April 1, 2024

“Most investors do today, what they should have done yesterday.”

-Lawrence Summers, Former US Treasury Secretary

Dear Fellow Shareholders,

In our last letter, we were pleased to communicate a successful result for the final quarter of calendar 2023. The first quarter of calendar 2024 kept the streak alive with a another quarter of returns greater than 6% (6.25% to be exact) – closely matching the return in the prior period (6.41%). Returns for the trailing 12 months ending March 31, 2024, were 16.98%.

These returns have been against a backdrop of “how many rate cuts, and when do they start?” speculation from Wall Street pundits. The anticipation of lower rates has powered the equity markets higher since October of 2023.

However, that perception is starting to change as we enter April due to recent inflation and employment numbers coming in “hotter” than the markets anticipated. I have asked the question internally: “what if they don’t cut rates”?

As we discussed in our last communication, the silly season (aka Presidential race) is upon us and the Federal Reserve is running out of time if they want to try to be apolitical and not cut short term rates close to the November election. These inflation and unemployment numbers keep pushing back the date for this to occur.

Due to i) a drop in the official inflation rate from 9% in June 2022 to 3.8% in March 2024, and ii) a record low unemployment rate. I would have thought the President would be polling much stronger than he is. I read recently that, since January 2021 (President’s Biden inauguration), consumer prices across the board were up roughly 20% and is likely what voters have anchored on. I always thought only government statisticians could come up with a “core” inflation number that excluded food and gas, which only applies to the citizens that don’t drive or eat!

I continue to position the Intrepid Capital Fund as an “all-weather tire” by minding the allocation between stocks, bonds and cash (or, better said, money market funds). This stays very consistent with roughly 60% of the Fund dedicated to stock holdings, 35% devoted to bonds, and a residual of ~5% in cash (money market). This is an attempt to deliver an attractive risk/return profile with both growth and income.

In a quarter like we just experienced, one might guess there were few meaningful detractors and that was certainly the case for the Fund in Q1 of 2024.

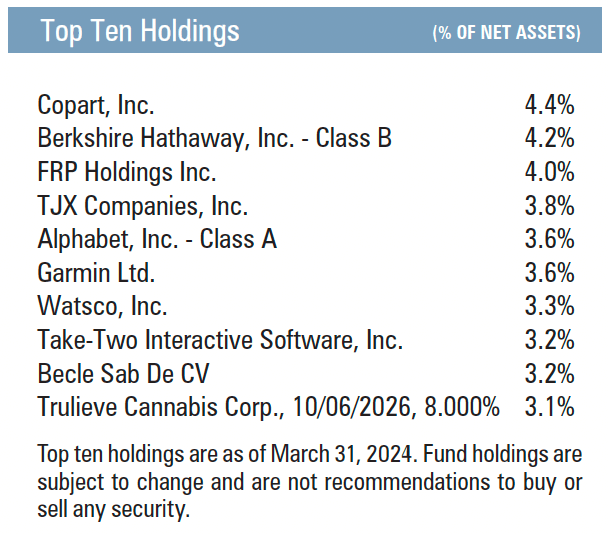

The top Contributors were Acuity Brands (AYI), Copart (CPRT), Berkshire Hathaway – Class B (BRK/B). The top detractors were Dropbox – Class A (DBX) and WNS Holdings (WNS).

Thank you for your continued support! If there is anything we can do to serve you better, please don’t hesitate to call.

All the best,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager