July 1, 2023

“After a certain high level of technical skill is achieved, science and art tend to coalesce in esthetics, plasticity, and form. The greatest scientists are always artists as well”

~ Albert Einstein

Dear Fellow Shareholders,

Dear Fellow Shareholders,

I recently learned that certain metal objects, even after being significantly distorted, will revert to their original shape once heat is applied. These objects are usually composed of a shape-memory alloy, which is also referred to as “smart metal.” If you don’t believe me, you can look up videos on YouTube of unrecognizable paperclips returning back to their original shapes over hot stovetops.

At Intrepid, we think the market is composed of smart metal, too. Even after periods of significant distortion, once enough heat is applied, securities bend back towards their intrinsic values. Some security prices have been distorted for so long, we believe that market participants have been hypnotized into forgetting what their true shapes even look like. Central banks have enabled this hypnosis through a combination of money printing and artificially low rates.

As we wrote in our commentary this time last year, we believe that the value of a security is the present value of its future cash flows. The heat from higher rates and quantitative tightening is finally starting to bring sanity back to valuations and bend things into place. In the fixed income world, which tends to fancy itself a “relative value” asset class, this has been felt, quite viscerally, by so-called core bond investors who were cajoled into reaching for yield by extending duration. This strategy worked phenomenally well from the early 1980s until a couple of years ago, with rates declining steadily for decades. However, we believe that blindly reaching for high-quality duration will not necessarily be a winning strategy for the next few years.

There has been a paradigm shift. Credit picking matters again, and we believe the Federal Reserve may be forced into letting creative destruction run its course to avoid runaway inflation and maintain credibility. Although this may lead to nice relief rallies for longer-duration debt, we are skeptical that there will be anything like the rallies of the previous few decades.

In this environment, we think there is a tremendous opportunity for fixed income investors to earn equity-like returns without equity-like risk. We believe that value will continue to shift from equity-accretive activities to debt servicing as interest costs continue to stay high. And we believe that by keeping duration limited, and not reaching for yield by taking on heaps of credit risk, fixed income investors can maintain optionality and nimbleness for a variety of scenarios. In short, we feel like we can have our cake and eat it, too, by continuing to focus on creditworthy, short-duration bonds and loans.

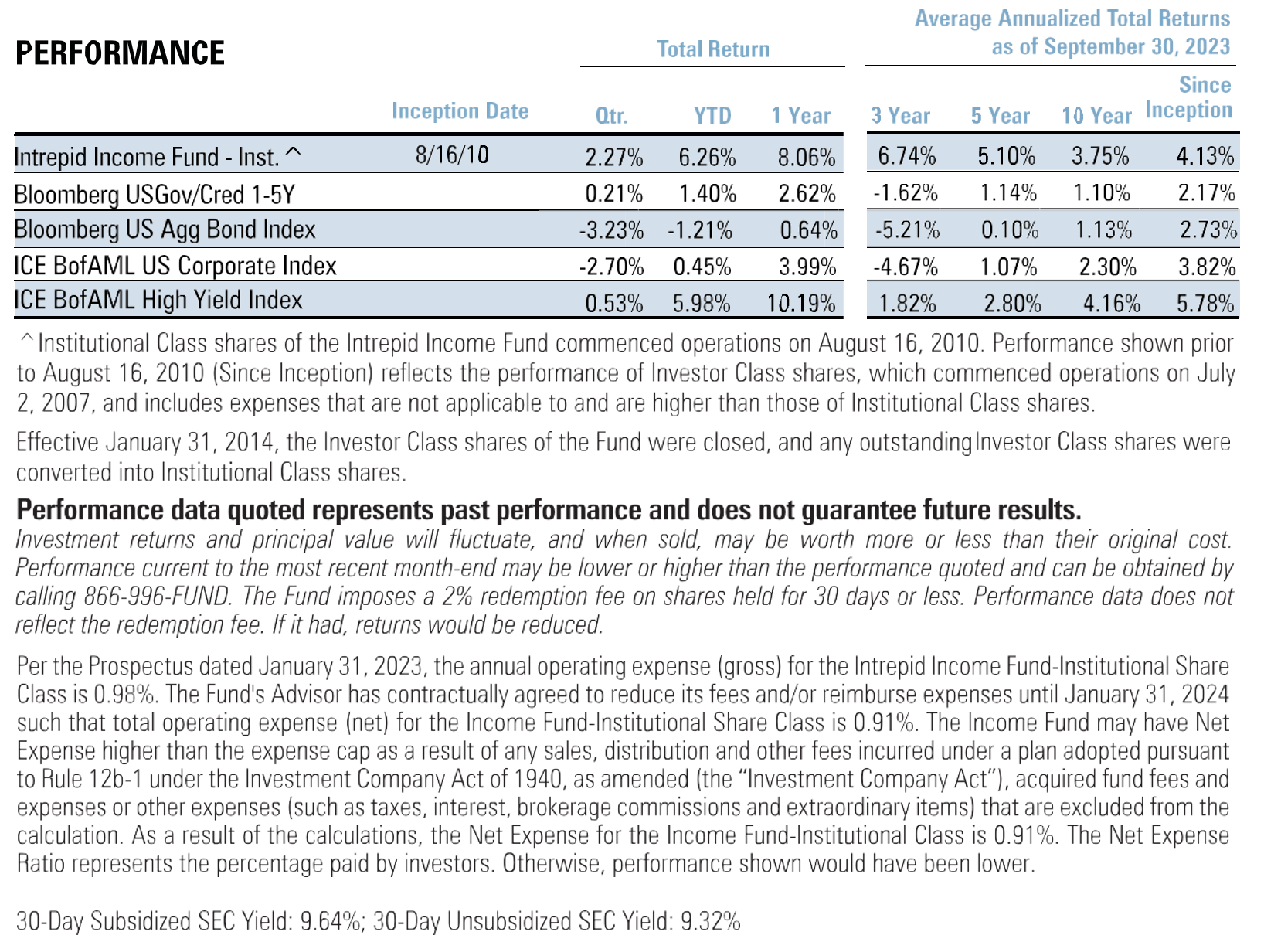

Shifting to performance, the Intrepid Income Fund (the “Fund”) returned 2.27% for the quarter ended September 30, 2023. Our primary focus remains on deploying capital in a disciplined way during these uncertain times in the economy and capital markets.

Fixed income indices continued to diverge. The duration-heavy Bloomberg US Aggregate Bond Index took more lumps, returning -3.23% for the quarter ended September 30, 2023 on the back of higher interest rates. Similarly, the ICE BofAML US Corporate Index (the “Corporate Index”) returned -2.70% over the same period. Riskier debt rallied, somewhat meagerly against the strain of higher rates, with the ICE BofAML High Yield Index (the “HY Index”) returning 0.53% during the period. Similarly, the shorter-duration Bloomberg US Govt/Credit 1-5 Year Total Return USD Index (the “1-5 Year TR Index”) insulated itself from losses, returning 0.21% during the quarter.

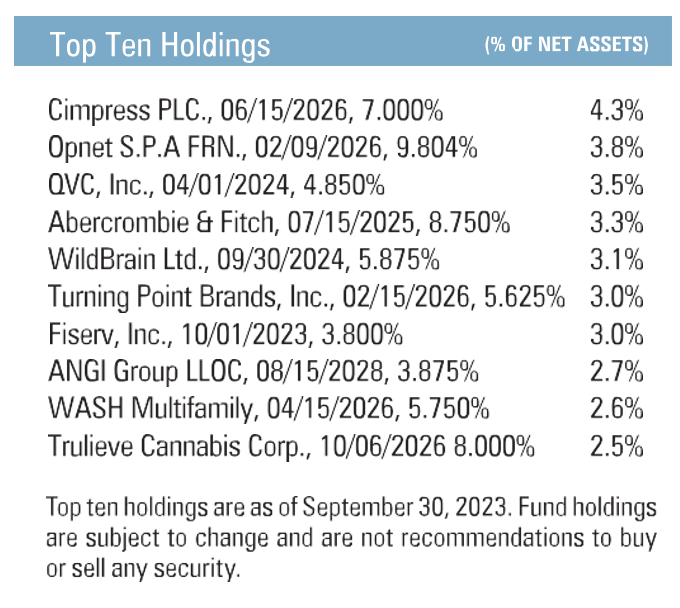

The Fund’s relative success during the third calendar quarter was attributable to idiosyncratic security performance and our short duration focus. As always, we welcome outreach and would love the opportunity to discuss our newest positions with you.

Despite the heat this market has faced, we remain excited about the abundant opportunities we see across the fixed income landscape today. We have no idea where the bottom may lie for risk assets, but we continue to evaluate capital deployment opportunities as objectively as we can, with a focus on ensuring we can remain nimble. Given our short duration profile, we will continue to recycle the proceeds from maturing and/or called bonds into what we think will be increasingly attractive opportunities.

At the end of the third quarter, the portfolio had a yield-to-worst of 11.03% and a modified duration of 2.1 years.

Thank you for your investment.

Sincerely,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Hunter Hayes

Intrepid Income Fund Co-Portfolio Manager