April 11, 2026

In last quarter’s commentary, we wrote that “…the credit conditions of the last three years have been mostly benign by historical standards and we are prepared for more volatility in 2026.”

That was meant to be a description of the Fund’s positioning…not a prediction. But for better or worse, volatility increased meaningfully during Q1 2026 due to three major negative external developments:

- growing concerns about the health of the private credit industry

- the sudden emergence of the Iran war, and

- panic about the impact artificial intelligence (AI) will have to existing business models within the technology sector, particularly in software (the “SAAS-pocalypse”).

These three events caused increased volatility in both the stock and bond markets during Q1. With that said, much like during the “Liberation Day” tariff-driven volatility a year ago, the high yield credit market proved remarkably resilient relative to other risk assets such as large cap (as represented by the S&P 500 Index) and small cap (as represented by the Russell 2000 Index) stocks.

Specifically, the high yield market was down only slightly during Q1 despite the volatility referenced above. As measured by the Bloomberg US Corporate High Yield Bond Index, the asset class returned -0.50% in the quarter and at its trough in March was down -1.29% year-to-date. By comparison, the S&P 500 and Russell 2000 indices were down -7.05% and -2.48% YTD at their March troughs, respectively.

We have discussed in these publications for some time how the high yield market has gradually evolved into a higher quality asset class than its past reputation implies. We based this on the status of its internal characteristics compared to its history — today it consists of higher average credit ratings, a higher mix of secured debt versus unsecured, and lower duration.

We have discussed in these publications for some time how the high yield market has gradually evolved into a higher quality asset class than its past reputation implies. We based this on the status of its internal characteristics compared to its history — today it consists of higher average credit ratings, a higher mix of secured debt versus unsecured, and lower duration.

So it was nice to see the high yield market generate dramatically less volatility than stocks as investor sentiment deteriorated throughout Q1. We like the track record the asset class is establishing and have seen more investors take notice and increase their comfort allocating to it.

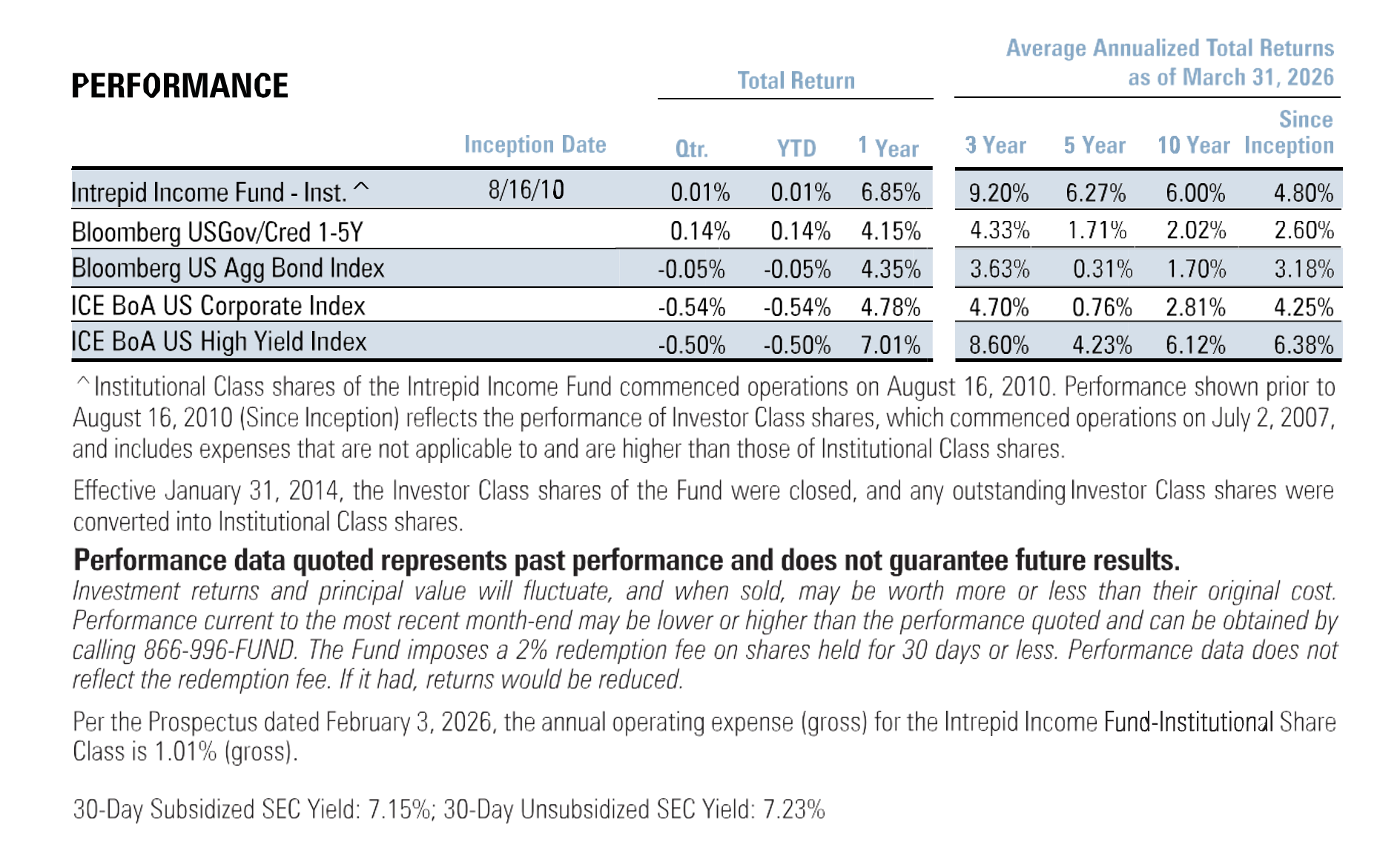

We are happy to report the Intrepid Income Fund (“the Fund”) eked out a slightly positive gain during the quarter of +0.01%. This result outperformed the high yield benchmark above, and was in between the Bloomberg US Aggregate Index (-0.05%) and the Fund’s benchmark Bloomberg US Government/Credit 1-5 Year Index (+0.14%).

We have stated in the past, and continue to believe, that staying out of the business of macroeconomic predictions and focusing on the task of analyzing our core niche of small, off-the-run fixed income securities is in the Fund’s best interest.

However, when major external events occur that could impact the Fund’s holdings, we take it seriously and immediately re-underwrite our positions for a potential new reality. We did it in early April 2025 when “Liberation Day” created the risk of a monumental shift in global trade, and we did it again in Q1 2026 in response to the potential impact of the private credit industry’s troubles, the Iran War, and the SAAS-pocalypse.

Below is a brief summary of each.

Private Credit’s Health

Without re-hashing what’s been well-covered in the financial press, the private credit industry has been hit by a combination of credit losses (driven by past loose underwriting and some high-profile fraud cases) and a resulting loss of investor confidence that has driven redemption requests. Due to the inherent lack of liquidity in this asset class, many of these requests have been “gated” in numerous vehicles.

This is something we follow closely, as shifts in sentiment in one asset class always runs the risk of becoming a contagion in adjacent ones. However, we note again that the public high yield bond market showed remarkable resilience — despite a period of outflows during the quarter in the asset class that was likely driven by investors’ lack of ability to access liquidity in their private credit allocations.

As the private credit industry has grown over the past decade, there are a number of troubled, higher-risk issuers that have been “taken out” (meaning refinanced) by the private credit market. Relying on other investors to refinance our holdings has never been consistent with our underwriting philosophy, but now that the private credit “rescue” option may be off the table going forward — we need to remain extremely vigilant to ensure we never find ourselves in that position.

We have also paid close attention to any private credit investor involvement in the liquid securities in our investment universe. Liquid holdings will likely be the first thing a private credit fund would sell to satisfy redemptions. While this could provide incredible entry opportunities, we need to keep our head on a swivel.

On a positive note, it would not surprise us to see assets reallocated from private credit investments to the public markets. The liquidity and integrity of valuation marks in public markets remedies two chief concerns of private credit uneasiness. For those investors who wish to maintain fixed income exposure, a rotation into high yield and levered loan asset classes seems logical. Time will tell.

Iran War

Despite the Fund’s solid relative performance this quarter — it was not a meaningful beneficiary of the war. Specifically, the Fund has very few positions in the energy sector and remains underweight compared to broad high yield indices. If anything, the increase in energy prices was a net negative for the Fund in terms of expected higher operating costs (materials, shipping) and reduced consumer sentiment in the future for the underlying companies.

With that said, after re-underwriting the Fund’s holdings for much higher energy prices, a potential slowdown in the global economy, and a potential re-igniting of inflationary pressure, we believe that our initial conservative underwriting appropriately accounted for scenarios such as this. As a result, we did not determine the need to sell or reduce any positions in response to the war’s anticipated macroeconomic impact. Instead, given our increased confidence in their ability to endure, we added to certain positions as opportunities arose.

SAAS-pocalypse

SAAS is an acronym for software-as-a-service and this former darling sector of the investment community experienced extreme pressure during Q1 as the frontier AI labs dropped new and better processing models weekly. The leap forward that occurred in AI’s collective capabilities during the quarter drove what was legitimate investor panic – not only in the software industry, but also in others such as business services that investors fear are the most exposed to AI disruption.

This risk was the most serious and most difficult re-underwriting we did during the quarter. Frankly, it’s a hard risk to assess. It’s difficult to argue that AI’s capabilities aren’t over-hyped today. However, it’s also difficult to argue they haven’t progressed dramatically over the last two years and likely will continue to.

What does this mean for software and business service credits? Like always, it means remaining extremely circumspect and vigilant in our re-underwriting. It means modeling increased disruption to business models, future earnings power, and credit metrics. And it means requiring these holdings to be able to deal with their future debt maturities through their own cash flow generation, as the incredible flight to capital to any perceived AI beneficiary increases the risk that any perceived AI loser could lose all access to the credit market in the future.

As a result of this process, and similar to actions we took in response to our re-underwriting exercise following the “Liberation Day” tariffs, we quickly jettisoned the positions that failed the criteria in the paragraph above.

Closing

The “SAAS-pocalypse” was the most impactful external development to the Fund this past quarter. As indicated above, we will remain focused on our niche opportunity set and continue to forgo incorporating macroeconomic predictions in our portfolio construction, while also being responsive and vigilant to potential risks as they emerge.

The Fund ended the quarter with an 8.4% yield to worst, an effective duration of 1.8 years, and has undergone a very recent and very rigorous re-underwriting process. As a result, we believe it is well-positioned to accomplishour objective of earning equity-like returns with lower volatility while maintaining a senior position in the capital structure.

As we have mentioned over the past several quarters, we have gradually decreased credit risk and increased liquidity in the Fund. We believe that served the Fund well during Q1. And while we don’t have any time for macroeconomic predictions, we continue to position the Fund consistent with last quarter’s statement: “…the credit conditions of the last three years have been mostly benign by historical standards and we are prepared for more volatility in 2026.”

If Q1 was a preview of the rest of the year, then attractive opportunities should follow and we believe the Fund is well-positioned to capitalize on them. However, if sentiment recovers and the issues the market is concerned about resolve themselves, we believe Fund’s 8.4% yield-to-worst and lower interest rate risk will deliver an attractive risk/return profile. Of note, US Treasury rates increased during Q1 on re-inflationary concerns despite the market’s expectations ofrate cuts entering the year. Will this be the next external development that causes market volatility?

Your guess is as good as ours. But despite the Fund’s very short duration of 1.8 years, we will continue to re-underwrite our holdings for any negative implications that could emerge from this potential risk.

Thank you for your trust and investment. If there is anything we can do to serve you better, please do not hesitate to reach out.

Hunter Hayes, CFA, Chief Investment Officer

Intrepid Income Fund Co-Portfolio Manager

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Matt Parker, CFA, CPA

Intrepid Endurance Fund Co-Portfolio Manager

Joe Van Cavage, CFA

Intrepid Endurance Fund Co-Portfolio Manager