April 1, 2023

Dear Fellow Shareholders,

Despite the steady drumbeat of higher rates and fears of a recession, the first three months of 2023 shined favorably upon credit markets. We continue to be reluctantly optimistic about certain pockets of high yield credit, especially on the front-end of the curve, but we are also taking advantage of “three-foot putts” that continue to pop up, specifically in short-dated, investment grade credit.

During March, for instance, when markets became dislocated on the back of a slew of bank failures, many investors unloaded higher-quality positions to prepare for potential redemptions and/or runs on capital. Why unload higher quality positions? Because these positions are often more liquid and usually incur a lower mark-down to liquidate in times of distress. Regardless of the reasons, we were keen to purchase high quality securities at double-digit money market yields as the drama unfolded, and the Intrepid Income Fund (the “Fund”) ended the first calendar quarter of 2023 with 22.1% of the portfolio in investment grade bonds.

We view this short-dated, investment grade sleeve as a ballast for the portfolio that will allow us to continue redeploying capital into a choppy, but attractive, high yield bond environment. We continue to look for robust, core credit positions issued by companies that we believe have the liquidity and cash flow profile to weather a recession and/or absorb the impact of higher rates.

It is interesting to compare this fixed income environment, which we view as attractive on a risk-adjusted basis, to the environment of 18 months ago, which we viewed as extremely unattractive. There is an old saying in credit that there are “no bad bonds, just bad prices” that we think rings true against this backdrop. Although we expect default rates to tick up, and for there to be more carnage as the higher cost of capital permeates its way through the system, we also believe that there are plenty of opportunities out there that compensate one for those risks. In other words, we are fine with the choppier economic environment given the significantly enhanced yield we can receive.

Another encouraging sign for lenders is the pick-up of new issue supply that priced in the first quarter. Despite considerable volatility, $45 billion and $404 billion of new issues were brought to market in the high yield and investment grade markets, respectively, according to CreditSights. These new issues carry significantly better rates and terms for lenders than we have seen in quite some time, and we participated in several deals. Although there continues to be gamesmanship by companies around tapping credit markets, many have recognized that we are in a new paradigm, and taken advantage of the credit window being open. We expect the new issue window to be a source of ideas for us now that things have shifted to more of a lender-friendly market, and we are taking an active role in refinancing discussions with many of our borrowers.

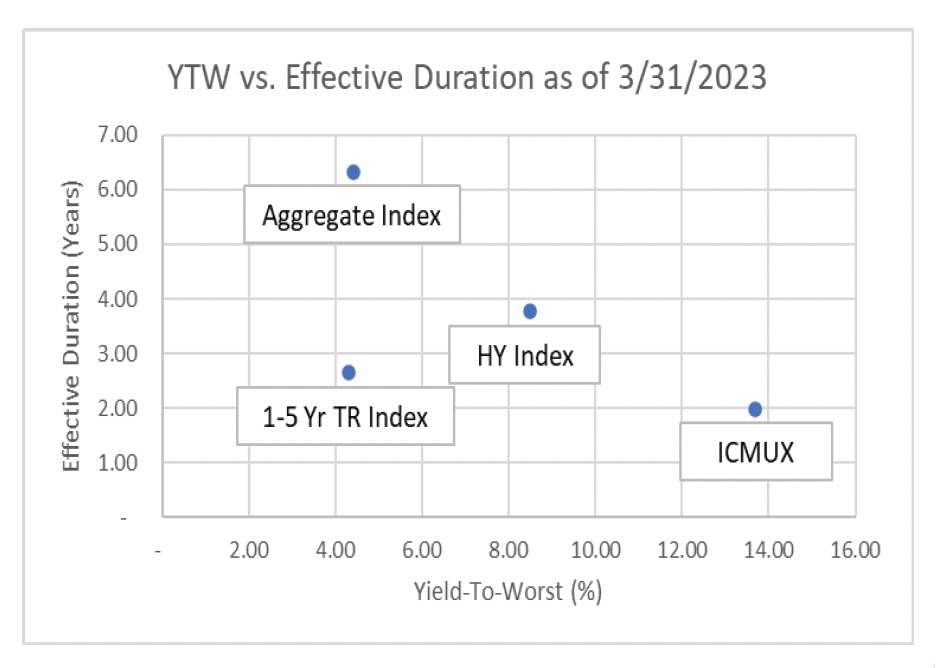

As the chart shows, we have taken advantage of the market dislocations to enhance our yield profile, but we have also kept our duration low relative to indices. We admit that we have no superior insight into the path of interest rates from here, but we do feel good about the credits we are underwriting. We expect our performance to be more volatile than it has been historically given our higher yield profile, and we will continue to deploy capital into this higher yielding environment for as long as the market gives us attractive risk-adjusted opportunities.

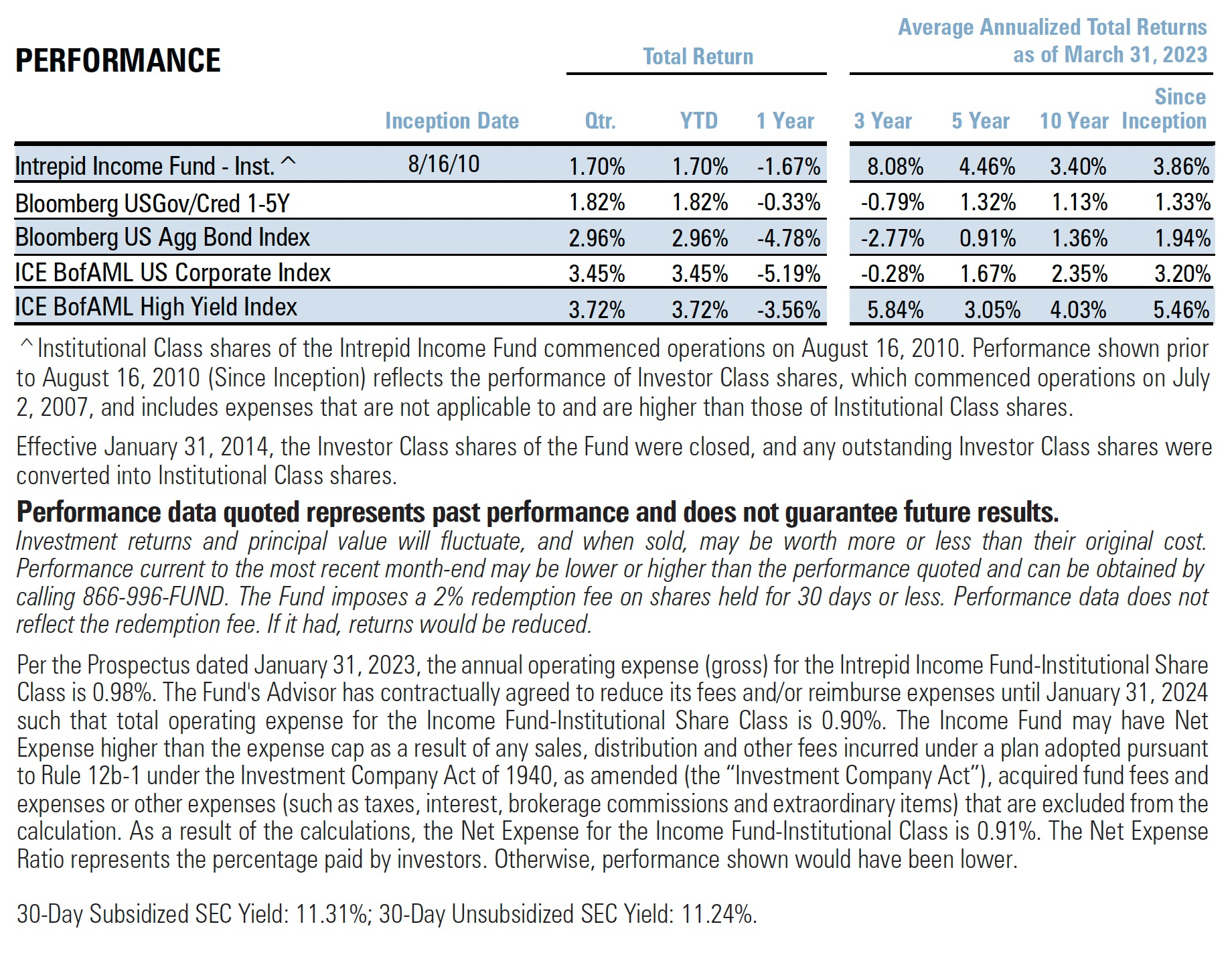

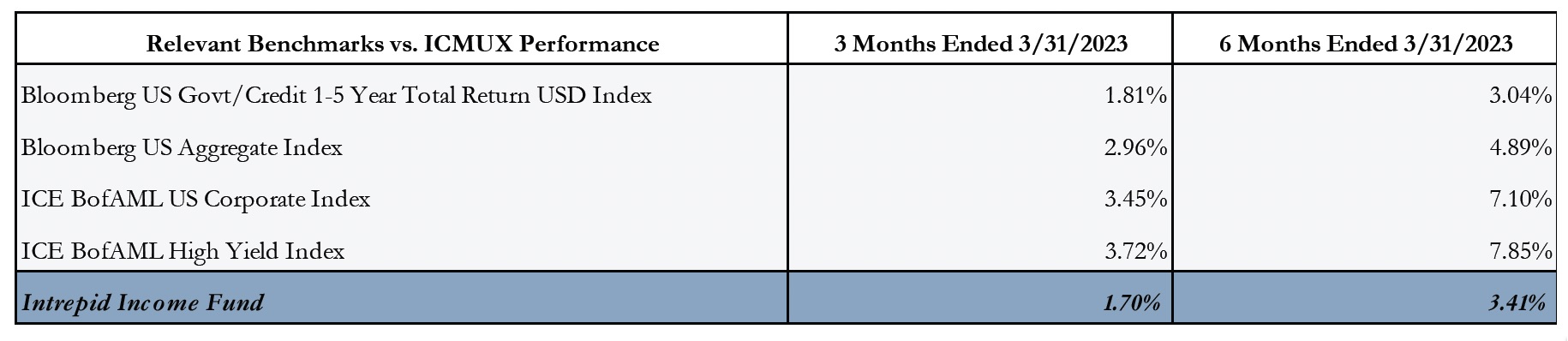

Shifting to performance, the Fund returned 1.70% in the first calendar quarter. The High Yield Index increased 3.72% over the same period. The Bloomberg Barclays U.S. Gov/Credit 1-5Y TR

Index gained 1.82% and the Bloomberg Barclays US Aggregate Bond Index gained 2.96% during the quarter.

This is not to say that we expect smooth sailing from here. Quite the contrary – it is likely that the Federal Reserve will continue raising rates in its quest to quell inflation, possibly leading to a recession. However, we believe that at today’s levels, pockets of fixed income provide a compelling entry point.

The Fund’s top contributors for the quarter were Cimpress 7.0% Unsecured Notes due 6/15/2026, Abercrombie & Fitch 8.75% Secured Notes due 7/15/2025, and Vista Outdoor Inc. 4.5% Unsecured Notes due 3/15/2029.

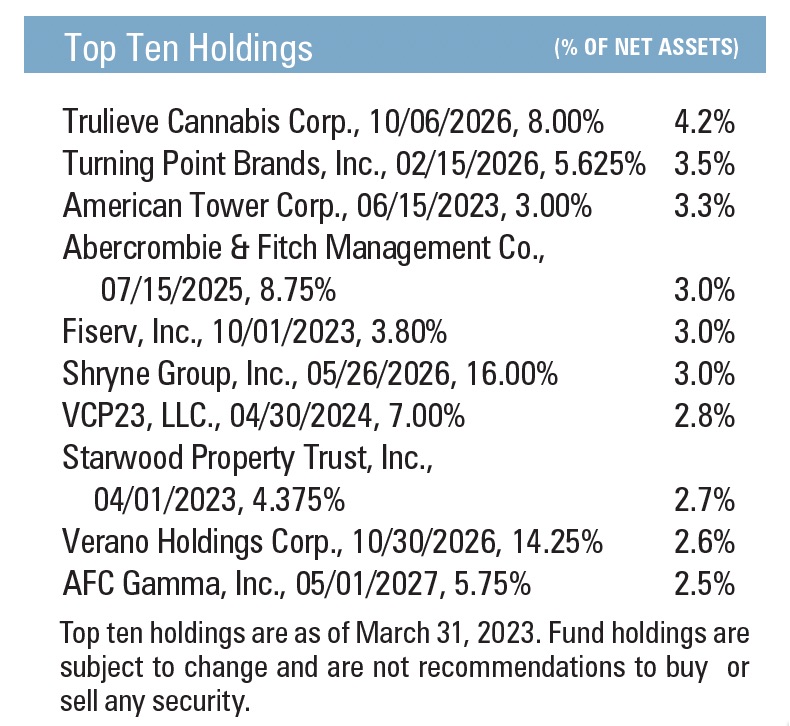

The Fund’s top detractors during the quarter were Atento 8.0% Secured Notes due 2/10/2026, QVCN 4.85% Secured Notes due 4/01/2024, and Trulieve 8.0% Secured Notes due 10/06/2026.

As always, we encourage investors to reach out for additional commentary on our positioning and strategy.

We remain sanguine about the prospects for short duration high yield despite the turbulence that may lie ahead for risk markets. Careful credit analysis will be the differentiator. The yield-to-worst for the Fund at the end of the first calendar quarter was 13.68% with a modified duration of 1.97 years.

Thank you for your investment.

Sincerely,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager

Hunter Hayes

Intrepid Income Fund Co-Portfolio Manager