April 1, 2023

Dear Fellow Shareholders

Similar to last quarter, small cap stocks again showed how volatile they can be during calendar Q1 2023 (the 2nd quarter of fiscal 2023).

Small caps rallied hard to start the period, rising over double digits by early February. However, the well-publicized banking crisis that emerged in early March pushed them all the way back into negative territory. From there, small caps rallied in the last few weeks to end the quarter with slightly positive returns.

The concerns about the banking system came out of left field during the quarter. We certainly did not expect it.

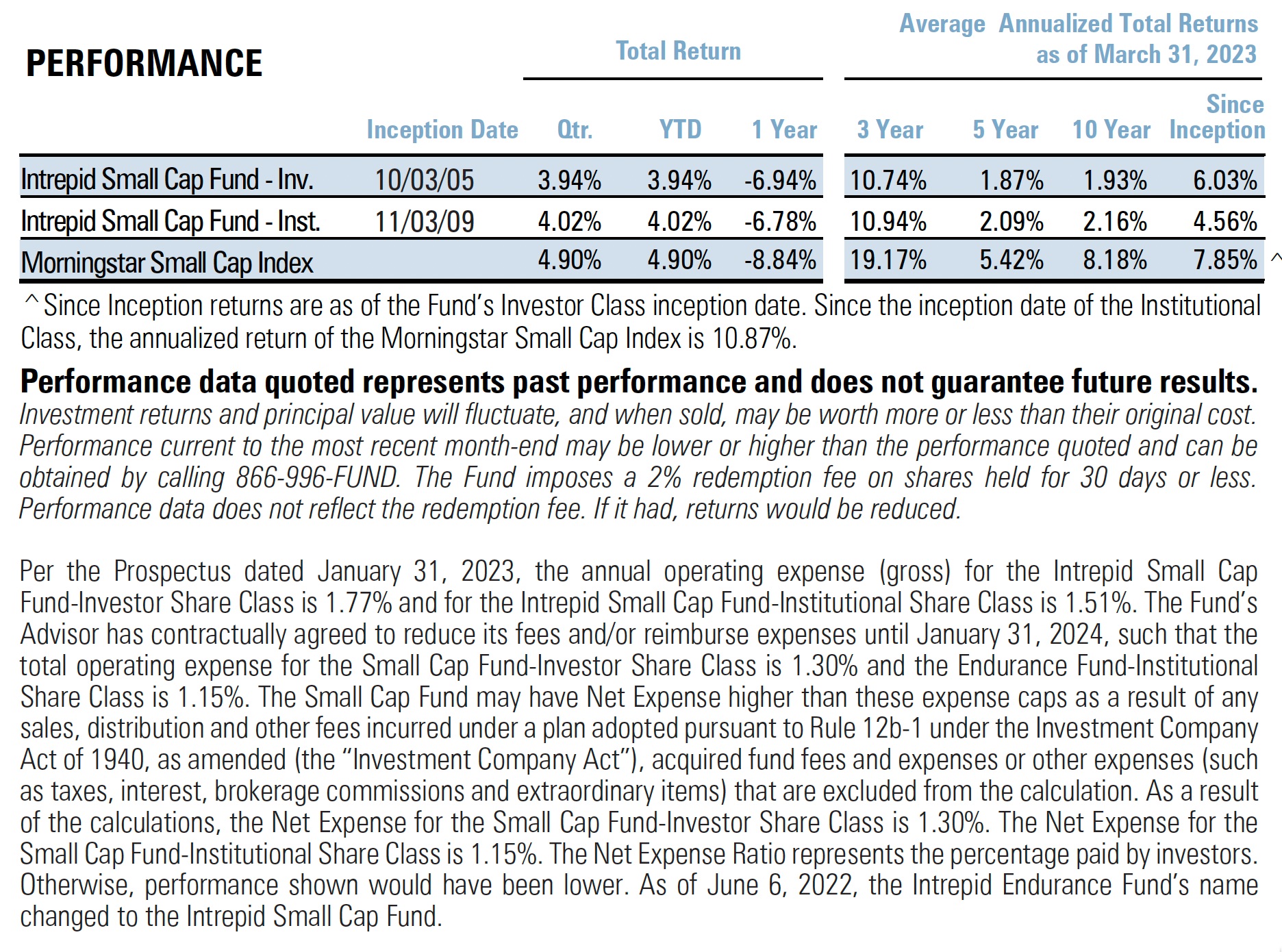

However, the Fund was positioned reasonably well for it, with only one traditional bank stock in the portfolio and at a very small weight. For the quarter, the Intrepid Small Cap Fund (“the Fund”) returned 3.94% versus 4.90% or the benchmark Morningstar Small Cap Index.

As a general rule, we do not invest much in the bank sector, despite it being a rather large part of the small cap market. Banks are very difficult to analyze or value with confidence and – as seen in the last few weeks – have black swan risks on both the asset and liability sides of their business. In addition, it’s a competitive industry with very few companies that possess the type of durable competitive advantages we look for. That is not to say that we would never invest in them; however, under normal circumstances we would anticipate having little banking exposure.

Besides the banks stocks themselves, another difficult thing to analyze is what the economic impact from the crisis will be. Now that things have calmed down and some confidence has been restored, will the economy go right back to normal? Or will the financial system pull back on credit growth in order to keep cash available for future deposit runs, stifling the economy in the second half of the year?

These questions lead to more questions, and there are a lot of investors

guessing about what happens next. If the economy does slow, will the Fed stubbornly continue to tighten? Or will they relent and lower rates? When will they decide? And at what pace will they raise or lower rates? Is quantitative easing back on the table to improve liquidity in the system?

As usual, we believe trying to answer these questions is counter-productive to our task of trying to source high quality small cap companies at attractive valuations. Instead, we often use periods of high uncertainty that drive questions like the above and thus higher volatility to source new positions that meet our investment criteria.

For instance, we added three new positions to the Fund in calendar Q1 (compared to zero new positions in calendar Q4):

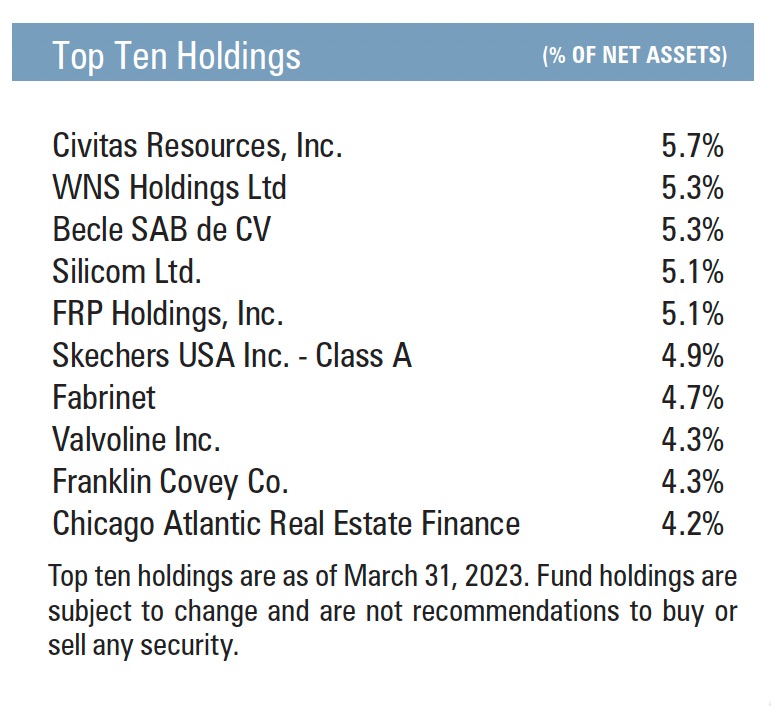

- Chicago Atlantic Real Estate Finance (REFI) is real-estate investment trust that focuses on providing short-term term secured loans to the legal US cannabis After some unsuccessful attempts to benefit from the capital-constrained cannabis industry in the past, we have decided to move up in the capital structure to take advantage of the attractive and well-covered loans that scaled lenders to the space are able to make. In addition, for a REIT the company has little leverage and a very attractive dividend (over 10%).

- Armstrong World Industries (AWI) is the leading manufacturer of ceiling systems in the United States. Assuming that you are in an office building reading this letter – if you look at the ceiling tile above your head, there is a greater-than-50% chance that Armstrong manufactured As a dominant market share leader in a low growth industry that supplies a very small component of the cost of new build and remodel projects, Armstrong has demonstrated very robust pricing power even before the recent bout of high inflation.

- Vector Group Ltd (VGR) is the fourth-largest manufacturer of cigarettes in the US, specializing in the discount and deep discount From a decades-old legal settlement that awarded them favorable tax treatment, the company has a structural cost advantage versus its peers that management exploits by launching new brands that undercut competition in order to gain market share. After establishing distribution and customer loyalty with the new brand, Vector implements the typical tobacco playbook by raising prices which sheds some market share but drives significant incremental profitability that more than compensates for the lost share. We believe the company is entering one of its profit harvesting periods today, which is an especially attractive time given that many consumers are trading down to the discount cigarette category.

The three largest contributors to the Fund’s performance for the quarter were Civitas Resources (CIVI), Becle Sab de CV (CUERVO MM) and WNS Holdings (WNS). The three largest detractors to performance were Franklin Covey (FC), Silicom (SILC) and Conduent (CNDT). We believe the selloff in each of these stocks was mostly due to temporary challenges and investor frustration surrounding earnings, but have not changed our favorable view of their long-term fundamentals.

Despite the three new holdings, positioning remains largely the same today as when we began the quarter. The top positions in the Fund continue to possess what we believe is the best combination of business quality and valuation. In addition, we continue to emphasize financial strength – only one of the top seven holdings has net debt. While the banking crisis has caused longer-term interest rates to fall dramatically over the last month, we still value balance sheet strength and liquidity as an important risk mitigator in the volatile small cap market.

With that said, two of the three new names described above (Armstrong World Industries and Vector Group) do have some debt. It’s an important point to mention – we are not afraid of debt, we just want to make sure that our holdings that have debt:

- Have stable, consistent operations to support the debt

- Have ample liquidity and no near-term debt maturities

- Are priced adequately for the higher risk

While we are not going full-throttle into highly levered small cap opportunities, it is not terribly surprising that – given the elevated volatility in the credit markets – we have found more opportunities in companies with debt recently. For instance Armstrong World trades at the lowest valuation it ever has since the spin-off of its flooring business in 2016. And at approximately 10x earnings, we believe Vector Group’s potential for attractive near-term earnings growth (and high dividend) are being ignored. We believe both of these opportunities exist partially because of the companies’ not-quite-pristine balance sheets.

We will continue to remain flexible and try to take advantage of what the market offers, with the goal of generating attractive risk-adjusted returns in what is often a volatile small cap market.

Thank you for your investment.

Matt Parker, CFA, CPA

Intrepid Endurance Fund Co-Portfolio Manager

Joe Van Cavage, CFA

Intrepid Endurance Fund Co-Portfolio Manager