July 1, 2022

“Saw the hands that build / Can also pull down”

~ U2, Lyrics to Exit from The Joshua Tree (1987)

Dear Fellow Shareholders,

Life thrives in unexpected places. Across the world, flora and fauna have found a way to survive in many extreme environments, from towering mountains to deep caves. But no hostile ecosystem surprises me more for its abundance of life than the desert.

I recently visited Joshua Tree, California, which is nestled between the Sonoran and Mojave Deserts. It was an amazing trip full of hiking and stargazing. The landscape is an enchanting mixture of beauty and grotesquery, like a Dr. Suess story set on Mars.

Joshua Tree houses a surprising range of desert plants and animals. Despite the unforgiving conditions, there exist over 50 species of mammals, 40 species of reptiles, and 700 species of plants that call it home. But the most distinctive, ubiquitous resident of this area is the eponymous Joshua Tree, a tortured inhabitant of the desert that Mormon travelers believed was a sign from the prophet Joshua back in the 19th century.

I could not help but be reminded of today’s market when looking out across the bleak landscape captured in the pictures I took at Joshua Tree National Park. Even though blistering heat (economic pressures), a lack of liquid (liquidity), and stifling dryness (pessimism) make the environment quite harsh, specimens like the stubborn Joshua Tree somehow manage to thrive.

We are looking to lend to companies that resemble the Joshua Tree. These are the type of companies that can grow and prosper, even in an economic desert. They do not have to be the flashiest companies or operate in the sexiest lines of business, but they must possess the grit to survive. Despite the tough market conditions, we believe these companies exist and we continue to look for opportunities to lend to them.

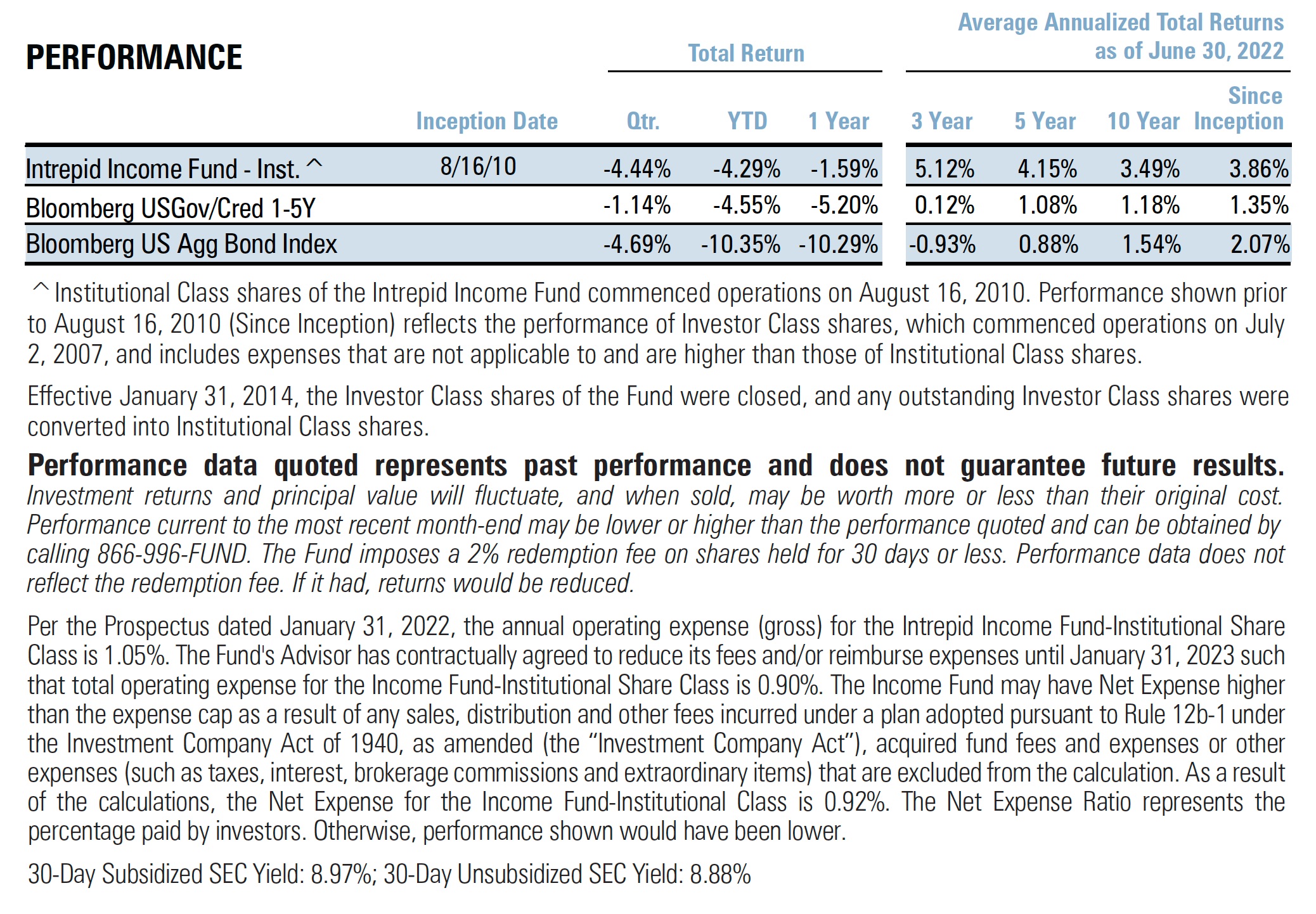

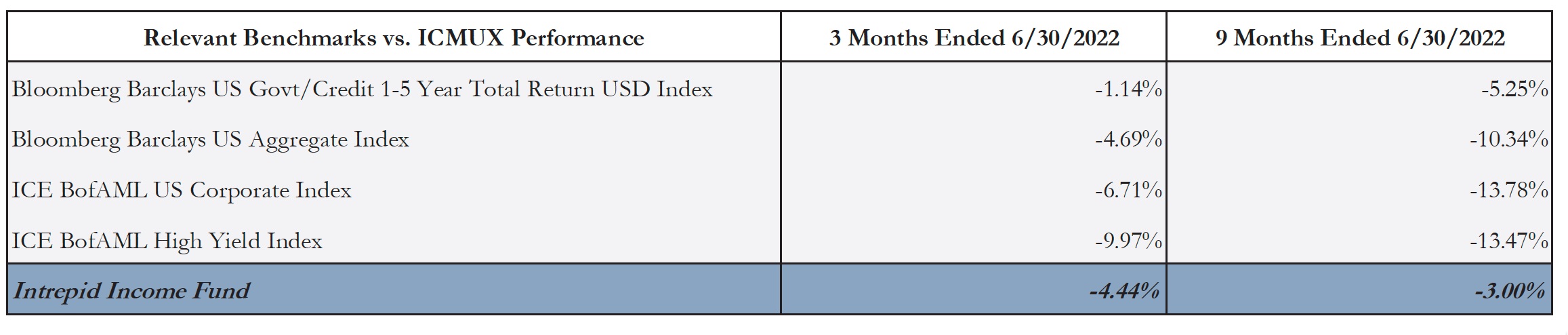

The Intrepid Income Fund (the “Fund”) returned -4.44% for the quarter ended June 30, 2022. General fixed income performance for the second quarter of the year was abysmal. Rates zoomed higher, with the 10-Year Treasury ending the quarter yielding 3.01%, 68 basis points above the end of last quarter. This translated into historically poor performance for the duration-heavy Bloomberg Barclays US Aggregate Index (the “Barclays Aggregate Index”), which returned -4.69% for the quarter ended June 30, 2022. Similarly, the ICE BofAML US Corporate Index (the “Corporate Index”) lost -6.71% over the same period. Riskier debt fared even worse on the back of wider spreads, with the ICE BofAML High Yield Index (the “HY Index”) returning -9.97% in the quarter. The shorter-duration Bloomberg Barclays US Govt/Credit 1-5 Year Total Return USD Index (the “1-5 Year TR Index”) returned -1.14% over the same period.

Although the Fund enjoyed favorable relative performance during the second calendar quarter, we were not immune from the tough market conditions. Our negative return was primarily attributable to general market weakness, although idiosyncratic security performance also contributed.

We continue to believe in the creditworthiness of our portfolio despite these challenging conditions and were able to redeploy capital from securities that matured, were called, or were sold during the quarter at much more attractive yields. The yield-to-worst on the portfolio at quarter-end was 11.79% and the effective duration was 2.14 years.

As the chart below reflects, we continue to seek out high yielding securities with a relatively short effective duration, which we believe should partially insulate us from the volatility in interest rates.

Our top contributors for the three months ended 6/30/2022 included:

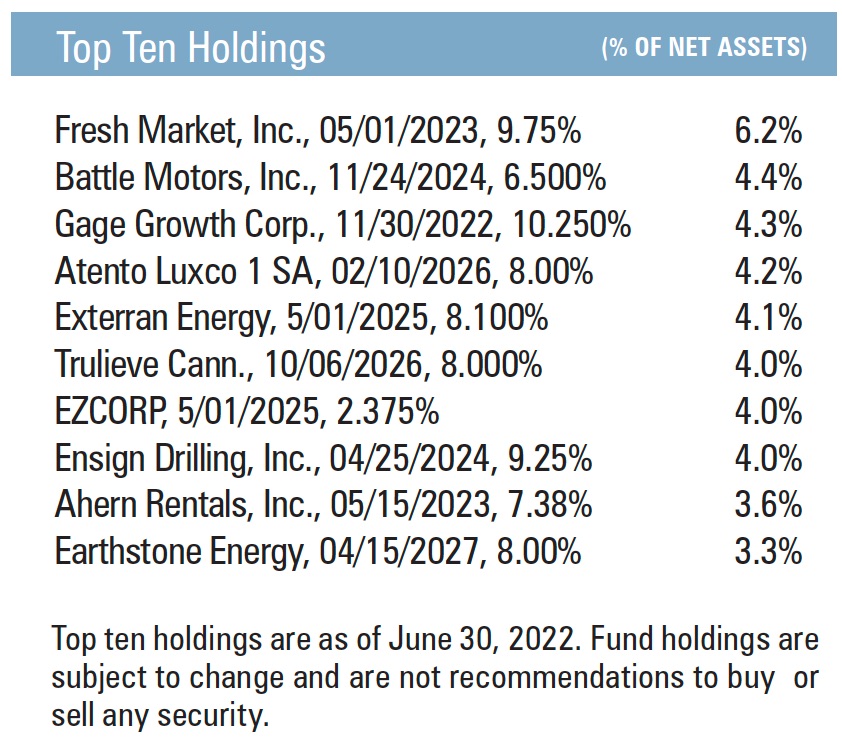

- Gage Growth Corporation Senior Secured Loan due 11/30/2022 – Gage is a Michigan-based cannabis operator that was acquired by Terrascend Corporation in an all-stock deal earlier this year. This loan enjoys a floating-rate feature that kicked in over the last few months as interest rates moved higher. Combined with an already generous double-digit coupon, robust collateral coverage, and a solid underlying management team at Terrascend, we continue to like this credit and will likely hold on until maturity.

- GRTWST 12.0% Senior Unsecured Notes due 09/01/2025 – We have written about these notes at length in previous commentaries. In May, PDC Energy completed its acquisition of Great Western and these notes were called at a dollar price of 113.192. As a reminder, we originally received a 2.5-point original issue discount for this deal, making our total return over the life of the security well over 20%.

- TFM 9.75% 1st Lien Notes due 05/01/2023 – The Fresh Market was a new position for us that we started nibbling on in the mid-90s dollar price during the quarter. In early May, the specialty grocer announced they were being purchased by a South American company called Cencosud. As part of the transaction, our notes were called at par right after the quarter ended.

Our top detractors for the three-month period ended 6/30/2022 were as follows:

- ATENTO 8.0% 1st Lien Notes due 02/10/2026 – We own Atento across the capital structure at Intrepid Capital and have written about our thesis in previous commentaries. We believe these 1st lien notes are well covered in a downside scenario, but that a lack of liquidity and an aversion to Latin American credit exposure unjustly punished this credit during the quarter. We believe that the company’s 2nd quarter results will be pivotal in understanding its trajectory and we will be looking for updates on the strategic plan, which may include a sale.

- RAX 5.375% Unsecured Notes due 12/01/2028 – After a poor showing in the first quarter, Rackspace’s unsecured notes continued to trend lower on the back of higher interest rates and a sudden market aversion to technology companies. We continue to be baffled by where the notes trade (they now yield nearly 13%) given that this company has had decent earnings, generates recurring cash flow, has a long runway until any debt maturities, and is continuing to grow quickly. We believe that as liquidity returns to the high yield market, these notes will pop back quickly, and we have opportunistically added to our position.

- AHERN 7.375% 2nd Lien Notes due 05/15/2023 – Ahern is a private filer, so we are limited in what we can discuss in this commentary. The equipment rental company has not yet addressed this short-dated maturity, which we believe has put pressure on the dollar price. We encourage those who would like to learn more about this situation to reach out to us.

The Income Fund had two corporate bond positions that were called or matured in the first calendar quarter. We also reduced several positions after they hit our internal yield bogey, selling out of a handful of positions entirely. In a world now awash in yield, we can be much pickier with where we deploy capital.

The proceeds from the bonds that were called, sold, or matured were redeployed into a mixture of existing and new positions. Given how volatile credit markets continue to be, we have employed a gradual, dollar-cost averaging approach when starting new positions.

We do not discuss any specific new positions in this quarter’s commentary, but we are only a phone call or e-mail away for anyone who would like to hear about what we are purchasing and why.

We have also been surprised by how well credit spreads have held up during the sell-off in risk assets year-to-date.  We believe that poor earnings results and continued macro pressures could contribute to widening spreads which would have a pernicious affect on the high yield asset class.

We believe that poor earnings results and continued macro pressures could contribute to widening spreads which would have a pernicious affect on the high yield asset class.

Strong liquidity from buy-the-dip buyers could cause this market to rip higher in the near-term. We anticipate that junk bond money managers will point to the historically high yields one can now get in the market and say this is a good entry point. And although it may be a decent entry point, we are not convinced. We continue to believe that risks are skewed to the downside and that the worst of the pain in junk bonds is yet to come.

Strong liquidity from buy-the-dip buyers could cause this market to rip higher in the near-term. We anticipate that junk bond money managers will point to the historically high yields one can now get in the market and say this is a good entry point. And although it may be a decent entry point, we are not convinced. We continue to believe that risks are skewed to the downside and that the worst of the pain in junk bonds is yet to come.

Although we are proud of how we have relatively protected our investor’s capital given the volatility of the past 6 months, we desire to do better. Our top priority is return of capital followed by return on capital.

Hence, our simple goal during these uncertain times is to protect your capital even at the expense of missing out on some of the inevitable bear market rallies. We believe that there will be a time to take on more risk, but now is not it.

The investment team continues to turn over every desert rock in the pursuit of unique, exceptional credits. Despite the arid market conditions, life thrives in unexpected places.

Thank you for your investment.

Sincerely,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Hunter Hayes

Intrepid Income Fund Co-Portfolio Manager

Past performance is not a guarantee of future results.