October 1, 2022

“The intrinsic value of an asset is determined by the cash flows you expect that asset to generate over its life and how uncertain you feel about these cash flows.”

~ Aswath Damodaran, The Little Book of Valuation

Dear Fellow Shareholders,

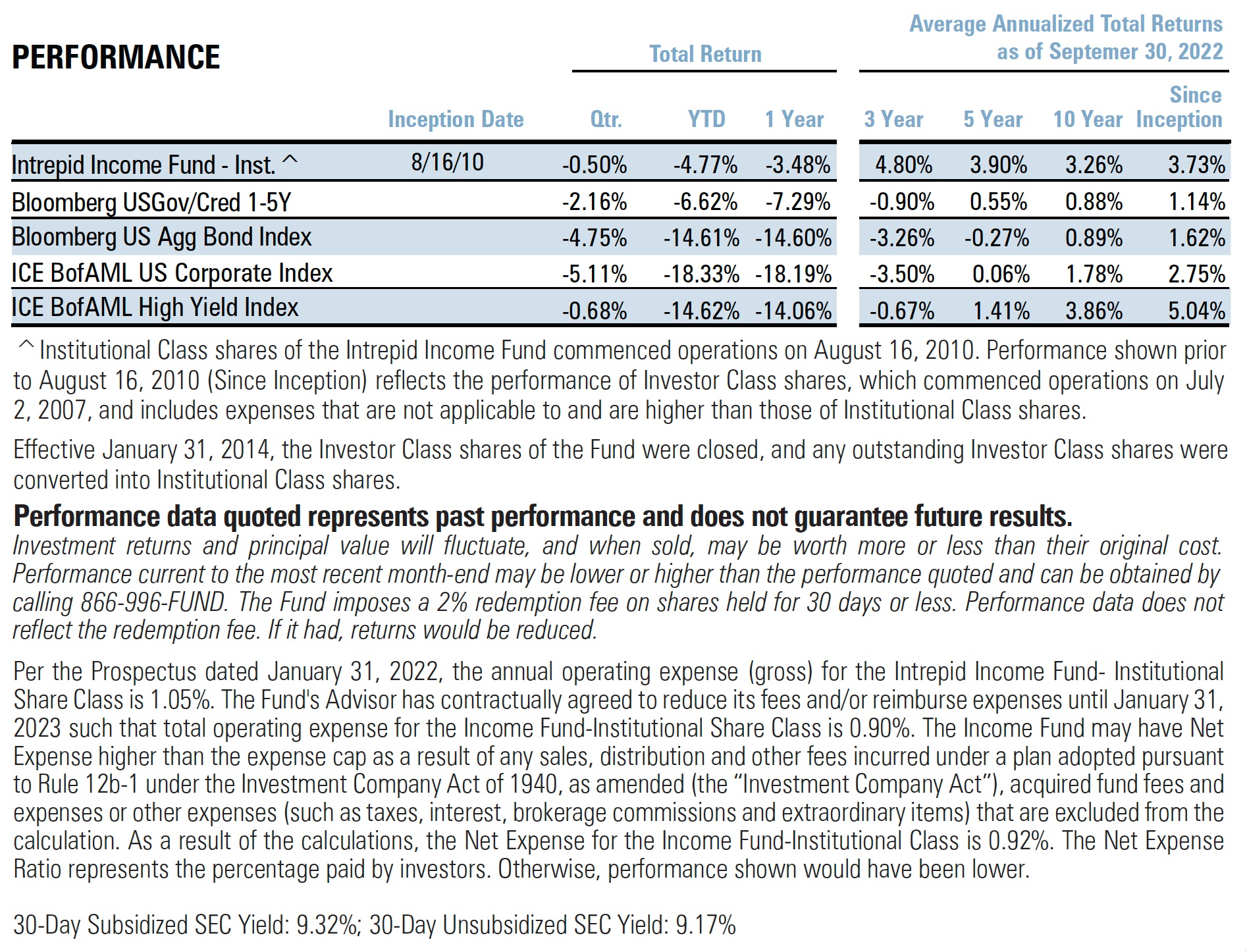

The Intrepid Income Fund (the “Fund”) returned -0.50% for the quarter ended September 30, 2022. Our primary focus remains on deploying capital in a disciplined way during these perilous times in the capital markets.

Fixed income indices continued to suffer. The duration-heavy Bloomberg Barclays US Aggregate Index (the “Barclays Aggregate Index”) took its lumps, returning -4.75% for the quarter ended September 30, 2021 on the back of higher interest rates. Similarly, the ICE BofAML US Corporate Index (the “Corporate Index”) returned -5.11% over the same period. Riskier debt attempted to rally during the quarter, but the ICE BofAML High Yield Index (the “HY Index”) could not quite gather enough steam, returning -0.68% during the period. Not even the shorter-duration Bloomberg Barclays US Govt/Credit 1-5 Year Total Return USD Index (the “1-5 Year TR Index”) was insulated from more pain, returning -2.16% during the quarter.

The Fund’s relative success during the third calendar quarter was attributable to idiosyncratic security performance and our short duration focus. Our top contributors for the three months ended 9/30/2022 included:

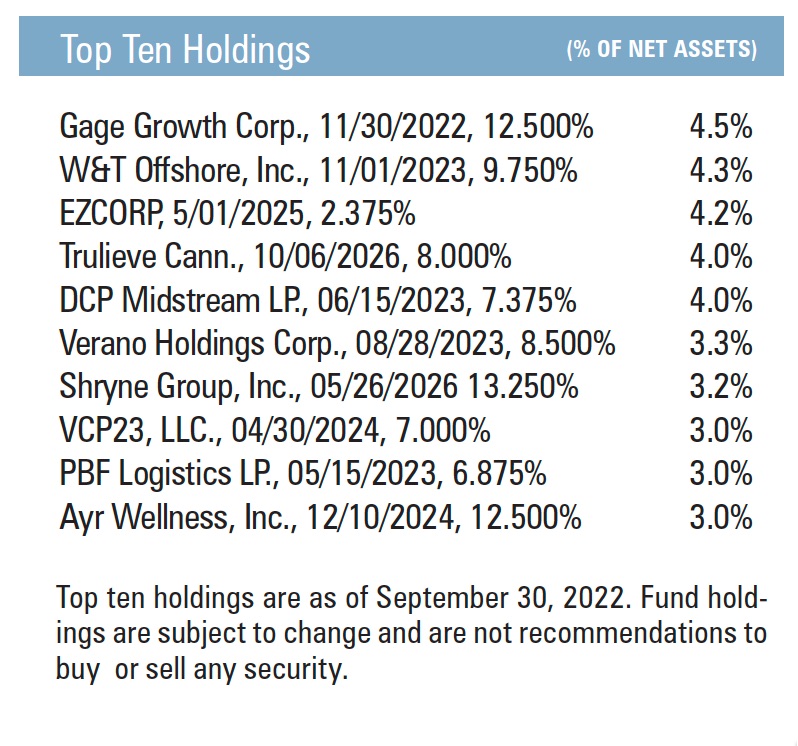

- Battle Motors 6.5% Convertible Note due 11/24/2024 – Battle Motors is a commercial vehicle manufacturer

focused on leading the electrification of trucking fleets. We lent the company money late last year so they could continue building out their Ohio-based facility and fulfill their large customer backlog. We felt like the company’s Convertible Note was well covered by its legacy diesel operations and that there was considerable upside if they could execute on their vision of being an electric vehicle manufacturer. The company opened another round of funding several months ago which offered us the chance to invest more money, or to sell down our position. The company had already performed well enough to earn a higher valuation, and we decided to opportunistically exit. We sold our notes in August at 117 cents on the dollar, which equated to a total annualized return of 28.2%. We will continue to follow the company and we hope to have the opportunity to partner with them in the future.

focused on leading the electrification of trucking fleets. We lent the company money late last year so they could continue building out their Ohio-based facility and fulfill their large customer backlog. We felt like the company’s Convertible Note was well covered by its legacy diesel operations and that there was considerable upside if they could execute on their vision of being an electric vehicle manufacturer. The company opened another round of funding several months ago which offered us the chance to invest more money, or to sell down our position. The company had already performed well enough to earn a higher valuation, and we decided to opportunistically exit. We sold our notes in August at 117 cents on the dollar, which equated to a total annualized return of 28.2%. We will continue to follow the company and we hope to have the opportunity to partner with them in the future. - DCPMidstream 7.375% Perpetual Notes – DCPMidstream is an investment-grade natural gas processing company based out of Colorado. The company has benefited mightily from the strong commodity environment and is on track to generate nearly one third of its debt in free cash flow this year. We started purchasing its perpetual notes over the summer because of a unique “fixed-to-floating” feature which we think incentivizes the company to pay down these notes. Given the rising rate environment, the company’s coupon would likely move from 7.375% to nearly 10% in December, which would make it the company’s most expensive debt by a large margin.Further bolstering our view that these perpetual notes will be paid down at par in December, Phillips 66 announced its intent to acquire DCP Midstream which could trigger a change of control on the company’s various debt securities. Following that announcement, the Perpetual Notes traded up several points and are now marked just below par –the level we believe they will be taken out at in December.

