January 7, 2023

Dear Fellow Shareholders,

This time last year, we wrote about how unappetizing credit markets appeared to us. The ICE BofA US High Yield Index (the “HY Index”) ended 2021 with a yield-to-worst of 4.32%, not too far above its all-time low. One year later, the index now carries nearly double that yield, ending 2022 with a yield-to-worst of 8.63%. A relentless hunt for yield has subsided into a craving for safety and security. As lenders begin contemplating the return of principal, not just the return on principal, we believe that credit markets are much more appetizing today, despite the risks that remain.

One of the most formidable of those risks is rising rates. Although we believe that rates will remain higher for longer, we will stop short of making any precise interest rate forecasts. Just look back at interest rate predictions from economists a year ago, which were off by several orders of magnitude, to see why we prefer to position ourselves in a way that does not require precise predictions. Rather, we seek to remain nimble as we adapt to a rapidly changing environment.

There are two common-sense ways for a fixed income investor to mitigate the uncertainty of interest rate movements – one is to lend for short amounts of time, such that an investor can redeploy capital as the environment shifts,

and the other is to lend money on a floating-rate basis, such that a lender benefits from a move higher in interest rates (but, conversely, also loses out on interest income if rates move lower). We have continued to employ both methods in the Intrepid Income Fund (the “Fund”), ending the calendar year with a modified duration of 2.27 years, and with 13.3% of the portfolio in floating-rate securities.

and the other is to lend money on a floating-rate basis, such that a lender benefits from a move higher in interest rates (but, conversely, also loses out on interest income if rates move lower). We have continued to employ both methods in the Intrepid Income Fund (the “Fund”), ending the calendar year with a modified duration of 2.27 years, and with 13.3% of the portfolio in floating-rate securities.

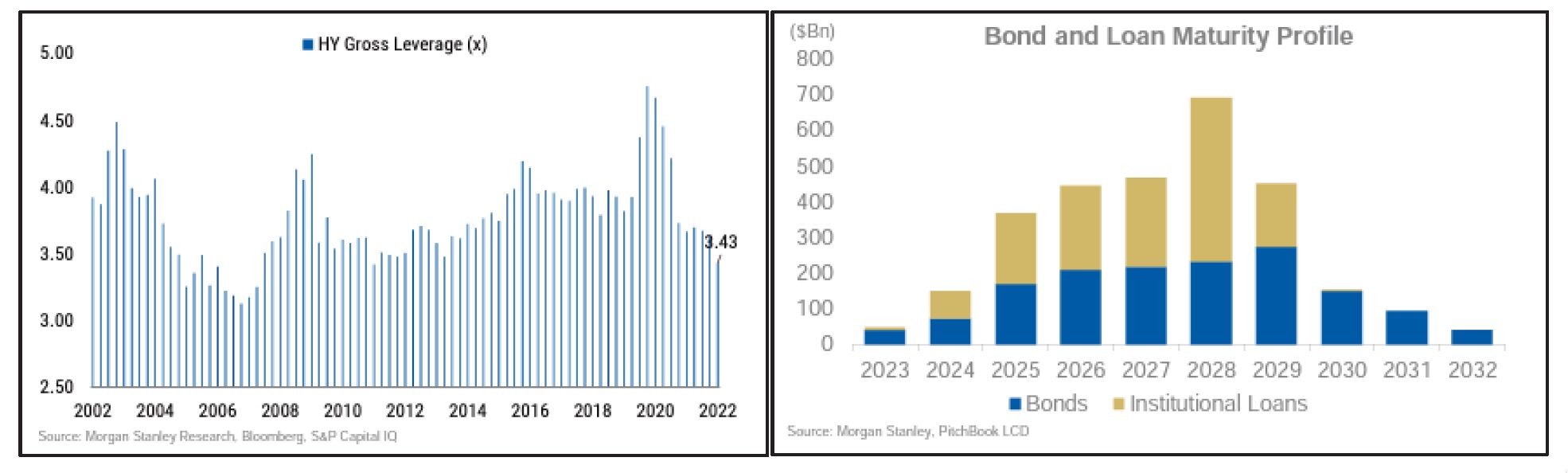

Rates aside, the fundamental picture for junk bond issuers is relatively robust. Gross leverage for the HY Index is a healthy 3.43x, as shown in a chart from Morgan Stanley below, and the heaviest year of debt maturities for high-yield bonds and leveraged loans is not until 2028. Many high-yield issuers are well capitalized, with low-coupon, fixed-rate debt that does not mature until later this decade, and strong cash positions that should bolster balance sheets through a downturn.

This is not to say that we expect smooth sailing from here. Quite the contrary – it is likely that the Federal Reserve will continue raising rates in its quest to quell inflation, possibly leading to a recession. However, we believe that at today’s levels, pockets of fixed income provide a compelling entry point.

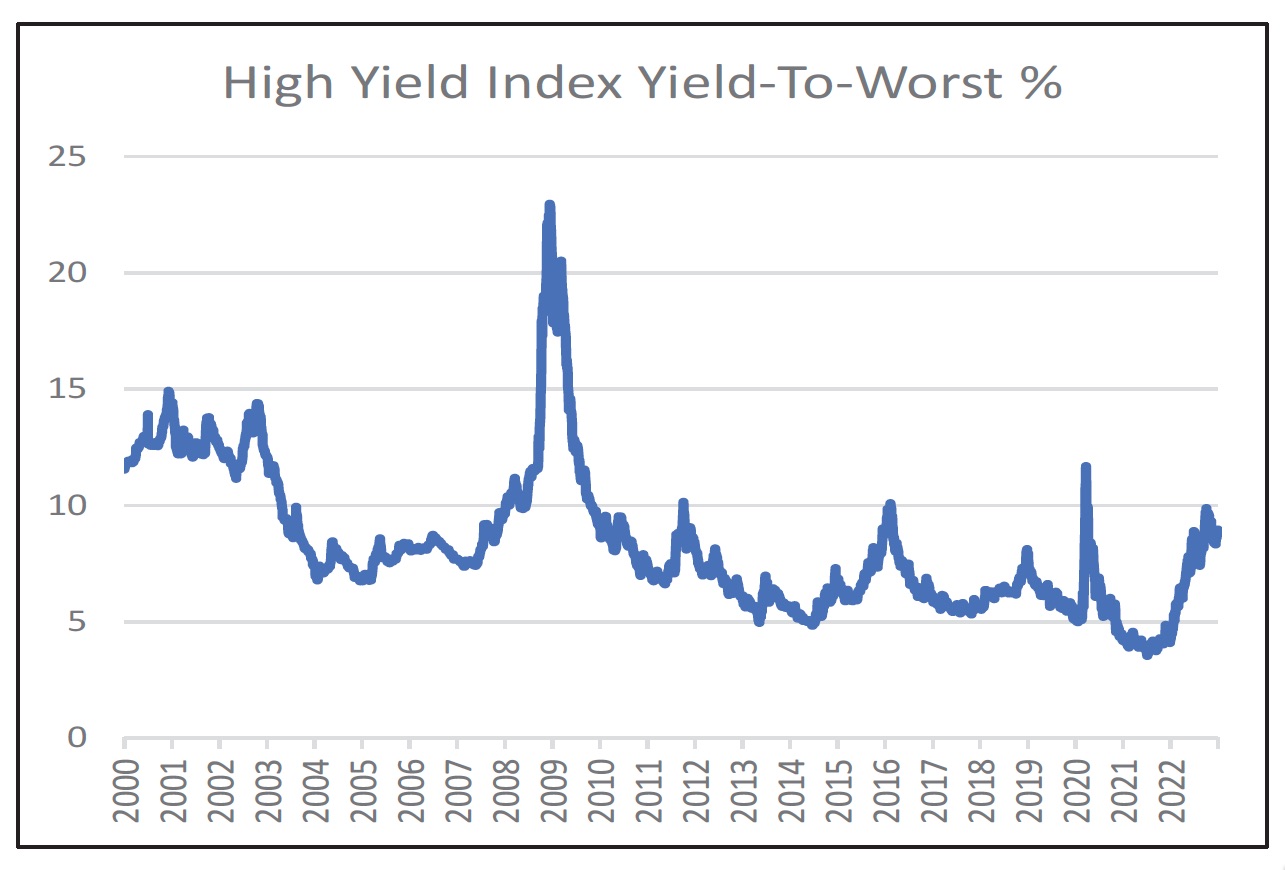

As the chart to the left shows, the yield-to-worst on the HY Index tends to be cyclical. The median yield-to-worst since 2000 is 7.56%, over 100 basis points below the level at the end of 2022. We can foresee scenarios in which yields tighten from here and we can also foresee scenarios in which yields blow out to double-digits. In either case, for an investor with a holding period of more than a year, we believe that there is compelling reward for the relative level of risk. Solid credit work will remain key, as many of the zombie companies that were kept alive by easy money policies will likely struggle through this period.

As the chart to the left shows, the yield-to-worst on the HY Index tends to be cyclical. The median yield-to-worst since 2000 is 7.56%, over 100 basis points below the level at the end of 2022. We can foresee scenarios in which yields tighten from here and we can also foresee scenarios in which yields blow out to double-digits. In either case, for an investor with a holding period of more than a year, we believe that there is compelling reward for the relative level of risk. Solid credit work will remain key, as many of the zombie companies that were kept alive by easy money policies will likely struggle through this period.

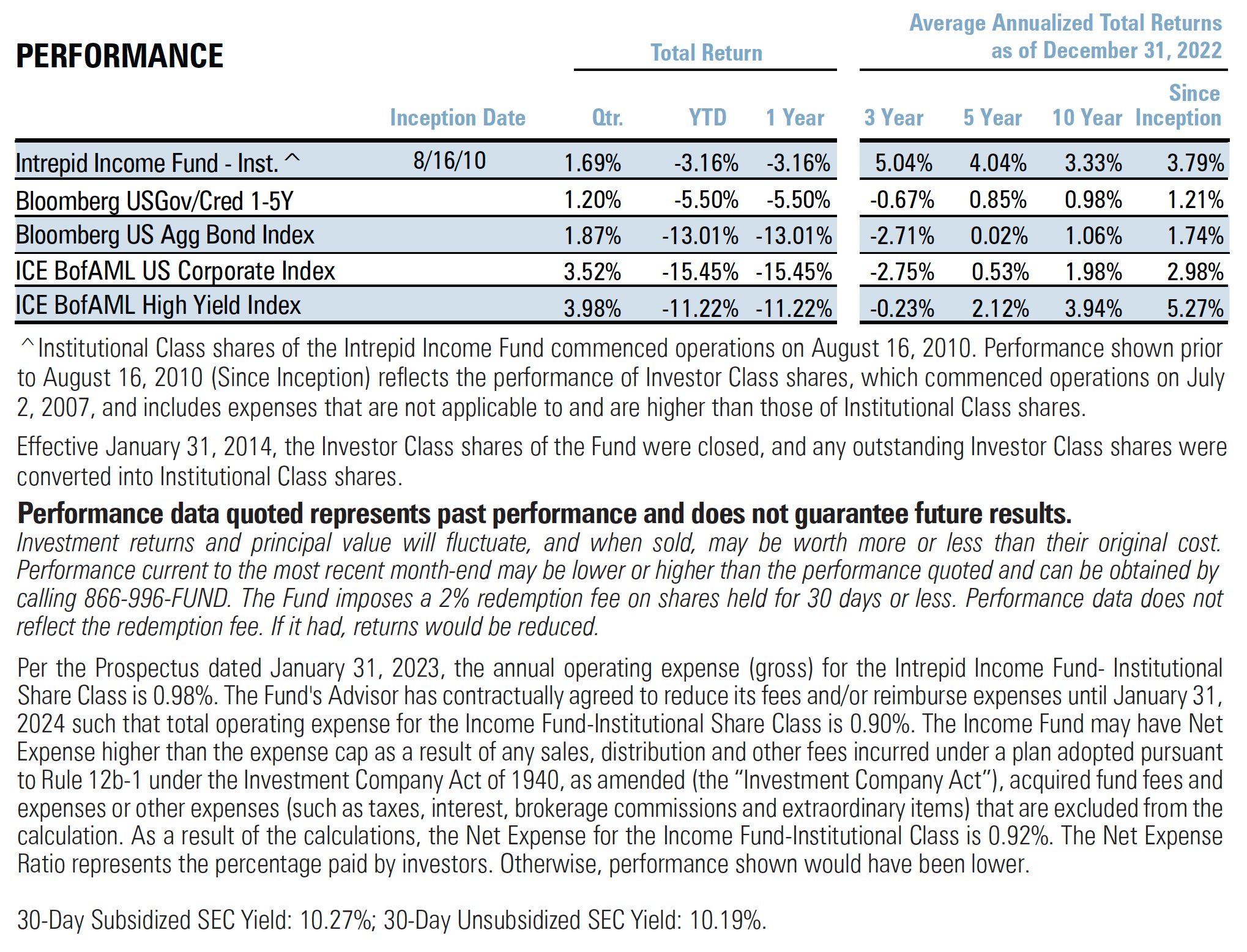

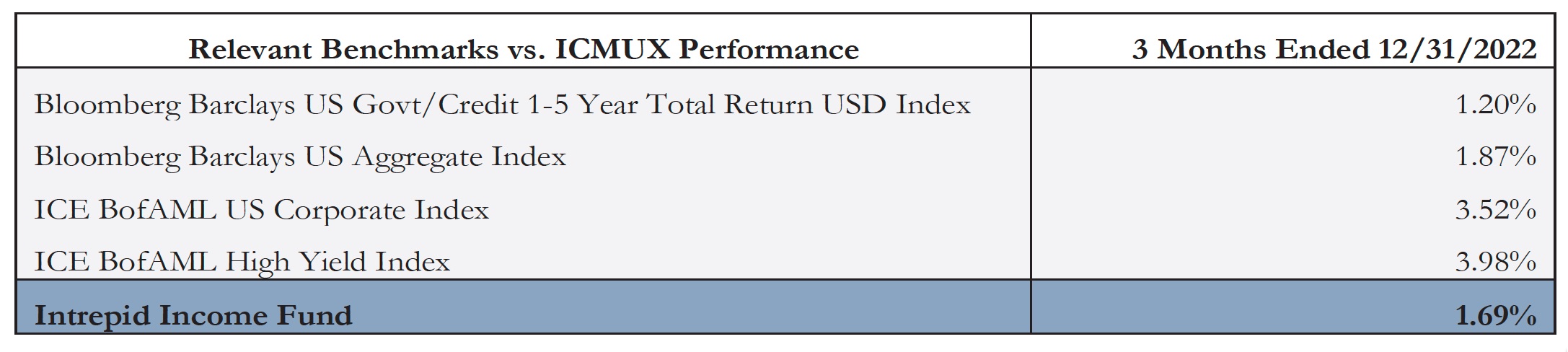

Shifting to performance, the Fund returned 1.69% in the fourth quarter. The High Yield Index increased 3.98% over the same period. The Bloomberg Barclays U.S. Gov/Credit 1-5Y TR Index gained 1.20% and the Bloomberg Barclays US Aggregate Bond Index gained 1.87% during the quarter.

The Fund’s top contributors for the quarter were Atento 8.0% 1st Lien Notes due 2/10/2026, W&T Offshore 9.75% 2nd Lien Notes due 11/01/2023, and Linkem Floating-Rate 1st Lien Notes due 2/9/2023.

The Fund’s top detractors during the quarter were Lightning Motors 7.5% Unsecured Convertible Notes due 5/15/2024, Trulieve 8.0% Secured Notes due 10/06/2026, and Ayr Wellness 12.5% Secured notes due 12/10/2024.

We had six positions that were either called, matured, or sold during the quarter. We added eight new issuers to the portfolio and rolled into three new securities from existing issuers. As always, we encourage investors to reach out for additional commentary on our positions and/or strategy.

Despite the pain we that may lie ahead for risk markets, we are excited by some of the compelling opportunities we are unearthing in credit markets. We will continue to judiciously deploy capital as things come our way. The yield-to-worst for the Fund at the end of the calendar year was 11.11%.

Thank you for your investment.

Sincerely,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Hunter Hayes

Intrepid Income Fund Co-Portfolio Manager