April 1, 2023

“Blessings we enjoy daily; and for the most of them, because they be so common, most men forget to pay their praise.”

— Izaak Walton

Dear Fellow Shareholders,

Dear Fellow Shareholders,

The author of the quote above, from the book “The Complete Angler,” wasn’t thinking about his blessings in the financial markets. Instead, he wrote those words about fishing. I too have reacquainted myself with a love of fishing from my youth. I find the distraction and focus required to be successful at fishing useful after a day staring into the flashing red and green symbols on my Bloomberg screen!

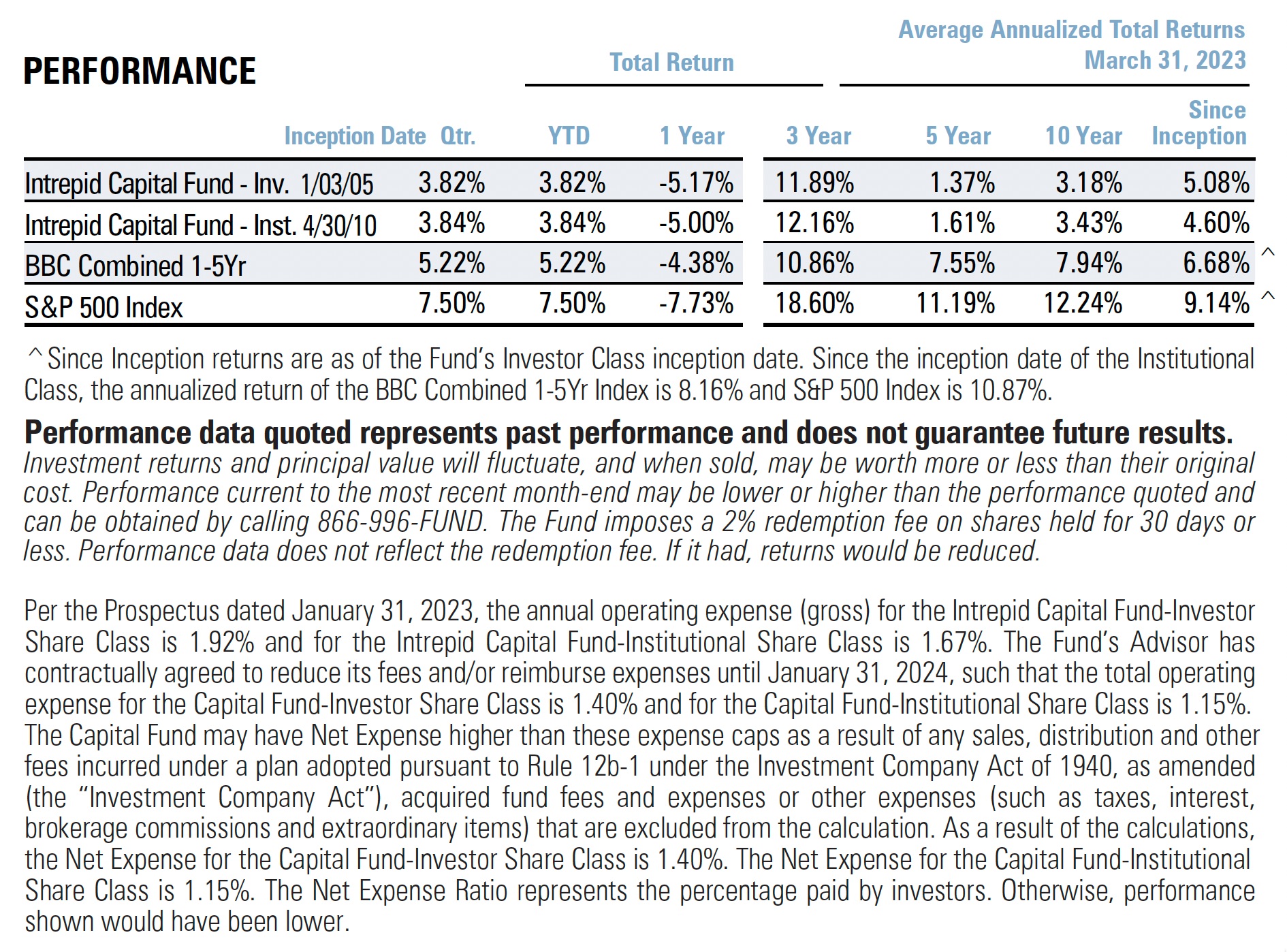

The Intrepid Capital Fund successfully completed the first six month’s of the funds fiscal year ending March 31, 2023. For the first quarter of this calendar year, the Fund appreciated 3.82% which, when compounded on the 4.96% return in the fourth quarter of 2022, resulted in a non-annualized 8.97% total return over the six months since September 30, 2022. Included in these results was a dividend paid on March 31, 2023, of 22.59 cents per share.

We are now living through the experiment from several years ago that some describe as “modern monetary theory” which brought us, at one point, 18 trillion (with a T!) of negative yielding debt. Only a room full of PhD’s could come up with something like that. I mean really – am I going to deposit my monies in a bank account and “earn” negative interest rates so I will be worse off when I come back for my funds!? At one point, retailers in Germany couldn’t keep safes in stock as locals preferred a safe over their local bank! The Federal Reserve, staffed with 400 PhD’s, has now realized the error of their ways and raised the Fed Funds rate from close to zero in March of 2022 to roughly 5% now. That has now acquainted the public with a term I have used frequently in the past: duration (as a measure of interest rate risk). As well as the term “uninsured” depositors.

March of 2023 brought us the largest bank failure since the Great Financial Crisis of 2008 when depositors at Silicon Valley Bank requested $147 billion be paid back to them in two days. Regulators quickly moved to close the bank. While the bank had the highest credit quality assets in US Treasury bonds, they had significant unhedged duration risk coupled with close to 80% of deposits over the $250,000 FDIC limits.

To give you a specific example applicable to Silicon Valley Bank, if you bought a 10 years to maturity Treasury bond at a 2% yield at par (100) and due to inflationary pressures and Federal Reserve activity the current rate was now 4%, the bond you bought at par when rates were 2% is now worth 83 cents on the dollar. I am amazed that bank regulators didn’t insist that management hedge that duration risk. Well, the rest is history.

The Intrepid Capital Fund hasn’t been a bank investor since inception for the simple reason it is very hard to understand the various assets a bank holds. We know the liabilities are the deposits, which as we have seen in the example above can quickly flee. There isn’t a bank out there that could survive a “run” on their deposits. A good example of a bank run is from one of my favorite movies “It’s a Wonderful Life” where Jimmy Stewart pleads with his neighbors to keep their money in his savings and loan – arguing that Joe’s deposits are in Carl’s house, etc.

My preference is for less exciting investments in the equity markets. I am attracted to founder/managers that often have a significant ownership interest. I have observed that this type of owner/operator often runs a company void of liabilities on the balance sheet and to quote the famous race car driver Mario Andretti “to finish first, you must first finish.” These balance sheets are built to finish.

Two recent acquisitions fit this bill to a “T.” Garmin (GRMN) dominates the marine/avionic/fitness categories for navigation. The families that founded the firm have a combined equity stake of roughly 20%, and the company has a billion (with a B!) in cash on the balance sheet. Watsco (WSO) is run by the father/son team of Albert and AJ Nahmad. This company is the leading HVAC distributor in the country with a large portion of their revenues coming from replacement equipment. Anyone close to the beach in Florida knows that the replacement cycle can be short!

I believe we are closer to the end than the beginning of the Federal Reserves rate hikes, but that doesn’t mean we won’t have price volatility around announcements of Consumer Price Index (CPI) statistics or future Fed policy. I will continue to seek investments like the two mentioned above when volatility spikes.

Thank you for your continued support. If there is anything we can do to serve you better, please don’t hesitate to call.

Sincerely,

Mark F. Travis, President

Intrepid Income Fund Co-Portfolio Manager