January 1, 2024

Dear Fellow Shareholders,

There is a popular saying in many areas that goes: “if you don’t like the weather, wait a few minutes.”

The same could be said of sentiment in the stock market, and Q4 was a prime example. In the last few weeks of Q3, interest rates surged, oil prices rocketed higher, and stocks tumbled. The chief concern was the rapidly rising level of treasury rates, which had just made 15-year highs. Prominent commentators suggested that the market was in a new regime and was headed for much higher rates. Calls for a recession grew louder.

What a difference a few months can make! As fears subsided with cooling inflation readings, the Fed surprised the market in December with a projection for rate cuts in 2024 (not just a “pause”). For investors conditioned to monetary stimulus, this was the “all clear” Pavlovian bell. The market then appeared convinced that a “soft landing” with accommodative monetary policy had been achieved. Small cap stocks, which are generally seen to be more economically sensitive than larger stocks, rallied sharply in the last three weeks of December to notch a great quarter.

While we don’t tend to view markets from the top-down, it’s hard not to say that the odds of a soft landing have improved. Inflation appears to be leveling off at a more manageable level. Supply chains have recovered. Consumer demand still looks to be in decent shape and company earnings have held up reasonably well. Credit spreads ended the year at their lows and look poised for a more friendly financing environment in 2024.

However, it seems premature to declare victory. This hiking cycle – one of the most aggressive in decades – ended less than six months ago, and many economists believe it can take over a year for increases to be felt in the real economy. Furthermore, we wouldn’t say that earnings this quarter were stellar. For many of the more economically sensitive businesses we follow, management teams cited outlooks that reflected deteriorating conditions and slowing discretionary consumer spending.

We have tried to invest the majority of the Intrepid Small Cap Fund’s (“the Fund”) capital in defensible businesses with strong balance sheets, while maintaining a small buffer of cash. This positioning tends to be more conservative than the broader market, which means it often underperforms during short-term risk-on periods in which the market disproportionately rewards riskier companies. We balance this against an expectation to outperform during risk-off periods, as well as a view that a concentration in higher quality companies trading at attractive prices is likely to outperform over a full market cycle.

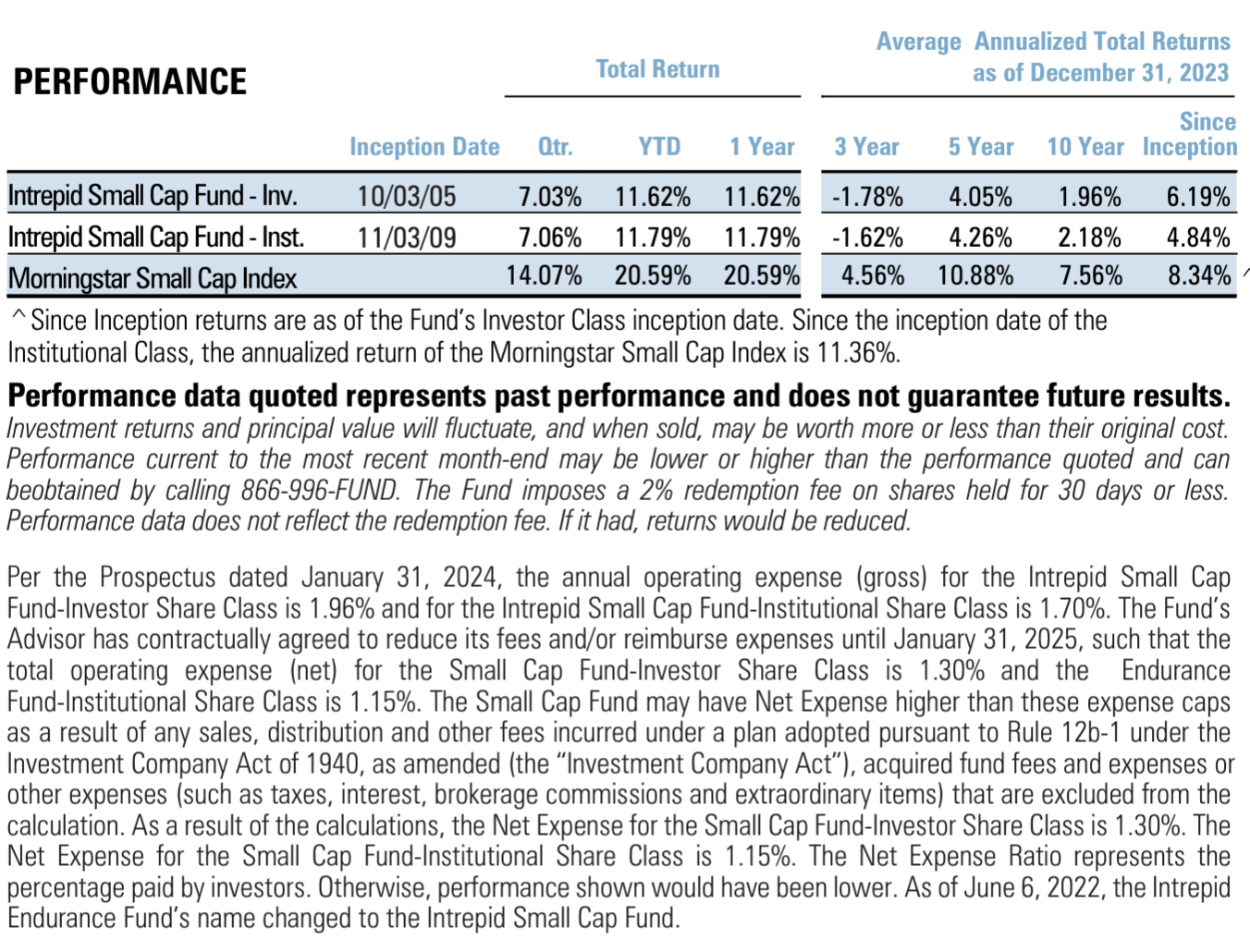

The fourth quarter of calendar 2023 was one of these short-term bouts of upside volatility in which the Fund did not keep up with the broader small cap stock indexes. It also happened to be a quarter in which two of the Fund’s larger holdings had poor results that weighed on overall returns. As a result, the Fund returned 7.03% for calendar Q4 2023 compared to 14.07% for the Morningstar Small Cap Index.

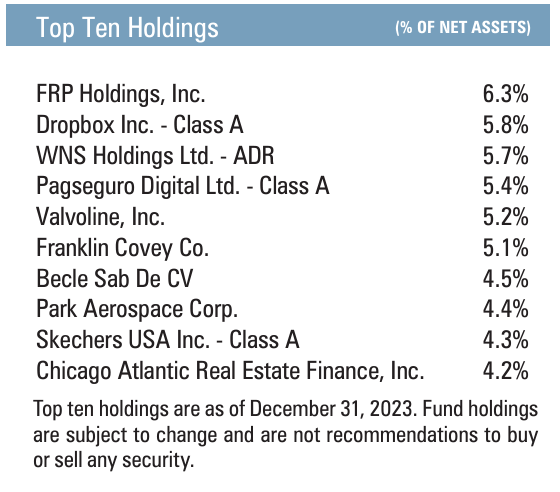

The two poor performers were Silicom Ltd (SILC) and Becle SAB de CV (CUERVO) and both were outsized weights coming into the quarter. However, our reaction to each was very different.

Becle, the largest producer of tequila worldwide, posted disappointing results for Q3. Everything went wrong for Becle: demand declined sharply in all geographies outside of North America, input costs increased and squeezed gross margins, and advertising and corporate costs all grew despite the lower top line and gross margins. However, while this was a very poor quarter, there are green shoots ahead for Becle in the ability to rein in corporate costs as well as a long-awaited relief in agave input costs over the next several quarters. In the meantime, they continue to build upon their leading market share in tequila and Irish whiskey with their top-notch brands.

The outlook for Silicom is not as bright. The company reported a significant and sudden pause in demand as their telecom customers sat in an over-inventoried position. While that can happen, what made it harder to stomach is that the company admitted that customers were using this pause to renegotiate margin terms for Silicom, putting its historic mid-30% gross margins at risk and creating a significant risk to its business model. Despite a pristine balance sheet and high insider ownership, the visibility into the future cash flows at Silicom is simply not as clear as it is for Becle. As a result, we kept our Becle holding but jettisoned Silicom during the fourth calendar quarter.

The top-3 contributors to performance were Pagseguro (PAGS), Skechers (SKX), and Armstrong World Industries (AWI). Pagseguro and Armstrong World Industries both benefitted from very inexpensive valuations to start the period and were beneficiaries of the declining in interest rates during Q4. Skechers reported a very strong Q3 2023 result.

The Fund purchased one new holding this quarter: Helios Technologies (HLIO). Helios is an industrial business that makes hydraulic valves and electronic controls that are used in a number of different end markets. We previously owned the stock and sold it in early 2023 as it appreciated beyond our intrinsic value estimate. We were pleased to be able to buy it back again at a favorable price after it reported a disappointing Q3 earnings.

There were a number of stocks that approached our desired entry price levels early during the quarter. However, buying activity was generally slow in the quarter (particularly in December) as stocks marched higher. However, we did use this period of optimism to trim a handful of positions.

Looking forward to 2024, there have been no major changes to positioning or approach. We continue to hunt for high quality small companies trading at attractive prices. The Fund ended the year with cash of 5.7% that can be deployed in the event that market volatility returns. If small caps continue to grind higher, we would expect to monetize more of our holdings and gradually build cash reserves.

If you have any questions or would like to discuss any of our holdings in more detail, please don’t hesitate to give us a call.

Thank you for your investment.

Matt Parker, CFA, CPA

Intrepid Endurance Fund Co-Portfolio Manager

Joe Van Cavage, CFA

Intrepid Endurance Fund Co-Portfolio Manager