- Exterran 8.125% Notes due 5/01/2025 – Exterran is an energy services company that, at quarter end, was in the process of being acquired by There was skepticism by the market around the company’s ability to close on the transaction, which offered a compelling entry point for the bonds in the mid-90s. The bonds were successfully called at 102.03 after quarter end.

Our top detractors for the three-month period ended 9/30/2022 were:

- Atento 8.0% Notes due 2/10/2026 – Atento is a customer relationship management and business process outsourcing company based in Brazil. The company has had a rough last year and has suffered through a cyber-attack, tough conditions in Latin America, and a horrendous currency hedge. However, we believe the company is about to turn a corner and offers a stable revenue base with robust cash generation that can service the debt. We will continue to monitor this situation closely.

- Cimpress 7.0% Notes due 6/15/2026 – Cimpress provides printing and digital marketing services. Although the legacy print business is under some pressure, other parts of the business are growing handily and should keep the top-line growing. Despite a large debt load, we believe that the company should generate enough free cash flow to de-lever over the next few Despite our optimistic view, the bonds have languished since our first purchase, and we have continued to acquire more.

- Rackspace 5.375% Notes due 12/01/2028 – Rackspace is an information technology company. It turns out that not just technology stocks have gotten walloped this year. Despite the bonds being down significantly, we believe the company will continue to generate cash flow and improve the balance sheet. Given the company’s far dated maturity wall and low cost of capital, we plan to continue acquiring a position through this sell-off.

The Income Fund had two corporate bond positions that were called or matured in the third calendar quarter. We also sold out of four positions that we believe offered less compelling value relative to other positions.

The proceeds from the bonds that were called, sold, or matured were redeployed into a mixture of existing positions and new positions, including:

- Abercrombie & Fitch 8.75% Notes due 7/15/2025 – Abercrombie & Fitch is an apparel products company that also owns Hollister. Despite having lost the insane degree of popularity that the brand once boasted, we believe the company is poised to grow in the low single digits over the next few years as it attempts to reinvigorate its brands. Most critically, these notes are secured and the only debt in the capital stack. The company also has net cash and an undrawn revolving credit facility.

- Valvoline 4.25% Notes due 2/15/2030 – Valvoline manufactures and distributes automotive lubricant and It is a fantastic business with exceptional returns on invested capital and historical growth. In August, Aramco agreed to purchase Valvoline’s petroleum unit, the proceeds of which would go to pay down these notes at par. We have been acquiring a position in the mid-90s and will look to add more if the deal were to fall apart for some reason.

- W&T 9.75% Notes due 11/01/2023 – W&T Offshore is an independent oil and natural gas producer in the Gulf of Mexico. The favorable commodity environment has resulted in a gusher of free cash flow for the company, which has significantly de-leveraged its balance sheet. These 2nd lien notes will be taken out at par some time before maturity as the company waits for the right opportunity to tap the capital markets. In the event that the debt window is closed, the company should have enough cash and credit capacity to pay down the notes organically.

- IEA 6.625% Notes due 8/15/2029 – IEA Energy Services is an infrastructure construction company that specializes in renewable energy projects. We started acquiring these notes after it was announced that MasTec, an investment grade issuer, would be acquiring IEA. That transaction recently closed, which resulted in these notes being upgraded to investment grade by the major rating agencies. Despite the duration of these notes, we like the long-term trajectory of this company and believe we are being compensated handsomely for a relatively robust credit.

- Brinker 5.0% Notes due 10/01/2024 – Brinker operates casual dining restaurants, including Chili’s Grill & Bar and Maggiano’s Little Italy restaurant If you know the Intrepid team at all, you know that Chili’s is our favorite spot for a night out. We are investing in what we know with this well-run company, which has continued to grow through this tough macro environment and should be able to comfortably refinance its upcoming debt maturities.

Despite the tough conditions in the market, we remain excited about the abundant opportunities we see across the fixed income landscape today. We have no idea where the bottom may lie for risk assets, but we continue to evaluate capital deployment opportunities as objectively as we can, with a focus on ensuring we can remain nimble. Given our short duration profile, we will continue to recycle the proceeds from maturing and/or called bonds into what we view as increasingly attractive opportunities.

At the end of the third quarter, the portfolio had a yield-to-worst of 11.37% and an effective duration of 2.0 years.

Thank you for your investment.

Sincerely,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Hunter Hayes

Intrepid Income Fund Co-Portfolio Manager