July 1, 2023

Dear Fellow Shareholders,

The second calendar quarter of 2023 ended with a sanguine tone, leaving the memory of March’s banking crisis and May’s debt ceiling standoff as distant memories. Treasury yields continued to float higher, and volatility across the entire fixed-income landscape ended the quarter close to the lows for the year. Most fixed-income investors seem content to “wait and see” how the higher interest-rate experiment pans out while enjoying the spoils of the highest cash yields in recent history.

During the second quarter, we witnessed the furious reemergence of the “reach for yield” trend with investors quite willing to embrace credit risk. As spreads continued to tighten during the quarter, the CCC tranche saw the most tightening, with the riskiest tier of performing junk bonds coming in by a massive 129 basis points in June alone. Does this mean that fixed-income investors believe we are headed for a soft landing? Undoubtedly some do, although, at Intrepid, we remain extremely skeptical that the effects from higher yields have truly been felt by the broader economy yet.

We continue to view short-dated, higher-quality credit as a ballast for the portfolio that will allow us to continue redeploying capital into a choppy, but attractive high-yield bond environment. We continue to look for robust, core credit positions issued by companies that we believe have the liquidity and cash flow profile to weather a recession and/or absorb the impact of higher rates.

The past few quarters, we have written about how this is a credit picker’s market, and that lenders will be rewarded or exposed based on the caliber of their credit work. We continue to believe that there are plenty of attractive credits out there, but shrewd and patient underwriting is the key to not losing one’s shirt in this environment.

During the quarter, the Intrepid Income Fund (the “Fund”) decreased its effective duration and increased its yield-to-worst as compared to the end of the first calendar quarter of 2023. We will be the first to admit that we have no superior knowledge of the trajectory of interest rates. We are instead focused on doing sound, fundamental analysis for which we believe we are getting more than adequate return per unit of risk.

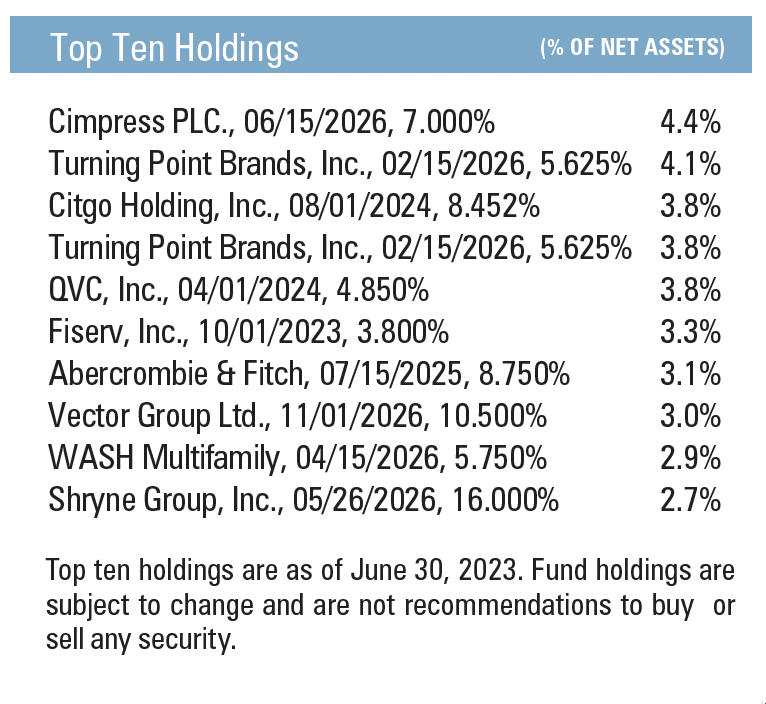

We have been acutely focused this year on increasing the credit quality of the Fund by lending to higher quality issuers and/or through instruments with robust security. At the end of the second calendar quarter, 20.5% of the Fund was in investment-grade bonds and 57.1% was in secured bonds or loans.

Although we are still open to lending on an unsecured basis, the hurdle to deploying capital to companies without security has been raised much higher. To that end, the Fund’s allocation to convertible bonds, which tend to have loose covenants, dropped to just 2.2% at the end of the quarter. Accordingly, the Fund’s allocation to loans, which tend to have much tighter covenants, ended the quarter at 15.3%. We will continue to be opportunistic about how we allocate across these sleeves.

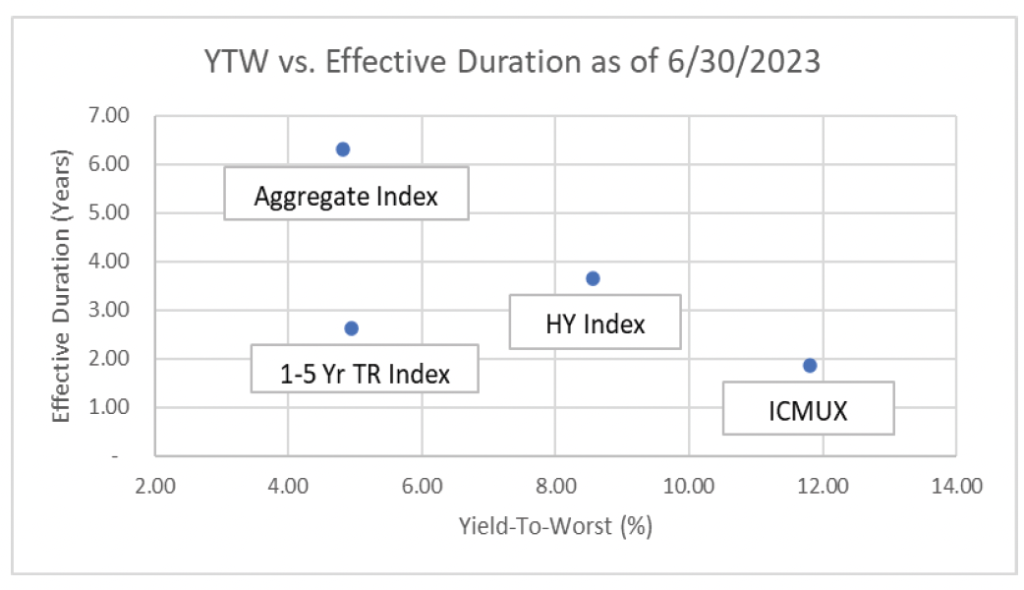

As the chart shows, we continue to limit our interest-rate risk, as measured by the Income Fund’s effective duration, especially relative to the indices. In this dislocated credit market, we also continue to find double-digit yielding credits with favorable return per unit of risk, in our view. All things equal, we would expect the Fund’s yield-to-worst to come down over the next few quarters as our higher-yielding positions begin to mature.

