July 1, 2023

“You can observe a lot just by watching.”

-Yogi Berra

Dear Fellow Shareholders,

I sure hope you were able to watch the College World Series in late June between Florida and LSU. What a home run derby that series was…exciting to the end!

What I have observed so far this year is that equity markets have climbed the proverbial “wall of worry.” Those worries include, but are not limited to: bank failures in March, a congressional debt ceiling standoff, uncertainty over the future direction of interest rates, and continued fears of recession. These fears were juxtaposed against the current mania around all things A.I. (artificial Intelligence).

In this current flight of investors fancy, investors poured money into the shares of index heavyweights such as Microsoft and Nvidia.

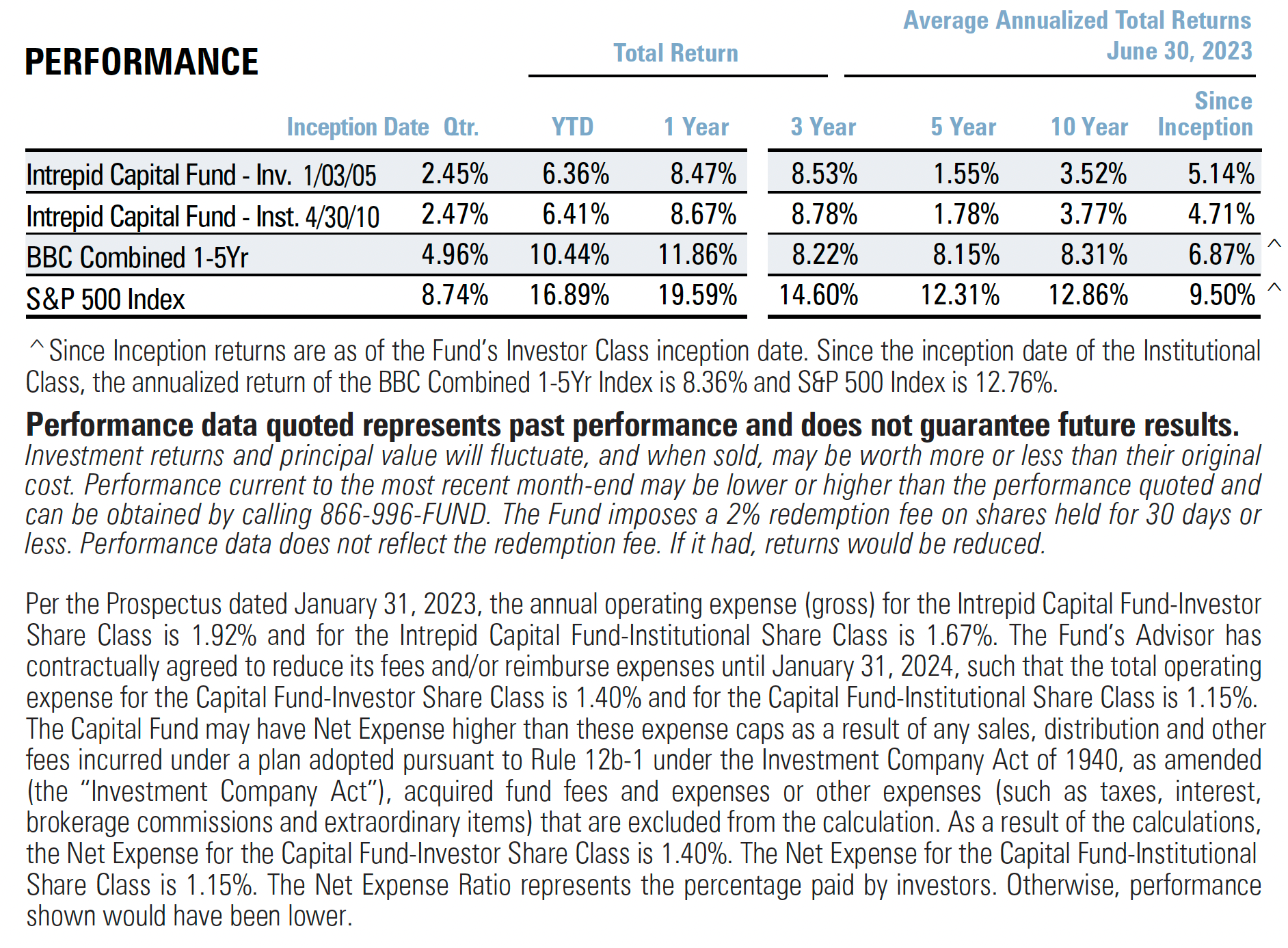

This pulled the S&P 500 Index up 8.74% for the second quarter of 2023. Similarly, much of the 16.89% year-to-date return of the S&P 500 Index is due to the same stalwarts mentioned above. Also posting exceptional returns for the year-to-date period were investor favorites Apple (+49%), Tesla (+113%), and Meta (+138%) – which are not sustainable in my opinion.

The rebound in technology stocks this year follows a tough 2022, which saw the technology-heavy Nasdaq 100 Index fall 32%. There was a similar reversal in the sentiment of energy stocks, which surged last year but are down 5% through the first half of 2023. The polar opposite environment this year is a good reminder of the importance of diversification!

So where do we go from here? I suspect, despite many on Wall Street calling for a bear market, that prices instead move higher. Historically, the third term of a Presidency has generated better than average results, although strategists like Mike Wilson at Morgan Stanley and others are calling for the S&P 500 Index to trade down to 3200, down roughly 29% from the current index price of 4500.

This time last year I closed the second quarter 2022 commentary with the following “I think when we look back 12-24 months from now that returns will more closely resemble long-term results for a portfolio consisting of stocks, bonds and cash.” I love it when predictions come true!

At Intrepid Capital we have tended toward smaller capitalization companies as represented by the Russell 2000 Index, which have lagged the larger company shares like those household names I mentioned earlier (Microsoft, Apple, Meta, etc.) by over 8 percentage points annualized over the last 5 years. I think change may be afoot as $3.5 billion has flowed into small cap ETFs since the start of the year.

However, small cap investors need to be wary of potential minefields in this area of the market, as 40% of the businesses in the Russell 2000 are unprofitable. In addition, many of these companies are dependent on floating rate bank debt compared to larger companies that can more easily access the bond market, which leads to lower interest rate exposure.

Our focus has been in the profitable 55% of the Russell 2000, with balance sheets that are built to last.

Top Contributors in Q2 2023 Top Detractors in Q2 2022

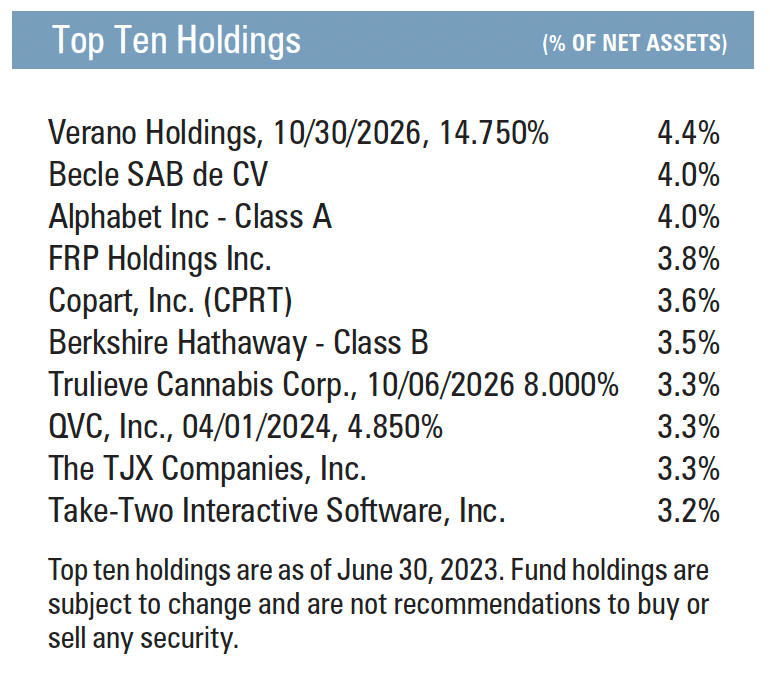

Copart, Inc. (CPRT) Atento Luxco 8% due 2026

Take-Two Interactive Software (TTWO) WNS Holdings LTD (WNS)

Alphabet, Inc., Class A (GOOGL) Levi Strauss & Co., Class A (LEVI)

Thank you for your continued support. If there is anything we can do to serve you better, please don’t hesitate to call.

All the best,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager