January 7, 2023

Ted Striker : Surely you can’t be serious

Rumack: I am serious… and don’t call me Shirley.

– Airplane!

Dear Fellow Shareholders

Do you remember the movie Airplane!? The 1980 slapstick classic is consistently listed as one of the greatest comedic films ever released. It stars Robert Hays (Ted Striker) as an ex-fighter pilot who boards a commercial flight from LA to Chicago in the hopes to win back his flight attendant girlfriend. After the plane’s crew falls ill from bad fish, Striker is forced to work with an air-traffic controller and his former commanding officer to try to bring the plane down safely. In one of the more memorable scenes, passenger Dr. Rumack (played by Leslie Nielsen) breaks the news to Striker that he is their best hope to land the plane despite a fear of flying and no commercial piloting experience. Nielsen delivers one of his most famous lines in the process.

We can’t help but think the Fed faces a similarly daunting challenge today. After an epic boom (mania?) in financial markets in the wake of covid and ensuing inflation that reached 40-year highs, they now face the dilemma of restoring price levels to their 2% inflation target while trying to minimize collateral damage to the real economy. Taking away the proverbial punch bowl while avoiding the ensuing economic hangover has historically been a tall order.

Inflation and interest rates remain front and center in investors’ focus. Bulls argue that inflation has peaked, the Fed can soon pivot back to a more dovish stance, rates are likely to return to lower levels, and the price of risk assets can climb higher again. There are certainly reasons that support this position. Inflation indeed appears to have peaked, and the gradual recovery of supply chains suggests that it’s unlikely we will

return to the 8-9% levels from this summer. On a month-over- month basis, headline and core (ex-food & energy)

CPI equate to an annualized pace under 2.5% – nearly in line with the Fed’s 2% objective. If this pace continues, it could seemingly provide the cover for the Fed to abandon its hiking cycle and cave to market and political pressure to prevent more economic pain. Furthermore, consumer spending – while slowing – has remained resilient, and employment is strong. A timely return to easier monetary policy might stave off any future weakness. This scenario is what many market observers are calling the “soft landing.”

On the other hand, the Fed has proven more hawkish than many expected, and there are a number of bearish investors who believe more rate hikes are needed to thoroughly quell the inflationary psychology permeating the economy. They argue that consumer spending is unsustainable as Americans have been forced to tap into pandemic savings to keep up with inflation (personal savings rates near 20-year lows), and that the full impacts of rate hikes have yet to trickle into the real economy. Layering a more cautious consumer on top of an already slowing economy would be a prescription for deteriorating business conditions. This bearish case assumes a recession, which has often been the outcome of historical tightening cycles. This is the “hard landing” alternative scenario.

Which outcome do we believe is more likely? In short, we have no idea. Given the sizable declines in equity markets in 2022 (the S&P 500, Russell 2000 and Nasdaq were down 18%, 20% and 33%, respectively), it’s clear to us that

(1) investors have already priced in a reasonable likelihood of a recession, and (2) long-term prospective returns in stocks are higher today than they were a year ago, despite what feels like a riskier environment. Outside of this, we don’t find it useful to focus on these macro-outcomes that we can’t predict any better than other market participants.

As we have frequently written, we find it far more productive to concentrate on individual small cap businesses, which we understand well. Price volatility in the small caps that we cover was generally lower in Q4 than the prior three quarters of 2022. As a result, trading in the Intrepid Small Cap Fund (“the Fund”) was also less active than prior quarters (there were no new positions owned at 12/31/22 that were not owned at 9/30/22). The majority of our time was spent researching and building out the inventory of names on our possible buy list.

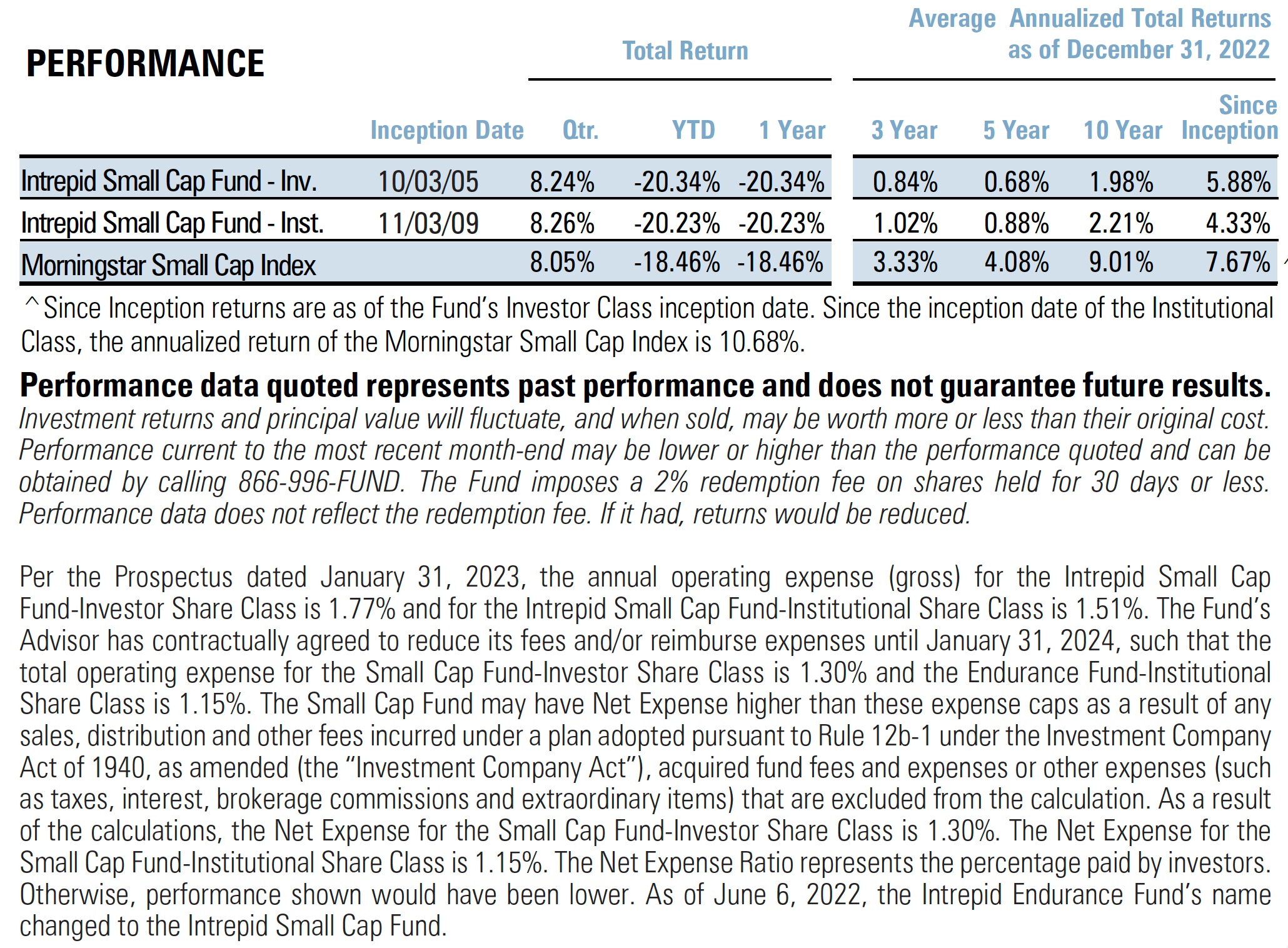

Performance

The movement in small cap stocks during calendar Q4 reflected changes in investor sentiment over which sort of landing is more likely in 2023. They rallied early in the quarter on decelerating inflation before paring gains later in the quarter. Most small cap indices ended the quarter up a mid- single-digit percentage.

For the quarter ended 12/31/22, the Fund returned 8.26%, slightly outperforming the 8.05% return of its benchmark Morningstar Small Cap Index. We are pleased with this outperformance in light of a higher than normal cash level throughout the quarter. As a reminder, the Fund has the ability to hold dry powder in the form of cash (or treasuries) which we limit to no more than 20%. During calendar Q4, the Fund’s average cash holdings were approximately 12%.

For the year ended 12/31/22, the Fund returned -20.23% compared to -18.46% for its benchmark. Although the underperformance is small on a relative basis, it was exceedingly disappointing. While mindful of our benchmarks, we have always placed a high importance on absolute returns and strive to avoid drawdowns of this magnitude. The Fund’s underperformance can mostly be explained by a negative contribution from a few names in the cannabis industry, which mostly took place in calendar Q1 2022. We have written about the cannabis sector in prior letters and currently have zero exposure.

Contributors & Detractors

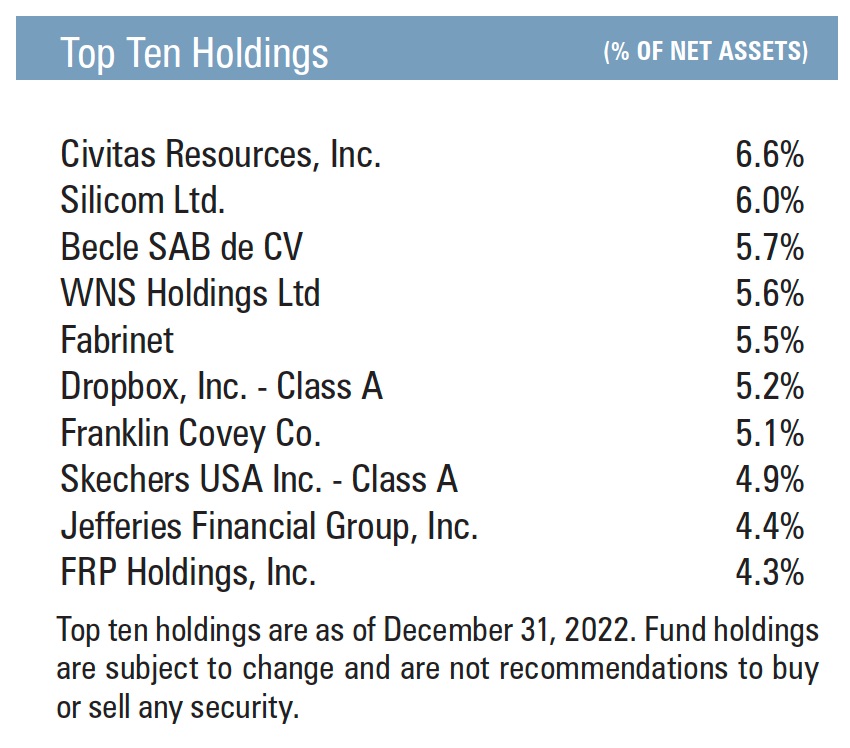

The three largest contributors to the Fund’s performance for the quarter were Fabrinet (FN), Skechers USA (SKX) and Becle SAB (CUERVO). The three largest detractors were Pagseguro (PAGS), IAC Interactive (IAC) and Delta Apparel (DLA). The share prices of PAGS and IAC sold off during the quarter on what we believe are temporary challenges, and their declines were probably exacerbated by year-end tax loss selling. Delta Apparel similarly struggled through a temporarily tough retail apparel environment, but we sold the position due to elevated financial leverage after revising our earnings expectations.

For the calendar year ended 12/31/22, the three largest contributors to performance were Civitas Resources (CIVI), Fabrinet (FN) and Franklin Covey (FC). The three largest detractors to performance were Atento (ATTO), IAC Interactive and Verano Holdings (VRNOF). The Fund no longer owns a position in Atento or Verano. IAC is one of the Fund’s few “long duration” holdings and sold off sharply this year on challenges at two of its largest subsidiary companies, as well as its “growth” style in a rising interest rate environment. IAC is a holding company led by a strong management team with a history of excellent value creation through capital allocation, and we believe the sum of its parts is worth significantly more than where the shares trade today.

Positioning & Outlook

Seven of the Fund’s top eight holdings had zero net debt at the end of 2022 (39% of overall portfolio). As such, we believe that it is relatively well positioned to withstand any further economic weakness that we may encounter in 2023. Similarly, the Fund’s 13% cash level to begin the year should provide ample reserves if small caps experience significant market volatility. Should stocks rebound higher throughout 2023, we believe the Fund’s holdings – which we try to concentrate in niche market leaders – will participate in such a rally.

As usual, we are not selecting securities based on any view of the broader economy or market. We underwrite small cap stocks with a multi-year perspective based on normalized (i.e. mid-cycle) earnings. When these stocks meet our business quality and valuation criteria, we are comfortable holding them through the cycle. While we hope for a healthier equity market in 2023, we are preparing for more volatility. We have our shopping list at the ready and welcome the opportunity to increase the Fund’s exposure at more attractive prices.

Thank you for your investment.

Matt Parker, CFA, CPA

Intrepid Endurance Fund Co-Portfolio Manager

Joe Van Cavage, CFA

Intrepid Endurance Fund Co-Portfolio Manager