October 1, 2023

Dear Fellow Shareholders,

The third quarter of 2023 began with a carryover of the benign market environment that we wrote about last quarter. Despite a steady rise in interest rates, volatility remained subdued and small cap stocks marched higher, with the Russell 2000 returning over 6% in July.

Conditions in August and September, however, were much more volatile. Oil prices and long-term interest rates screamed higher, with the 10-year treasury reaching its highest level since 2007. Small caps tumbled, reversing their July gains and ending the quarter down -5.1% (as measured by Russell 2000).

The surge in interest rates later in the quarter remains front and center on investors’ minds. Unlike similar treasury selloffs we saw in 2022, however, this spike in rates came when headline inflation was much lower. Now investors are wondering (1) if higher rates are here to stay and (2) if so, can the economy and asset prices digest them without much pain. Predictions vary, but confidence does not (reminding us of the old phrase “often wrong, never in doubt”).

Some argue that rate increases are explained by a healthy acceleration of economic expansion, pointing to metrics like real wage growth and low unemployment. These optimists tend to believe stock prices are well supported and can move higher. On the other hand, some bears blame a supply/demand mismatch in the treasury issuance market and point to an unsustainable fiscal deficit (return of the bond vigilantes?). They believe rates are poised to move higher and stocks to move lower. Others say that this is simply a return to a more normal interest rate environment after a central bank-driven historical anomaly for much of the last decade.

We’re thankful that our investment process doesn’t require us to diagnose every wiggle in the treasury market or predict where rates will go next. However, we prefer to err on the side of caution and invest as if rates will remain higher instead of wagering that we’re on the brink of a return to the

loose money policy that defined the last decade. That means constructing a portfolio of businesses with strong balance sheets that aren’t dependent on the debt markets to keep them afloat.

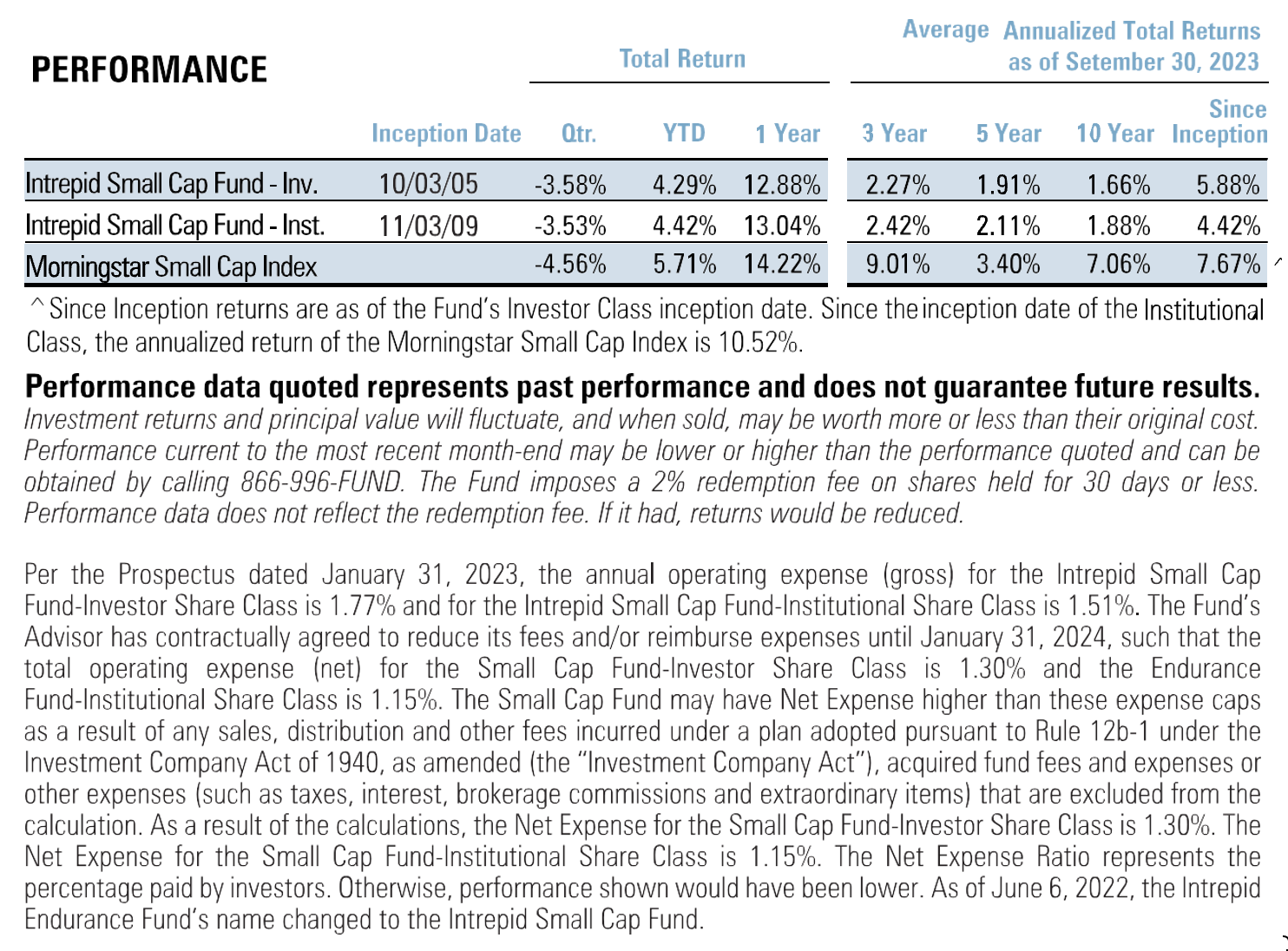

The Intrepid Small Cap Fund (“the Fund”) returned -3.53% during the quarter, slightly outperforming the -4.56% return of its benchmark Morningstar US Small Cap Index. For the Fund’s fiscal year ended September 20, 2023, it returned 13.04% versus 14.22% for its benchmark. As value investors focused on downside protection, we sometimes say that we aim to participate in bull markets and protect in bear markets. While we aren’t happy to trail our benchmark, we are reasonably pleased to have captured over 90% of the upside in what was a strong last twelve months for small caps.

The Fund’s relative performance this quarter was also a tale of two halves. It lagged small cap indices by a wide margin when small caps rallied in the beginning of the quarter, before outperforming by an even wider margin as stocks fell later in the quarter. We normally expect a healthy amount of tracking error vs our benchmark given the concentrated nature of our holdings and our high active share. While this was abnormally high even by our standards, it is not the result of any major changes to the portfolio.

The three largest contributors to the Fund’s performance for the quarter were Fabrinet (FN), Park Aerospace (PKE) and Civitas Resources (CIVI). The three largest detractors were Silicom (SILC), IAC Interactive (IAC) and Valvoline (VVV). We continue to own each of these detractors and believe that the selloffs during the quarter were due to temporary issues rather than deterioration in long-term fundamentals.

For the fiscal year ended September 30, the three largest contributors were Fabrinet, Civitas Resources and Skechers (SKX), and the three largest detractors were Silicom, Pagseguro (PAGS) and WNS Holdings (WNS).

Trading activity has been higher than normal in the last several weeks as market volatility has picked up. In general, you should expect us to be more active in choppy markets as it’s more likely there will be dislocations from our fair value estimates.

We think the Fund is positioned well in the event that credit markets continue to tighten. Of our top-ten holdings, five have net cash and only two have above one turn of net leverage. As we look forward to a potentially more volatile market in upcoming quarters, our game plan remains the same as it has in similar periods of market stress:

- Prioritize strong balance sheets – Security selection will emphasize businesses that can comfortably withstand a higher rate This is not to say that we wouldn’t buy any company that had meaningful debt, but instead, that the discounts we will require to own these businesses will be greater.

- Maintain cash buffer – The fund will hold a 5-10% position in cash (or short-term money market instruments) to serve as dry powder that can be deployed into attractive opportunities should markets draw

- Capitalize on volatility – Continue to use bouts of volatility to our advantage by adding exposure to stocks that become more attractive and trimming from those that become less

In the context of a macroeconomy that seems highly uncertain, we find it helpful to stay focused on the dozens of businesses that we understand extremely well. We believe our simple strategy of investing in good businesses at good prices will produce attractive results over full market cycles, which eliminates the need for us to constantly change our approach as the winds shift.

If you have any questions or would like to discuss any of our holdings in more detail, please don’t hesitate to give us a call.

Thank you for your investment.

Top Contributors in Q3 2023 Top Detractors in Q3 2023

Fabrinet (FN) Silicom Ltd. (SILC)

Park Aerospace (PKE) IAC Interactive (IAC)

Civitas Resources (CIVI) Valvoline (VVV)

Top Contributors in Fiscal Year 2023 Top Detractors in Fiscal Year 2023

Fabrinet (FN) Silicom Ltd. (SILC)

Civitas Resources (CIVI) Pagseguro Digital – Class A (PAGS)

Skechers USA – Class A (SKX) WNS Holdings – ADR (WNS)

Matt Parker, CFA, CPA

Intrepid Endurance Fund Co-Portfolio Manager

Joe Van Cavage, CFA

Intrepid Endurance Fund Co-Portfolio Manager