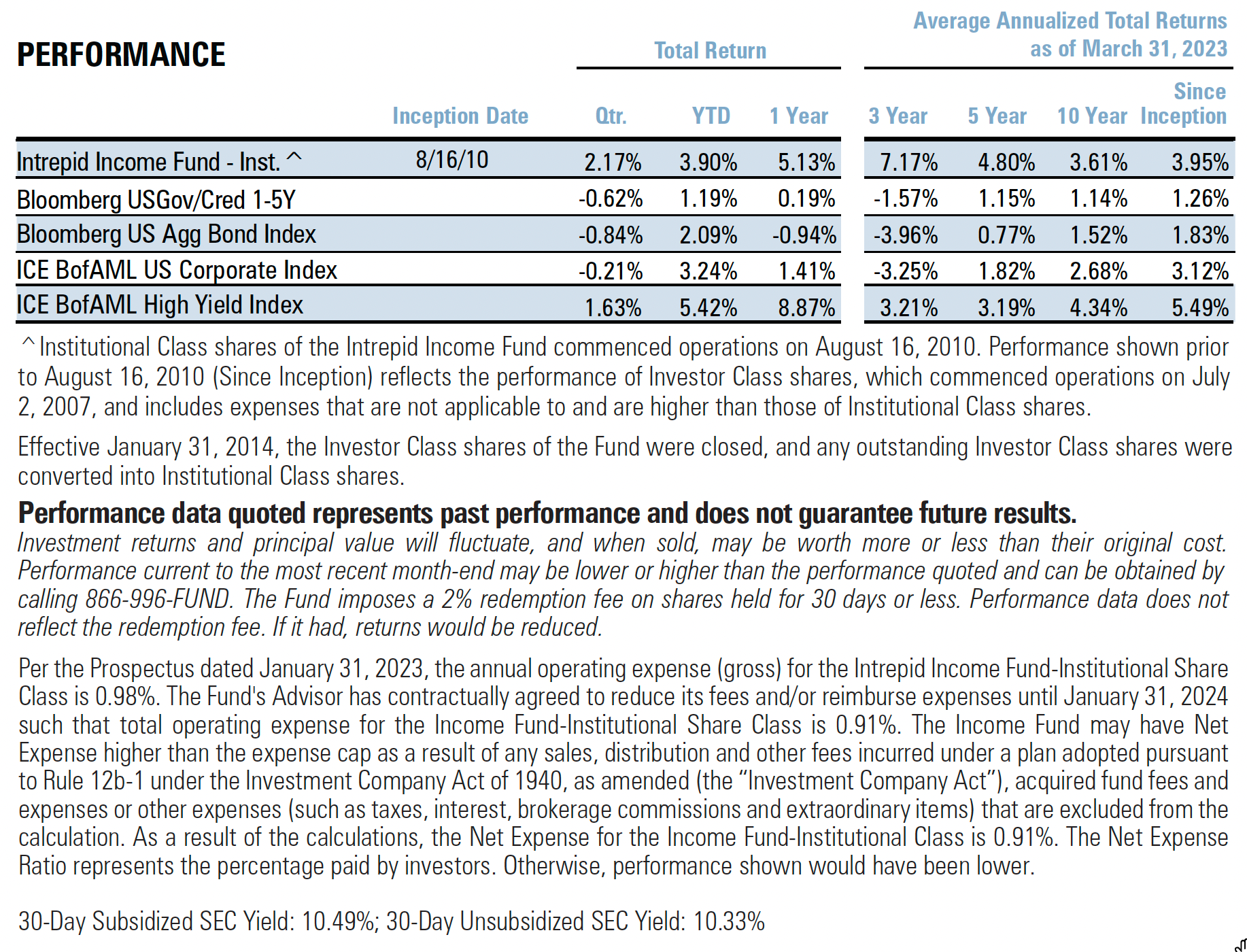

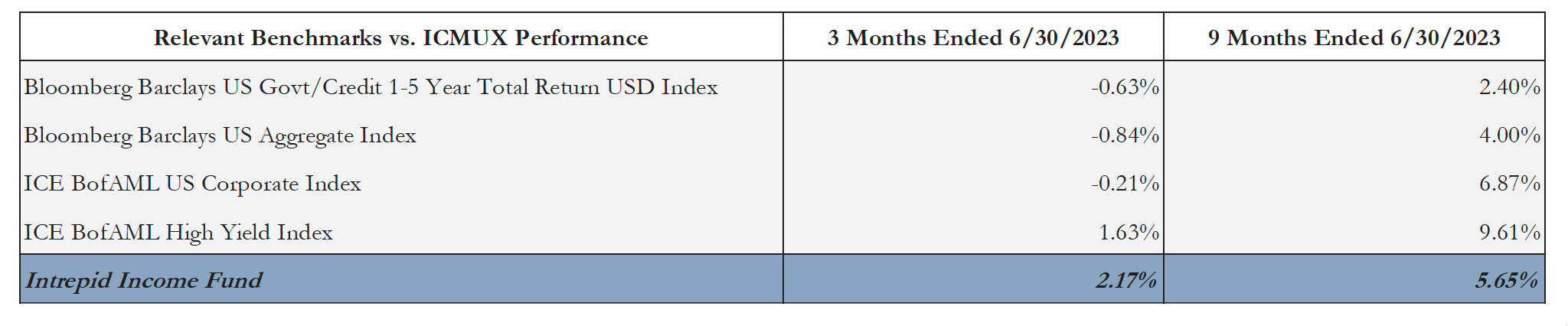

Shifting to performance, the Fund returned 2.17% in the second calendar quarter of 2023. The High Yield Index increased 1.63% over the same period. The Bloomberg Barclays U.S. Gov/Credit 1-5Y TR Index returned -0.62% and the Bloomberg Barclays US Aggregate Bond Index returned -0.84% during the quarter. The US Corporate Index saw a -0.21% return for the same period.

The Fund returned 5.65% for the nine-month period ended June 30, 2023. The High Yield Index increased 9.61% over the same period. The Bloomberg Barclays U.S. Gov/Credit 1-5Y TR Index returned 2.40% and the Bloomberg Barclays US Aggregate Bond Index returned 4.00% during the nine-month period ended June 30, 2023. Lastly, the US Corporate Index was up 6.87% across the same nine-month period.

As always, we encourage investors to reach out for additional commentary on our positioning and strategy.

We remain sanguine about the prospects for short-duration high yield despite the turbulence that may lie ahead for risk markets. Careful credit analysis will be the differentiator. The yield-to-worst for the Fund at the end of the first calendar quarter was 11.81% with a modified duration of 1.87 years.

Thank you for your investment.

Sincerely,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Hunter Hayes

Intrepid Income Fund Co-Portfolio Manager