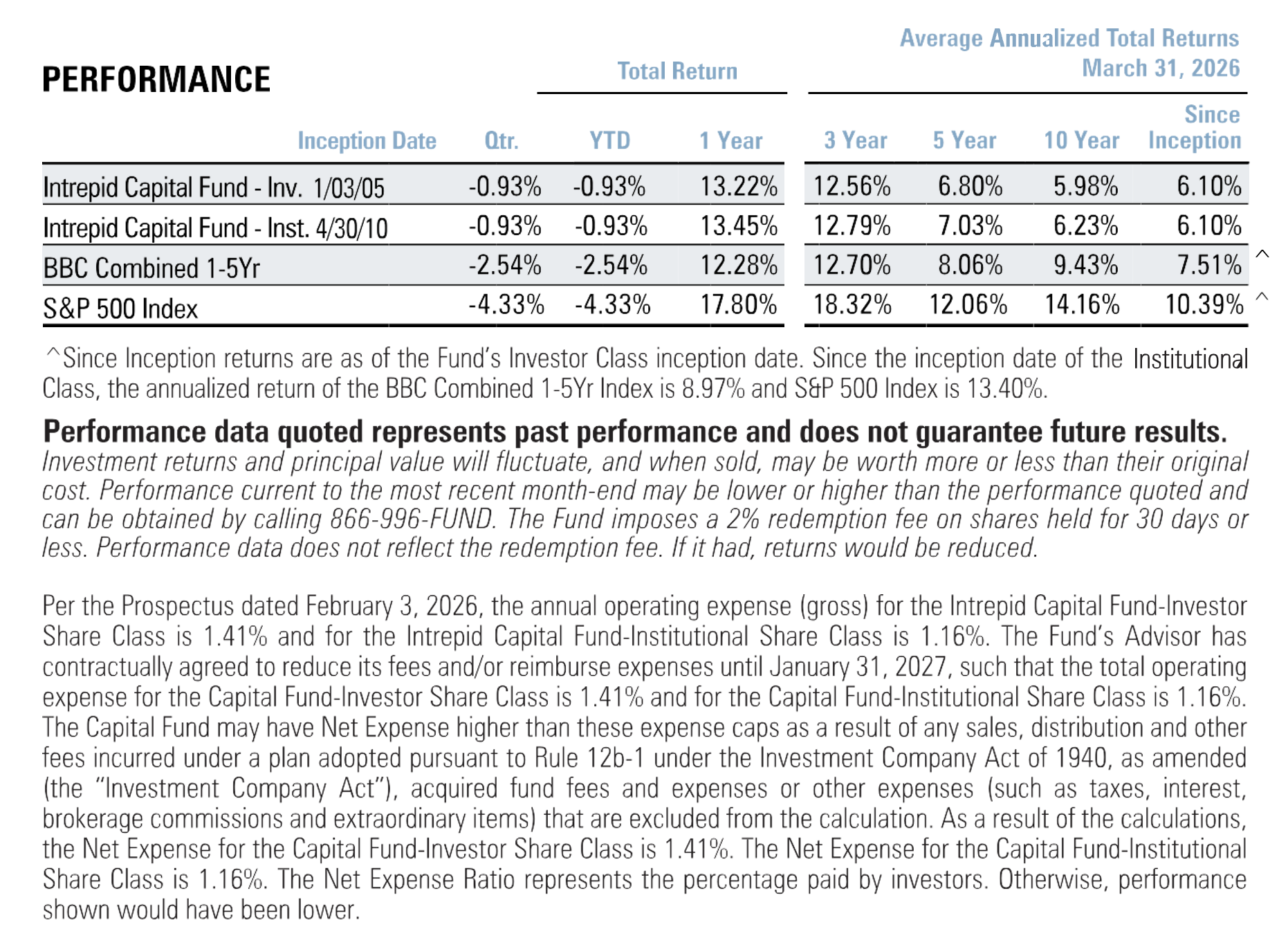

We are now in somewhat of a stalemate in that the regime doesn’t want “change” and the Iranian Revolutionary Guard doesn’t either. Subsequently, theyhave successfully blocked the Strait and President Trump has called for a two-week truce – brokered by Pakistan. We shall see. Despite all of the excitementlisted above the fund ended just modestly down for the first calendar quarter of2026 (-0.93%) which was relatively favorable to the US equity indices for thesame time period. This performance includes a dividend of $0.11932 per sharepaid on March 31, 2026.

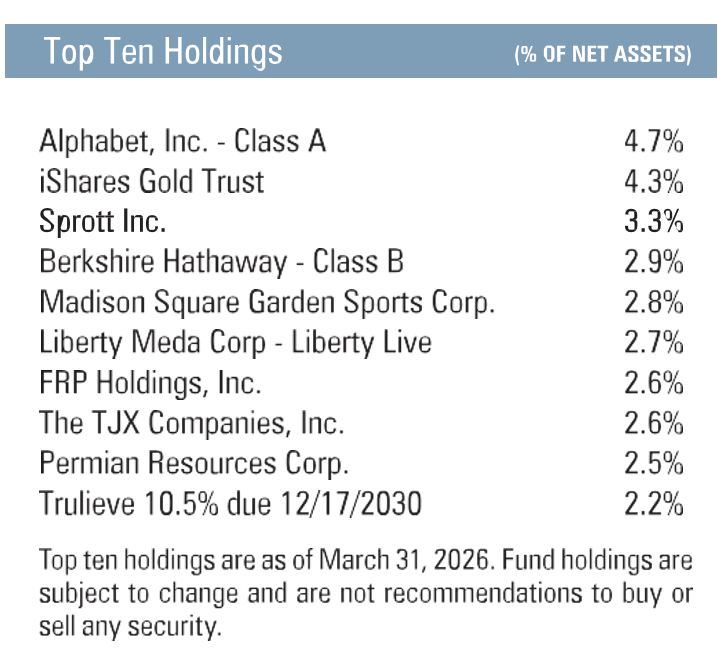

Top contributors for the semi-annual period ending March 31, 2026:

| Sprott Inc (SII): | +1.38% |

| Permian Resources (PR): | +1.04% |

| Fabrinet (FN): | +1.04% |

| Madison Square Garden Sports (MSGS): | +0.82% |

| Alphabet (GOOGL): | +0.80% |

Top detractors for the semi-annual period ending March 31, 2026:

| Fiserv (FISV): | -1.11% |

| Jefferies (JEF): | -0.60% |

| Take Two Interactive Software (TTWO: | -0.57% |

| Conduent 6% Notes due 11-1-2029 | -0.56% |

| Copart (CPRT): | -0.39% |

Thank you for your continued support. If there is anything we can do to serve you better, please don’t hesitate to call.

All the best,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager