January 1, 2024

Dear Fellow Shareholders,

Calendar year 2023 was a year of significant sentiment shifts across fixed income markets. The year started off with

high inflation taking a toll on long duration and higher-quality credits, which was exacerbated by an ominous run on bank

deposits at several large commercial banks and fears of an imminent recession.

Conversely, the year ended on a much more positive tone, with investors increasingly sanguine about a “soft landing” for

inflation and credit risk – driving strong returns throughout all fixed income categories in this most recent quarter.

We reacted to each of these changes in sentiment as follows:

- Early in the year, we aggressively purchased high quality credits as investors pressured by capital runs

liquidated these securities to boost liquidity. - As the year ended, and investors regained more confidence in a “soft landing” economic scenario, we

trimmed some of our riskier and less liquid positions.

We do see the likelihood of an economic “soft landing” as higher than before. The rate of inflation in the United States has consistently slowed throughout the second half of the year. And just as important, the economy has held up reasonably well despite the rapid rise in interest rates orchestrated by the Federal Reserve.

In that vein, the Fed has now communicated not only a “pause” in interest rate hikes, but in December surprised the market by projecting the need for multiple rate cuts during 2024. This caused many investors to snap into a pattern recognition mode that anticipates imminent rate reductions and a return to a bond market with low volatility (driven by the tailwind of falling rates) – quite a difference from the highly volatile experience of the last two years as rates steadily rose. This change in Fed communications sparked a massive rally to end the year.

As stated in past quarterly letters, we continue to believe a return to a multi-year bond melt-up driven by an accommodative

central bank is unlikely – or, at the very least, that it is premature to assume it will happen. One of the inconsistencies with

that outlook is that for significant rate cuts to happen, there likely needs to be a meaningful weakening of the economy,

housing, and/or labor market. Were the Fed to cut rates prior to that, they increase the risk of a reacceleration in inflation.

A 1970’s-style rebound in the inflation rate after an initial ebb would be contrary to the Fed’s mandate and likely necessitate

another, more bearish “pivot” in interest rate policy (this time to start hiking rates again).

As such, we view the current market outlook of six rate cuts by the end of 2024 as presumptive of a significant slowdown

in economic activity. While possible, and there are sectors of the economy that have weakened in the second half of the

year, the economy has likely remained much too resilient, at least so far, to justify that violent of a turn in the rate cycle.

However, we have no special insight on what the future holds for the economy over the next year. We do think that should

the market be correct and the economy weakens enough to justify a half dozen interest rate cuts, that is not an ideal

setup for riskier credits that depend on a growing economy to maintain acceptable leverage metrics. Thus, we found it an

opportune time to lighten up on our holdings with higher leverage or more economic sensitivity.

Despite this action, we continue to think there is a tremendous opportunity for fixed income investors to earn equity-like

returns in short duration high yield without taking on equity-like risk. With a current yield of 7.9% and a yield-to-worst of

9.4%, we believe the Intrepid Income Fund offers a very attractive option for investors – especially given the recent actions

dedicated to reducing the more risky holdings within the Fund. Our short duration bias remains strong, with a modified

duration of 2.0, allowing us to remain nimble and take advantage of future opportunities should markets become less

sanguine about a “soft landing” over the coming year.

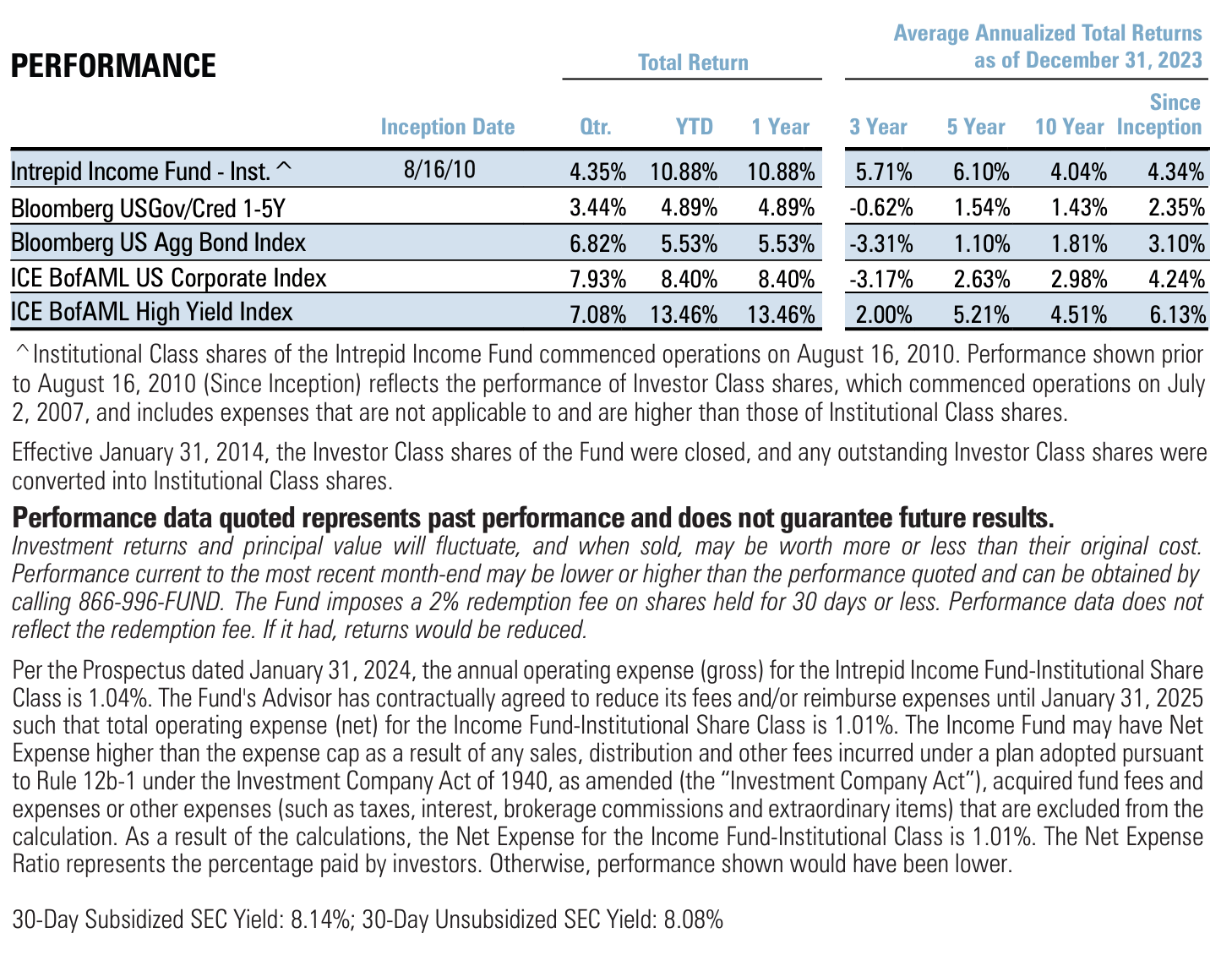

Shifting to performance, the Intrepid Income Fund (the “Fund”) returned 4.35% for the quarter ended December 31,

2023. While a very satisfactory absolute return for one quarter, this did trail the duration-heavy Bloomberg US Aggregate

Bond Index’s return of 6.82% due to the index benefitting from the aforementioned rapid decline in rates to end the

period. In contrast, the Fund outperformed the 3.44% return for the shorter-duration Bloomberg US Govt/Credit 1-5

Year Total Return USD Index, which is our other benchmark.

Both the ICE BofAML US Corporate Index and ICE BofAML High Yield index reported very strong returns in

the quarter (7.93% and 7.08%, respectfully), driven by the decline in both interest rates as well as the market’s

perception of credit risk.

It is typical for the Fund to underperform fixed income indices with higher inherent duration during periods of sharp

interest rate declines that spur price-driven rallies in bonds. Given the Fund’s high income focus (we are the Intrepid

Income Fund, after all) and short duration bias, most of its returns are typically driven by the coupon and interest income

that its holdings generate over time. Thus, when credit markets are being driven by rapidly declining rates and the associated

price appreciation, such as in calendar Q4, our goal is to continue generating attractive returns, but without taking on risk

that we are not adept at navigating/forecasting around.

The Fund’s strategy is designed to generate attractive returns through all market environments and not just those where

bond prices are rising rapidly. With the Fed’s recent communication, it appears that the market may have just finished

a very challenging rate hiking cycle for fixed income investors. If that is the case, we are pleased with the Fund’s overall

performance in what proved to be a difficult environment since the first rate increase was announced by the Federal

Reserve on March 16, 2022.

The Fund’s total return from that date through the end of calendar 2023 was +8.38%, which handily outperformed the

negative total return for the Bloomberg US Aggregate Bond Index (-2.70%), the slightly positive total returns for the

Bloomberg US Govt/Credit 1-5 Year Total Return USD Index (+1.87%), and the ICE BofAML US Corporate Index

(+0.57%). The Fund also outperformed the ICE BofAML High Yield Index’s return of +7.51% through this period.

The Fund’s success during this period of rapidly rising rates was attributable to both its short duration positioning as well

as its steadfast focus on circumspect credit underwriting in what was an uncertain macroeconomic period. As always, we

welcome outreach and would love the opportunity to discuss our past and current positioning with you.

To summarize our thoughts looking forward, we still believe it is too early to assume we are returning to a regime where

blindly reaching for high quality duration will be a durable, winning strategy. We believe that longer duration fixed income

strategies, which were considered “core” strategies before the current interest rate regime, will continue to be volatile, and,

because of this volatility, will not offer very “fixed” rates of return.

We remain focused on finding idiosyncratic, short duration credits that offer attractive risk/reward prospects and the

ability to reinvest called and matured proceeds into future opportunities as they emerge. While the Fund has de-risked

a bit in response to a more positive monetary outlook, we have been able to replace these positions with attractive core

holdings that preserve a solid yield profile and possess the characteristics we demand of low leverage, stable operations,

creditor-friendly capital allocation, and a margin of safety should a downside case play out.

We also will look to be opportunistic in layering in unique longer-duration opportunities in high quality credits that we

know well when offered at attractive yields. If successful, this will allow the Fund to participate more in the price-driven

upside should rates continue to fall as the market expects, while still preserving the strong credit quality and yield metrics

of the Fund.

While the market is pricing in a new, bullish rate cycle and an “all clear” on a “soft landing,” we believe continuing to

emphasize our diligent credit underwriting philosophy will provide attractive risk-adjusted returns to Fund shareholders

while protecting them should there be a return to credit market volatility in 2024.

As always, thank you for your investment.

Sincerely,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Hunter Hayes

Intrepid Income Fund Co-Portfolio Manager