October 1, 2023

“The first rule of compounding is to never interrupt it unnecessarily.”

-Charlie Munger

Dear Fellow Shareholders,

The quote above is one rule of wisdom from the Buffet/Munger Duo at Berkshire Hathaway that I have tried to implement – both personally and as your Portfolio Manager – knowing that both human emotion as well as Wall Street’s penchant “for a trade” are working against me in that pursuit.

I am currently reading “How to Invest” By David Rubenstein, co-founder of the Carlyle Group.

The book is a compendium of interviews from investors of all stripes. In one interview he is speaking to Mary Erdes, head of private banking at JP Morgan. She notes some market performance (keep in mind the interview was in 2021) that says the balanced mix of stocks and bonds had an average return on 6.5% over the last 30 years, but unfortunately the average investor had only earned less than half of that (~3%). We have seen similar outcomes from Dalbar and Associates which publishes an annual study of investor behavior in the mutual fund business. This is the proverbial “buy high, sell low,” unfortunately!

I feel certain you have seen the ubiquitous Progressive Insurance ads where the instructor is showing classroom attendees how to not be their parents. My personal favorite is when his group is heading into a pro football game. They are in a parking lot, and the collective concern is “how will we remember where we parked” and “when can we leave the game?” I am sure my kids can relate when we attend a Jaguars game together! The collective message is “Don’t Be That Guy/Gal” or in the case of the ad “Don’t be your Parents.” In my case, it’s too late!

The analogy here is don’t let your emotions get the best of you and sell when the current outlook is bleak or fear overcomes you. Easier said than done, I know!

This all comes to mind as we are suffering through some difficult months in the last quarter as the Fed tries to engineer a soft landing and Treasury rates continue to rise in the face of persistent strength in the Consumer Price Index (CPI). The benchmark 10 year Treasury now yields more than 4.50%, which presents a drag on values of stocks and bonds as cash flows to be delivered far into the future are worth less with a higher discount rate. Please keep in mind, to use the Federal Reserve refrain, that “rate increases have a lagging and variable effect on the economy.” Wow, that was insightful!

The good news now for investors is compounding hasn’t been this easy (if it ever really was!) as the Fed engineered increases of a greater-than-5% short term rate, which has brought the bond market with it in terms of currently available yields – many of which we haven’t seen since before the Great Financial Crisis(GFC) of 2008. That being said, there has been tremendous pain for bond investors getting to this point. I sarcastically commented this time 3 years ago that “bond investors are getting return-free risk” as the Fed Reserve Quantitative Easing (QE) brought short term rates to 0.25% and dragged down long term rates as well. To wit: the 1.25% Treasury bonds due May 15, 2050 are quoted at $48.18, less than half of their offer price just over three years ago. That is the risk I was referring to!

Please keep in mind the Intrepid Capital Fund has been devoted to short term corporate bonds since inception of the Fund, with generally a third of the Fund devoted to this asset class. The good news is we are now rewarded as a lender in this part of our portfolio. I refer to this as “an equity surrogate return” as short duration bonds we seek now offer yields similar to long term equity returns (9-11%).

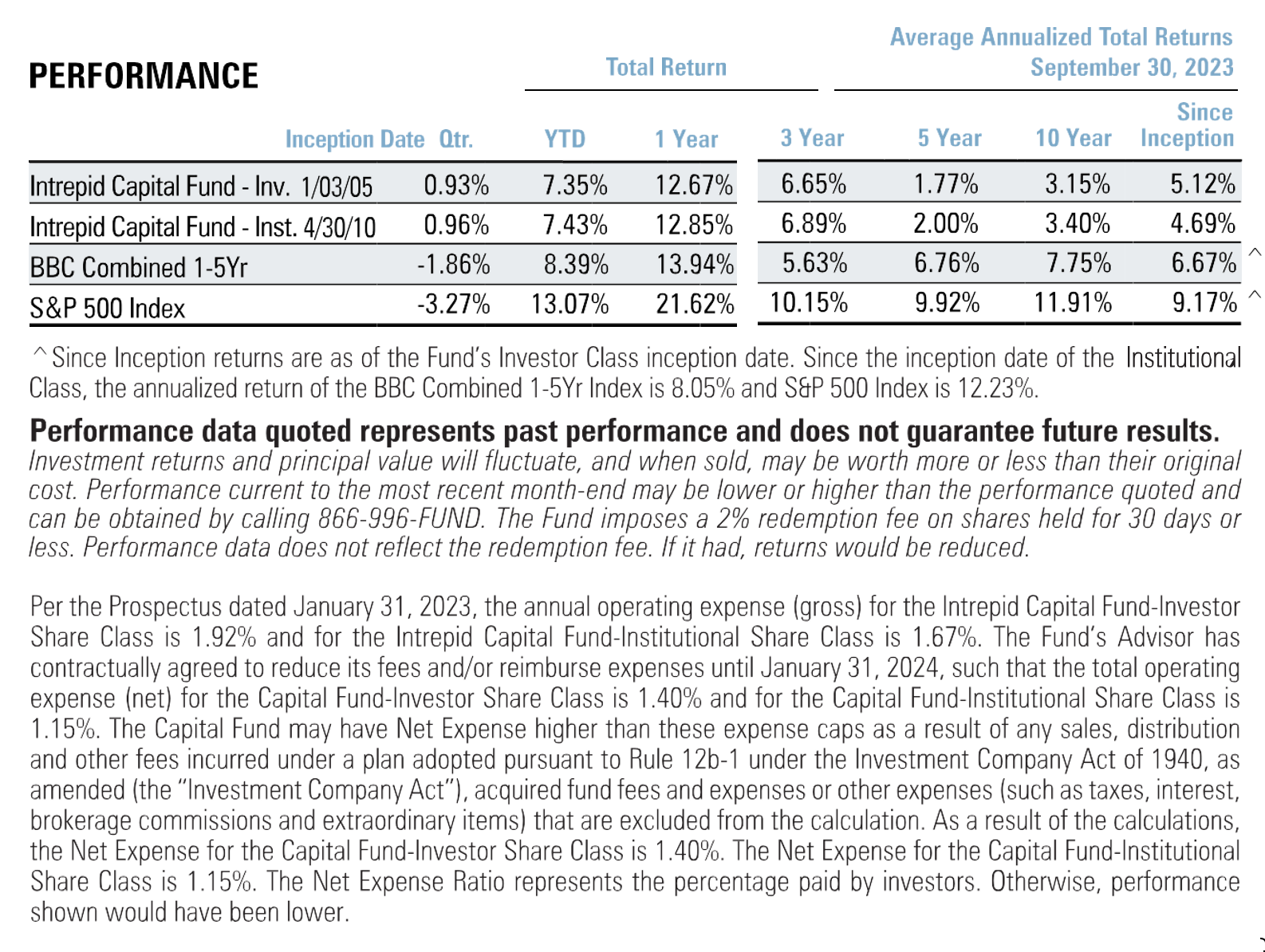

I am pleased to say the Fund closed out the fiscal year ended September 30th, with a solid 12.67% return. This return puts the Fund in the upper quintile of its peers for one year and upper decile over the last three years. This message to stay invested is easier to say than do, I realize, particularly after a difficult August and September this year. Although October is more famous as a difficult month, I think statistically September may have it beat.

I do recognize there is plenty for one to worry about, such as a possible government shutdown, mortgages at 7.75%, oil at $94/barrel, gas approaching $4/gallon, student loan repayment restarts, a looming Presidential election, war in Ukraine, etc. etc. To close I leave you with one more Charlie Munger quote: “The Big Money is not in the buying or selling, but in the waiting.”

I will be here waiting! Waiting for shares in businesses where our interests are aligned with management who often own a large stake in the company they founded (or are family members of founders), along with the types of bonds I described above.

Thank you for your continued support, if there is anything we can do to serve you better, please don’t hesitate to call.

Top Contributors in Q3 2023 Top Detractors in Q3 2023

Civitas Resources (CIVI) Atento, 02/10/2026, 8%

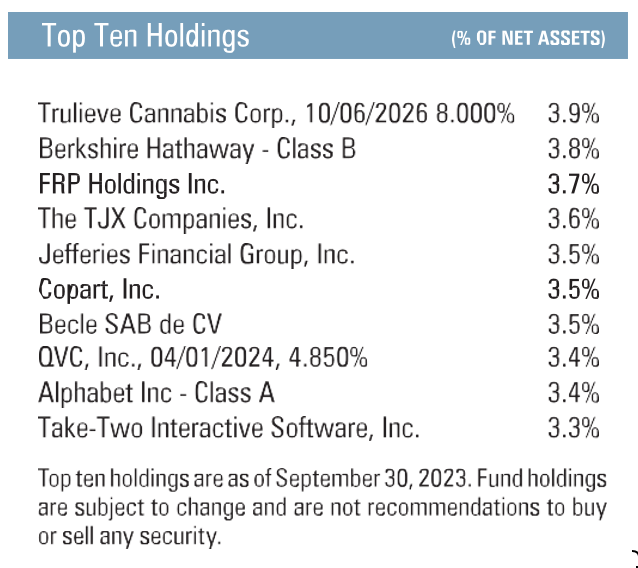

Trulieve Cannabis, 10/06/2026, 8% Dollar General (DG)

Alphabet – Class A (GOOGL) Live Nation (LYV)

Top Contributors in Fiscal Year 2023 Top Detractors in Fiscal Year 2023

Civitas Resources (CIVI) Atento, 02/10/2026, 8%

Copart (CPRT) Dollar General (DG)

Alphabet – Class A (GOOGL) CVS Health (CVS)f

All the best,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager